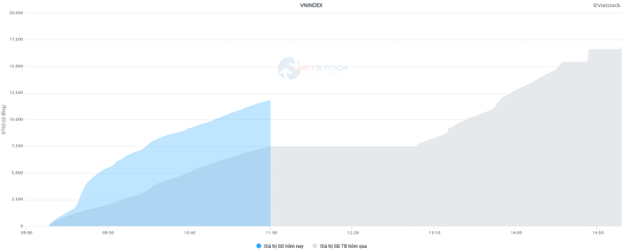

Market liquidity increased from the previous trading session, with the VN-Index matching volume reaching over 959 million shares, equivalent to a value of over 21.3 trillion dong; HNX-Index reached over 79.4 million shares, equivalent to a value of more than 1.2 trillion dong.

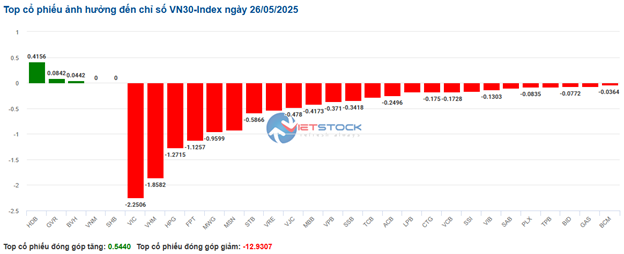

VN-Index opened the afternoon session with buyers gradually returning and taking the upper hand, helping the index surge and close in positive territory. In terms of impact, VHM, GVR, VIC, and BCM were the most positive influences on the VN-Index, with an increase of over 8.6 points. On the other hand, VPL, STB, ACB, and VRE were still under selling pressure but had little impact on the overall index.

| Top 10 stocks with the highest impact on the VN-Index on May 26, 2025 |

Similarly, the HNX-Index also had a rather optimistic performance, with the index positively impacted by IDC (+6.6%), PVS (+3.46%), VCS (+4.47%), and CEO (+4.72%)…

|

Source: VietstockFinance

|

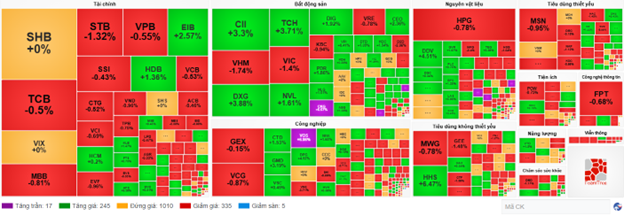

At the close, green covered all industry groups. The real estate sector was the group with the strongest increase of 3.13%, mainly driven by VIC (+1.61%), VHM (+6.83%), BCM (+4.93%), and SZC (+6.97%). This was followed by the materials sector and the telecommunications sector, with increases of 1.88% and 1.46%, respectively.

In terms of foreign trading, foreigners continued to sell a net of more than 35 billion dong on the HOSE exchange, focusing on VIC (92.9 billion), VCG (69.42 billion), GEX (56.66 billion), and HPG (52.51 billion). On the HNX exchange, foreigners sold a net of more than 13 billion dong, focusing on SHS (13.6 billion), HUT (5.7 billion), NTP (4.81 billion), and VCS (1.28 billion).

| Foreigners’ buying and selling dynamics |

Morning session: The market was clearly divided, and the real estate group began to surge.

The market continued to fluctuate and be clearly divided in the late morning session. At the midday break, the VN-Index lost 3.54 points, stopping at 1,310.92 points. Meanwhile, the HNX-Index regained green, up slightly by 0.11% to 216.55 points. The market breadth was quite balanced with 314 declining stocks and 300 gaining stocks.

Market liquidity improved significantly compared to the low level of the previous week. Trading value reached nearly 12 trillion dong on the HOSE and over 632 billion dong on the HNX, up 59% and 26%, respectively, compared to the previous session.

Source: VietstockFinance

|

In terms of impact on the index, VCB, BID, and VHM were the main pillars that put the most pressure on the VN-Index, taking away nearly 2 points. Meanwhile, GVR is holding the index from falling too sharply, contributing nearly 1 point increase.

The industry groups continued to fluctuate within a narrow range. Information technology was the group with the largest temporary decline of -0.7%, mainly affected by FPT (-68%) and CMG (-0.75%).

