: Crypto Ventures")

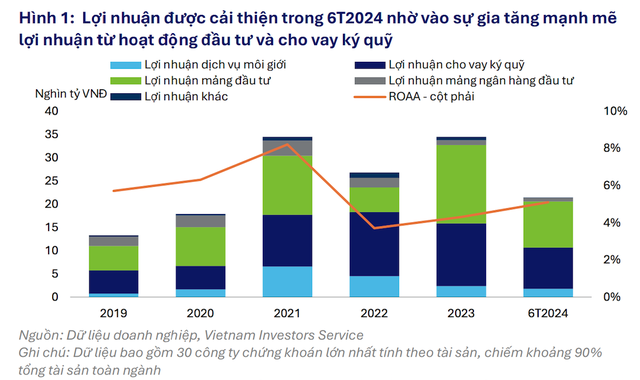

In its recent update, Vietnam Investment and Securities Investment Rating JSC (VIS Rating) reported improved profitability in the securities industry for the first half of 2024, particularly among larger securities companies.

Margin lending profits surged by up to 70% year-over-year in the first half

Specifically, the industry’s average return on total assets (ROAA) increased from 4.3% in 2023 to 5.1% in the first half of 2024. Strong market sentiment, low-interest rates, and a declining incidence of bond defaults boosted trading volume, stock valuations, and encouraged investors to engage in more margin borrowing.

Margin lending profits for large securities companies (SSI, VPS, HCM, MBS) increased by 40-70% year-over-year, while investment profits rose by 25%.

Securities companies actively involved in bond underwriting and distribution (TCBS, ORS) saw significant profit increases from distribution, underwriting, and bond custody, with an average rise of 160% year-over-year. Companies with large stock investment portfolios (VCI, SHS, VDS) also recorded substantial gains in investment profits.

For the second half of 2024, VIS Rating anticipates that profits from margin lending and investing in fixed-income assets will help securities companies maintain a stable ROAA, despite a decline in the stock market’s value from its peak in Q1 2024.

Asset risks are expected to stabilize in the second half of 2024

According to VIS Rating, some securities companies focusing on bond underwriting and distribution still carry high risks due to their increased investment in corporate bonds and their commitment to buy back the bonds they distribute.

Notably, TCBS, VPBANKS, and VND have increased their holdings of bonds issued by large enterprises and continue to broker buyback commitments for the bonds they sell to investors. VND recorded overdue receivables in Q2 2024 from a large customer in the renewable energy sector, which recently defaulted on bond principal and interest payments.

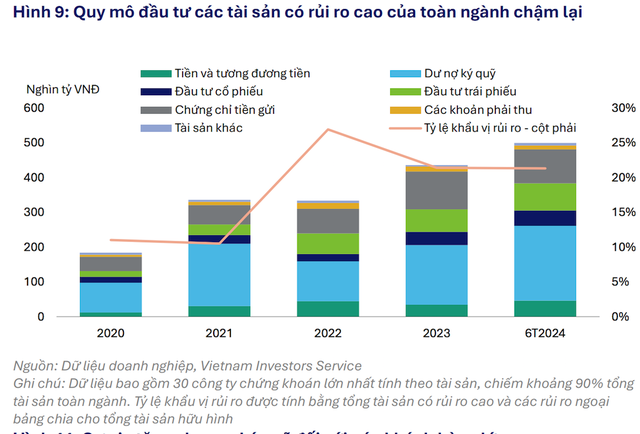

Margin lending to large customers has increased, raising the risk for securities companies if they are forced to sell collateral in a declining stock market, as occurred in Q4 2022.

However, VIS Rating experts expect asset risks to stabilize in the second half of 2024 as new bond defaults remain low. Additionally, the capital increases announced in the first half of 2024 by many large securities companies and those affiliated with banks will help strengthen their risk buffers.

“Securities companies have increased short-term borrowing to fund margin lending and investment activities, and liquidity risk remains well-managed thanks to a large volume of liquid assets,” the report also noted.

With liquid assets such as cash and certificates of deposit accounting for 30% of securities companies’ total assets, VIS Rating assesses that the industry’s liquidity risk, despite higher leverage, remains manageable.

However, some companies, including KAFI, FTS, MBS, and VND, which typically source 20-50% of their funding from institutional and individual customers, may face refinancing risks. Negative events could trigger a wave of withdrawals from these customers, potentially leading to liquidity issues for the securities companies.

{kind=link}