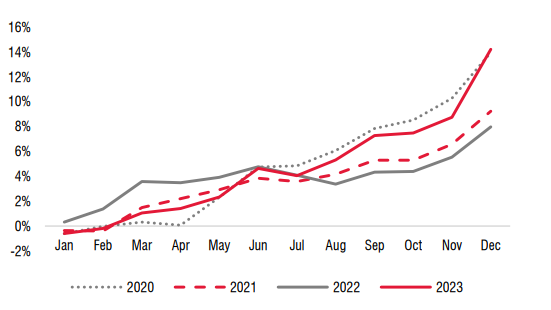

In terms of cash flow, the analysis team points out that record-low interest rates will be the main driver of growth, especially for individual investors. Bank deposits continue to increase as other investment channels are limited.

|

Growth of deposits since the beginning of 2023

Source: SSI Research

|

The flow of individual investor capital is expected to return to the stock market in stages in 2024; and since individual investors accounted for 92.2% of the average daily trading volume in the entire market in 2023, the analysis team predicts that the VN-Index will have significant breakthroughs in 2024 thanks to this capital flow.

Foreign investors had a net withdrawal in 2023, and the analysis team believes that this trend will reverse in 2024 following the Fed’s gradual interest rate cuts and the opportunity for the Vietnam stock market to be upgraded by FTSE Russell to an emerging market in the 2024-2025 period. The inflow of foreign investor capital may not recover immediately, but the selling pressure from foreign investors is expected to be less strong than the previous year.

In terms of fundamental factors, the analysis team believes that the recovery of the economy will become more evident in the second half of 2024, with exports increasing due to global interest rate reductions and consumer confidence gradually returning.

Domestically, the main focus will still be on the recovery of the real estate sector in the context of real estate companies needing to quickly resolve legal issues of projects and the high real estate loan-to-value ratio. If liquidity in the real estate and corporate bond markets does not recover quickly, consumer confidence will be affected.

The main highlights of the real estate sector in 2023 identified by SSI Research include the relatively slow resolution of legal issues of existing real estate projects and the passage of important new regulations (Land Law, Housing Law, and Property Law) by the National Assembly to enhance the protection of homebuyers’ rights and stabilize the market.

If the legal issues of existing projects are not resolved early in 2024, the analysis team predicts that M&A activities will increase significantly and focus on projects with sufficient legal compliance. Therefore, the estimated supply may improve positively from the low level in 2023. Liquidity in the market continues to improve for the mid-range segment in major cities, where there is a large shortage of supply, although the pace of improvement may be slow due to high prices.

On the other hand, the resort real estate segment may continue to face many challenges. Fundraising from the sale of projects with sufficient legal compliance can help real estate companies buy more time to resolve legal issues for projects still in progress.

“We forecast that the recovery of the real estate market will be differentiated among segments and will take more time to fully recover. Only real estate companies with strong financial health can overcome the challenges in 2024.

The non-performing loan ratio of banks may reach its highest level in the third quarter of 2024, and then decrease according to our base scenario. The prospects for the real estate and banking sectors may not be favorable in 2024.

The expected recovery process will take place slowly, not to mention some factors that need close monitoring, including the draft land tax currently being developed by the Ministry of Finance, which will have a major impact on real estate demand,” the forecasters said.

In addition, other factors that need to be closely monitored include the geopolitical situation and domestic economic recovery support policies.

The fair value for the VN-Index at the end of 2024 is 1,300 points

The analysis team believes that profit growth will be the main driver of superior stock performance this year. In addition, in the context of record-low interest rates, high dividend yields are becoming an attractive factor.

The estimated profit growth for 2024 of 83 stocks within the SSI Research coverage is expected to reach 15.3% compared to the same period (a decrease of 5.6% compared to the same period last year). Some industries are expected to experience significant recovery (post-tax profit growth of more than 30% compared to the same period) such as steel, retail, and securities.

“In addition, we also have positive views on the information technology and industrial real estate sectors based on long-term growth potential,” the analysts said.

SSI Research believes that the fair value for the VN-Index at the end of 2024 is 1,300 points, and the market may surpass this threshold at certain times during the year.

{kind=link}