At the C2C conference on the Prospects of the Banking Industry in 2024 from Techcombank’s perspective, Mr. Phung Quang Hung – Deputy CEO, Director of the Corporate and Institutional Financial Division of Techcombank, shared the main drivers supporting the growth of the banking industry in 2024.

The C2C conference organized by HSC on March 6th. (Screenshot)

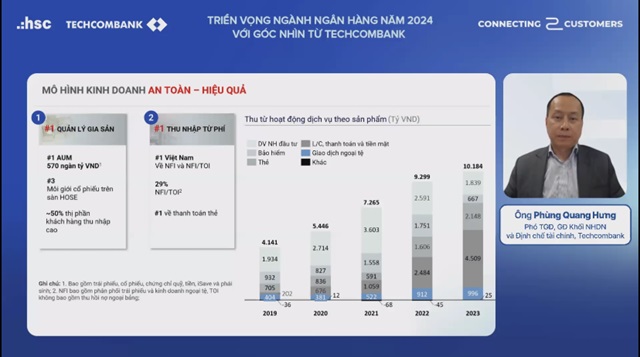

|

Mr. Hung stated that in the corporate customer segment, FDI capital continues to flow strongly into Vietnam. Specifically, disbursement of FDI capital in the first two months of 2024 reached its highest level in the past 5 years and grew nearly 10% compared to the same period last year. In which, registered FDI capital doubled and diversified across sectors, including real estate, demonstrating the potential of these sectors.

In the import-export businesses, the import-export turnover in the first two months of the year also reached the highest level in the past 5 years. This is positive as export activities, especially in the first half of last year, experienced a decline. Many industries faced a 20-30% decrease in output due to reduced consumption in major global markets caused by central banks’ tightening monetary policies.

Mr. Hung emphasized that the recovery of export growth is significant for Vietnam as exports account for a large proportion. This is also a growth driver for 2024.

Mr. Hung highlighted that if we look at domestic sectors such as the real estate value chain, we can see that after the difficulties of the first 9 months of last year, real estate transaction sales have shown positive signs since the last quarter.

Looking at other aspects of domestic supply companies, the domestic consumption and demand for retail goods have consistently shown positive growth in recent months. This means that consumer spending is increasing, which has a positive impact on these businesses.

In terms of the retail industry, which means the individual customer segment, the percentage considered as the middle income upward class in Vietnam continues to increase rapidly due to Vietnam’s general GDP development and urbanization pace.

With these factors, the financial needs of both corporate and individual customers are expected to continue growing positively in 2024.

Regarding the financial needs of customers, for example, in the bond market, when individuals hold bonds as investment tools or asset preservation, bond debt accounts for only 15% of GDP. This figure is still very low compared to other countries in the region. Additionally, insurance fees/gross domestic product and the value of fund certificates or home loans compared to Vietnam’s GDP are also at low levels compared to other countries in the region. This represents potential for development.

In conclusion, Mr. Hung expects that the development momentum of the industry will come from the special segments of corporate customers, such as FDI, infrastructure construction, domestic consumption (FMCG), and export services. For individual customers, the momentum for banks to continue developing comes from the segments of customers with moderate and upward income, which continues to increase.

In addition to these drivers, Mr. Hung also noted that unexpected factors may impact the banking industry.

Firstly, the global economic environment, the extent of economic recovery in major economies such as the US and Europe, and the pace at which the US Federal Reserve reduces interest rates to promote the economic development of fast or slow markets. If the pace is fast, it will be a positive factor, otherwise, it will have less positive impact than expected.

Secondly, for the domestic market, for example, the recovery of the real estate market, although there are positive signs, the recovery rate continues to increase or slow down, it will also have certain impacts because real estate construction supply chains contribute a significant proportion to GDP.

Or the macroeconomic aspect of Vietnam, factors such as inflation and interest rates, how they will evolve. Currently, according to general forecasts, inflation will slightly increase as Vietnam continues to maintain a low-interest rate environment to promote economic development.

“However, a non-positive factor is that if Vietnam’s market interest rate increases more than expected, it will also affect the financial costs of businesses. However, the probability is low because the current Vietnamese market liquidity is abundant and with such a large FDI capital inflow, the State Bank of Vietnam also has much room to manage interest rates and exchange rates,” Mr. Hung noted.

By Khang Di