")

: Mixed Signals Emerge")

: Short-Term Outlook Continues to Deteriorate")

The market seemed to be on the brink of a breakdown, but today’s magnificent surge thwarted it. Bank stocks performed well, but they couldn’t prevent the VNI from ending the session in the red.

The market was robust in the morning session, with high liquidity fueled by strong proactive demand. The breadth was impressive, and the trading of bank stocks was lively, boosting liquidity. However, this consensus abruptly vanished, and the afternoon selling pressure caused many stocks to reverse their gains.

This still reflects short-term trading behavior. If we consider the four recent losing sessions as a rapid pullback due to profit-taking, today’s performance resembles fresh money entering the market when selling pressure subsides. Nevertheless, the supply of stocks continued to outweigh demand, pushing prices down.

Nonetheless, the market is not in a dire state. There are no adverse developments that could trigger surprise or panic. Fluctuations result from typical supply and demand dynamics, although the trading volume is more significant than usual: The matching value of the two exchanges increased by nearly 34% compared to yesterday, reaching approximately VND 16,500 billion.

Today’s performance of bank stocks is a positive sign, indicating that after a period of consolidation, money flow remains robust. The market desperately needs a leading stock or a catalyst to ignite bullish sentiment. The recent failed attempts to break above the peak were due to the lack of a strong enough leading sector and sufficient capital flow. Currently, earnings reports are trickling in, and there will be both positive and disappointing figures. Overall, the market’s differentiation aligns with the current phase, and the ability to select the right stocks will be decisive. This market cannot be traded based on trends, but rather by focusing on specific portfolios.

I maintain the view that the market is in a normal state, and it is advisable to maintain a balanced stock proportion. The intense intra-day adjustments in specific stocks can be gradually bought back. Whether the VNI surpasses the 1,300 mark is irrelevant; instead, focus on the money flow of individual stocks. The current situation may persist, and there won’t be a “wave of earnings reports” reflected in the index but only in isolated stocks.

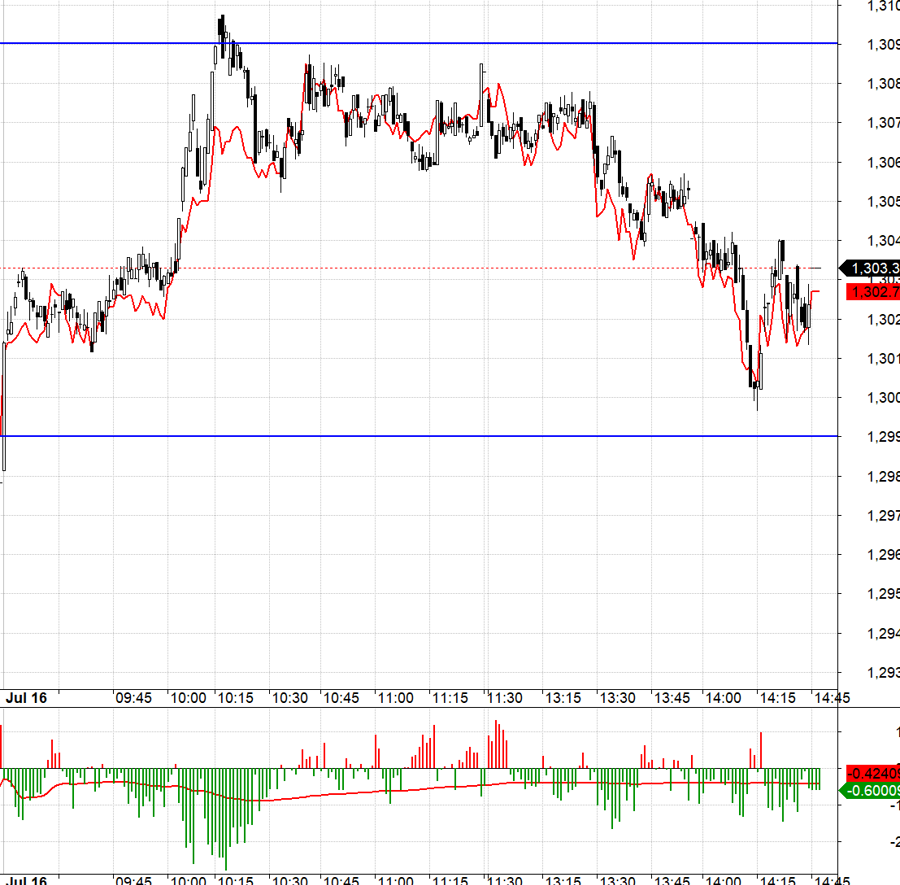

The futures market is approaching expiration with F1, so the basis will be tight, favoring both Long and Short positions with safe stop-loss levels. However, VN30 is within a broad range of 1299.xx to 1309.xx, making trading more challenging. VN30 opened this morning above 1299.xx and, after a period of consolidation, bank stocks surged. With their pulling power, VN30 has a better chance of reaching 1309.xx than falling back to test 1299.xx, so Long positions are more probable.

After the rise to 1309.xx and the closure of many Long positions on F1 (basis expansion discount), VN30 hugged 1309.xx until the start of the afternoon session. This phase is tricky because, while bank stocks remain robust, other pillars are gradually weakening, facing substantial selling pressure. Overcoming this resistance requires high liquidity, and active selling orders in other pillars push prices down. VN30 then has three plausible scenarios: breaking through 1309.xx, trading sideways and hugging 1309.xx with a narrow range, or gradually sliding towards 1299.xx. Thus, the preferred strategy is to Short, with a stop-loss threshold based on scenario 1, and if the Short position is placed close to 1309.xx, even if scenario 1 doesn’t unfold, the outcome will be a breakeven or a minor loss in scenario 2. Ultimately, VN30 followed scenario 3, sliding towards 1299.xx as bank stocks also came under selling pressure.

Today’s session indicates a lack of sufficient consensus and money flow. The market may experience further adjustments before significant capital inflows balance it. The strategy remains to be flexible with Long/Short positions in derivatives.

VN30 closed today at 1303.3. Tomorrow’s resistances are 1309, 1315, 1320, 1326, 1331, and 1339. Supports are 1297, 1291, 1285, 1279, and 1271.

“Stock market blog” reflects personal views and does not represent the opinions of VnEconomy. The perspectives and assessments are those of the individual investor, and VnEconomy respects the author’s style and viewpoint. VnEconomy and the author are not responsible for any issues arising from the published investment views and opinions.

Dragon Capital Chairman: “Long-term vision is needed, accepting necessary adjustments for a safer, more efficient, and higher quality market”

According to Mr. Dominic Scriven, Chairman of Dragon Capital, the role of the finance industry in the stock market will be significant in 2023 and possibly in 2024. The roles of other industries, such as real estate or consumer goods, will depend on their respective challenges.

Investing in a volatile market: Should beginners consider putting money into high-yield bonds for 10-30% yearly profit?

Short-term stock market trading has proven to be a risky venture for many investors, leading to substantial losses. However, there are a few select open funds that have managed to achieve impressive returns, reaching up to 30%.

{kind=link}