Projects 2026 Profit Decline, Marking a 5-Year Low")

")

: Mixed Signals Emerge")

: Short-Term Outlook Continues to Deteriorate")

C2C conference organized by HSC on 06/03. (Screenshot).

|

At the C2C conference on the prospects of the banking industry in 2024 from Techcombank’s perspective, experts from HSC provided an analysis of the overall picture of the banking industry.

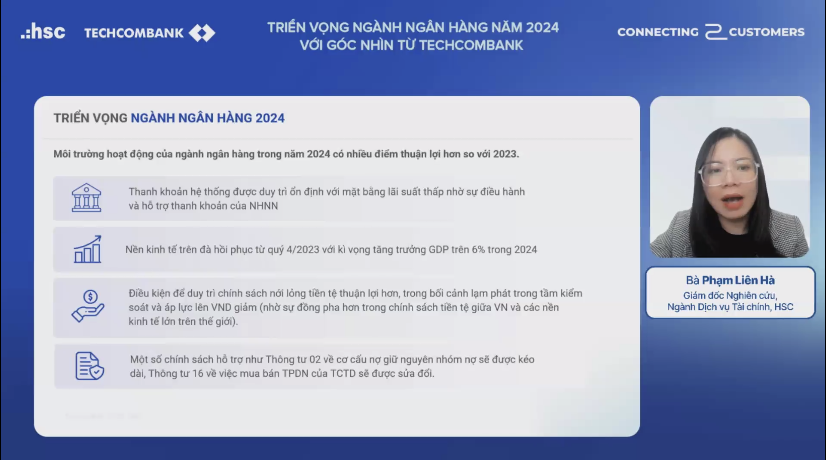

According to Pham Lien Ha, Director of Financial Services Research at HSC, the operating environment of the banking industry in 2024 will be more favorable compared to 2023.

The first advantage is that the liquidity of the banking system is maintained stable with low-interest rates due to the management and liquidity support of the State Bank.

The second advantage is that the economy is on track to recover from Q4/2023 and is expected to continue growing with a GDP growth target above 6%.

The third advantage is that the conditions for the State Bank to continue its loose monetary policy are also more favorable in the context of inflation being under control and pressures on the VND have reduced compared to last year, thanks to better coordination in Vietnam’s monetary policy with major economies worldwide.

Furthermore, some supportive policies, such as Circular 02 on debt restructuring and Circular 16 on the trading of corporate bonds by credit institutions, are likely to be extended and amended.

Based on these favorable factors, Ha expects credit demand to recover, leading to better credit growth in 2024 compared to the low level in 2023.

“The growth momentum for the banking industry in the first half of 2024 will come from public investment, exports and imports, and the FDI customer segment. Although slightly slower, credit growth from individual customers for both consumption and investment purposes is also expected to recover stronger in the last 6 months of the year,” Ha assessed.

In terms of NIM, after a decline of about 50 basis points in 2023, this expert expects a slight recovery with an increase of about 20-30 basis points.

Regarding fee-based activities, Ha predicts a certain level of recovery from the low level of last year, especially in bancassurance. Nevertheless, this activity will still face many difficulties in 2024.

Regarding asset quality, although there has been improvement in Q4/2023 with a decrease in the NPL ratio, this is still a point of concern.

Ha pointed out two noteworthy points. The first is that the overall NPL ratio at the end of 2023 is still relatively high, about 4.8-4.9% (although more than half of this NPL ratio comes from NPLs in banks under special control or restructuring, such a high NPL ratio will be a bottleneck for the economy if not addressed).

The second point is the NPLs of the leading banks or specifically the 14 banks in HSC’s monitoring list, which stood at 1.67% at the end of 2023, only slightly higher than the 1.5% at the end of 2022. However, this is due to Circular 02. At the end of 2023, the total debt restructured according to Circular 02 was VND 183.5 trillion, equivalent to about 1.35% of the total credit balance of the whole banking system. If we add the restructured debt ratio of 1.35% to the overall NPL ratio of the industry or to the NPL ratio of the 14 leading banks, the actual NPL ratio is still relatively high.

“However, with continued supportive policies in 2024 and the recovery and growth of the economy as well as credit growth, the relative scale of NPLs and provisioning pressure is still under the control of banks, and there is a high possibility of slight improvement,” Ha said.

With the above viewpoints and forecasts, the expert estimated that the profit growth of the 14 leading banks will reach 20-21% in 2024, higher than the 5.5% profit growth in 2023.

Khang Di

{kind=link}