|

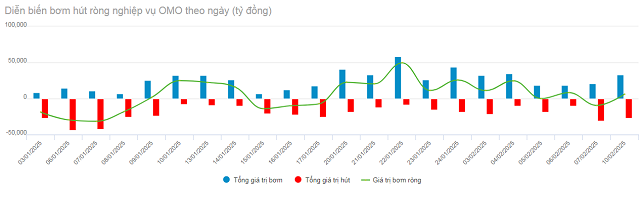

Net OMO pumping and sucking developments in the past week (03-10/02/2025). Unit: Billion VND

Source: VietstockFinance

|

Specifically, the SBV lent through the collateral channel with a total volume of 126,439 billion VND, with terms of 14 days (50,267 billion VND) and 7 days (76,172 billion VND). The interest rate for both terms was fixed at 4%/year.

The new issuance on the aforementioned term purchase channel mainly aimed to meet a large volume of maturities (98,613 billion VND).

In addition, the regulator consistently issued bills throughout the week, but the scale was significantly reduced compared to the pre-Tet week. The total volume of newly issued bills with a term of 7 days and a fixed interest rate of 4%/year reached 18,600 billion VND.

On the other hand, the lot of 31,250 billion VND bills matured in the week of 01/20-03/02, returning the corresponding volume to the market.

At the end of the week of 10/02, the SBV net injected 40,476 billion VND into the market. The circulating volume in the term purchase channel was 161,406 billion VND, and 22,850 billion VND in the bill channel.

|

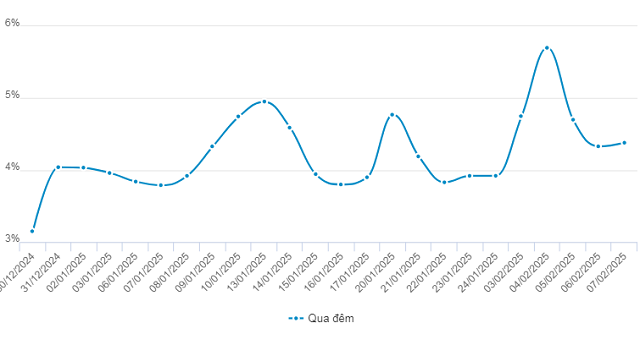

Interbank interest rate developments for overnight term since the beginning of 2025. Unit: %/year

Source: VietstockFinance

|

Regarding interbank interest rates, the overnight term rate soared to 5.7%/year in the 04/02 trading session when the system’s liquidity was tight after a long holiday. With the net injection move and liquidity support from the regulator, the interbank overnight interest rate cooled down to 4.38% at the end of the week (up 46 basis points compared to the pre-Tet week).

|

DXY movements since the beginning of 2025 up to the session of 11/02

Source: marketwatch

|

Last week, USD price remained high amid tensions between Trump and the US’s largest trading partners. At the close of 07/02, the DXY index increased by 0.63 points compared to the previous week (31/01), reaching 108.1 points, but lower than the 108.99 points of the first session of the week on 03/02.

The USD soared in the first session of the week on 03/02 due to President Donald Trump’s tariff moves but quickly cooled down after weak US employment data.

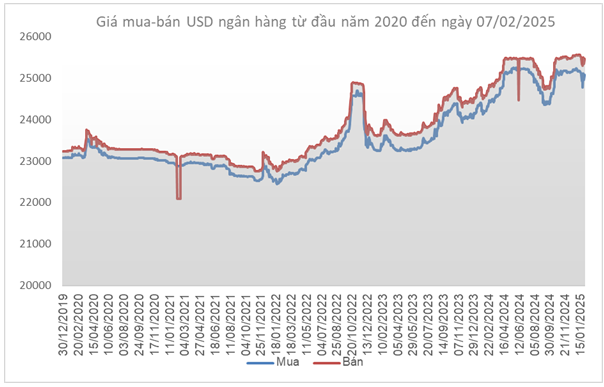

Source: VCB

|

USD/VND exchange rate at Vietcombank on 07/02 was listed at 25,080-25,470 VND/USD (buy-sell), up to 310 VND/USD in the buying direction but increased by only 170 VND/USD in the selling direction compared to the pre-Tet period.

– 10:31 11/02/2025

Market Beat: VN-Index Surges Over 6 Points in Late Recovery

The market was volatile during the afternoon session, with the VN-Index dipping into negative territory at one point. At the close of trading on January 16th, all three major indices managed to recover, but the gains were narrower compared to the morning’s enthusiasm.

The Green Land’s New ‘Stock’ with a Capital of VND 1,800 Billion has Just Been Assigned a Securities Code: Fourth Quarter Profit Triples Year-on-Year

For the full year 2024, Regal recorded net revenue of VND 550 billion, a 48% decrease compared to 2023, while posting an impressive 36% growth in after-tax profit, which stood at VND 162 billion.

The Cash Flows into Mid and Small-Cap Stocks

Although the VN-Index closed today with a modest gain of 0.39%, nearly a hundred stocks outperformed, rising over 1% compared to their reference prices. Notably, only six of these were from the VN30 basket, with the majority being small- and mid-cap stocks. Among these, several high-liquidity stocks stood out, leading the market’s gains.

The Highest Central Exchange Rate in a Year

As of February 4th, the Dollar Index weakened by 0.5% to 108.96, retreating from a three-week high of 109.88 touched the previous day. Despite this, the USD/VND rate remained under pressure as markets forecast a diminishing likelihood of the FED executing two interest rate cuts this year, with the probability now sitting at just under 50%.

The First Month of 2025: VN-Index Slips, Liquidity Hits 3-Year Low, Foreigners Keep Selling

The first month of the year witnessed a significant 23.4% decline in average trading values, bringing the figure to a meager 11.406 trillion VND. This places the monthly liquidity at a three-year low, a concerning development for the market.

{kind=link}