: Robusta Cools Down")

: Q3 Earnings Reports Flood In, Xuan Thien Group’s Subsidiary Posts Another Loss")

: Will the Recovery Trend Continue?")

: A Mixed Bag of Wins and Woes")

2024 Apartment Consumption Expected to be the Highest in 4 Years

According to the OneHousing Market Research and Customer Insight Center, in the first half of 2024, the Hanoi market recorded more than 52,000 transactions, of which apartments (both primary and secondary) accounted for 54%.

New supply, transaction volume, and unit price increases indicate that the Hanoi market has passed the recovery phase and entered a strong growth period. Specifically, Hanoi’s primary supply in Q2/2024 increased for the fifth consecutive quarter, reaching 8,400 units, up 97% from the previous quarter and up 340% year-on-year. Favorable macroeconomic factors and the consecutive launch of new projects drove the Q2 supply to its highest level since 2020.

Apartment transactions increased in both volume and selling prices. Specifically, compared to Q1/2024, the number of transactions in Q2/2024 increased by 49%, and the average unit price increased by 21%.

OneHousing’s research shows that in the 2024-2025 period, the Hanoi apartment market is expected to introduce and absorb approximately 22,000-23,000 units annually. The supply and consumption in Hanoi during this period are forecasted to surpass the 2020-2022 period and be the highest in the last four years.

The new supply in Q2 mainly came from the luxury and high-end segments, accounting for 97% of the total market. The absence of new affordable housing and the minimal presence of mid-range options (~3%) indicate a shift in the market dynamic, with luxury and high-end segments dominating the supply.

Future supply is expected to come largely from the eastern and western regions of Hanoi, where new subdivisions and projects are being developed on a large scale.

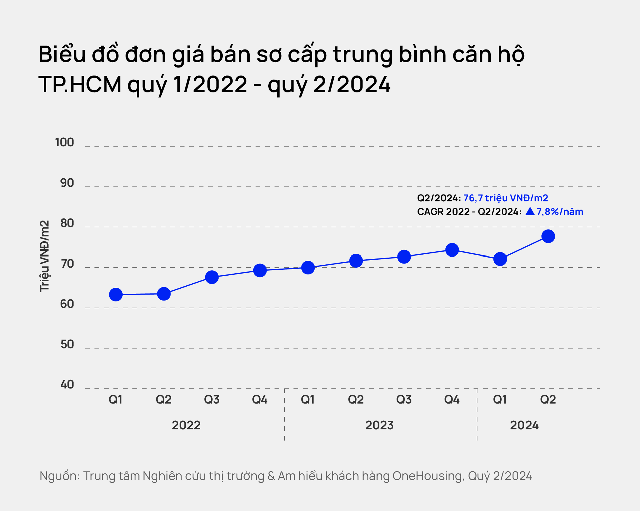

Ho Chi Minh City’s Apartment Prices Hit a Record High in Q2

Lagging slightly behind Hanoi’s market, Ho Chi Minh City’s apartment market is anticipated to enter a recovery phase in the 2024-2025 period, with supply and consumption forecasted to surpass 2023 levels.

Specifically, in the first half of 2024, Ho Chi Minh City recorded a 132.5% increase in new apartment supply in Q2 compared to the previous quarter. Experts predict that the market will recover during this period, with an expected supply of 8,000-10,000 units per year.

The luxury segment is leading the Ho Chi Minh City apartment market in the first half of 2024, accounting for 54% of new supply, with most new projects located in the eastern part of the city.

Notably, the average primary selling price in Ho Chi Minh City in Q2/2024 reached a record high of VND 76.7 million/sqm, a 6% increase compared to the same period last year. Despite the high prices, consumption in Q2/2024 still increased by 7.3% year-on-year to 1,600 units, higher than the new supply (~1,200 units). The consumption of luxury and high-end apartments accounted for 80% of the total.

Mr. Tran Minh Tien, Director of the OneHousing Market Research and Customer Insight Center, believes that the positive macroeconomic indicators and the upcoming enactment of the three amended Real Estate Laws will lay the foundation for the continued growth of the apartment market in Hanoi and Ho Chi Minh City in the second half of 2024 and beyond.

Regarding the Hanoi market, the Q2 figures demonstrate a robust recovery in the apartment sector after five consecutive quarters of growth, signaling the beginning of a new growth phase. Meanwhile, the Ho Chi Minh City real estate market is expected to enter a recovery phase in 2024-2025 as legal issues surrounding projects are gradually resolved and new apartment supply increases compared to 2023. The luxury and high-end segments will dominate new supply in both markets. Well-planned mega-cities and reputable developers with strong financial capabilities will have the opportunity to lead the market in the coming years.

{kind=link}