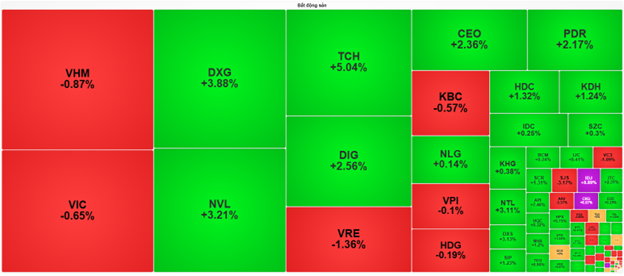

In the pillar industry groups, most of the financial stocks fluctuated slightly around the reference price, except for some stocks with significant volatility such as EIB (+2.57%), HDB (+1.58%), FTS (+2.05%), BVH (+2.92%), VAB (+5.22%), STB (-1.32%), and SSB (-1.34%). Meanwhile, the real estate sector index was slightly red due to pressure from the Vingroup trio, including VHM (-0.87%), VIC (-0.65%), and VRE (-1.36%). However, the rest of the industry traded brightly in the late morning session, with many stocks surging strongly such as NVL (+3.21%), TCH (+5.04%), DXG (+3.88%), DIG (+2.56%), PDR (+2.17%), CEO (+2.36%), and even IDJ and CKG hitting the ceiling price.

Source: VietstockFinance

|

Foreign investors increased selling pressure with a net sell value of nearly 370 billion dong on the three exchanges in the morning session. Among them, HPG was the most net sold stock with a value of over 81 billion dong. On the net buying side, VSC led with a value of over 58 billion.

10:35 am: Shifted to a tug-of-war after a sudden selling pressure

The market gradually stabilized and shifted to a tug-of-war around the reference price after a sudden selling pressure. The VN-Index decreased by 0.65%, indicating the current adjustment pressure and reflecting the caution of cash flow in the face of unpredictable developments.

The VN-Index is currently trading at 1,305.89 points, down 0.65%. The index representing the large-cap stock group, VN30, recorded a deeper decrease of 0.9% to 1,396.73 points, indicating that the pressure mainly came from blue-chip stocks. Meanwhile, the HNX-Index maintained a slight decrease of only 0.07% to 216.16 points. The division was also reflected in the capitalization-based indices: VS-LargeCap decreased by 0.7%, and VS-MicroCap decreased by 0.78%, while VS-MidCap recorded an increase of 0.2%, indicating that some mid-cap stocks are attracting cash flow.

Witnessing the adjustment pressure covering the VN30 basket. The market breadth leaned entirely towards the declining side with 25 decreasing stocks, while only 3 stocks increased and 2 stocks kept the reference price. The stocks with the most positive impact included HDB, contributing 0.42 points, GVR with 0.08 points, and BVH with 0.04 points. Conversely, the group of stocks with the most negative impact was VIC with 2.25 points, VHM with 1.86 points, HPG with 1.27 points, and FPT with 1.13 points. The downward trend is currently dominating the market.

Source: VietstockFinance

|

Looking at the overall picture of the industries, the market is facing significant pressure from the consumer services group, which decreased by 2.77%. The large-cap industries could not avoid the negative trend: Real estate decreased by 0.93%, credit institutions decreased by 0.58%, and financial services decreased by 0.72%.

On the other hand, some industries maintained green, notably media and entertainment with an increase of 1.35% and insurance with an increase of 0.78%. Transportation also recorded an increase of 0.42%.

Specifically, the credit institution group (accounting for 29.84% of market capitalization) decreased by 0.58% for the whole industry, with many large-cap stocks still facing selling pressure. Typical codes include TCB down 0.66%, MBB down 0.81%, VPB down 0.55%, CTG down 0.54%, STB down 1.20%…

Real estate (accounting for 15.82% of market capitalization) decreased by 0.93%. Codes such as NVL decreased by 0.96%, DXG decreased by 2.44%, KBC decreased by 1.93%, PDR decreased by 1.34%, TDC decreased by 1.87%, and LHG decreased by 1.84%.

The food, beverage, and tobacco industry (accounting for 8.96% of market capitalization) decreased by 0.31%. Notable codes include VNM down 0.60% and MSN down 0.14%.

In contrast, transportation (accounting for 7.23% of market capitalization) had a positive performance, increasing by 0.42%. Code PHP decreased by 0.27%, but other codes in the industry may be supporting the general uptrend, such as VOS hitting the ceiling price, GMD increasing by 3%, VSC increasing by 0.23%…

As of 10:30, the market breadth was clearly divided. Notably, more than 1,000 codes stood still, reflecting the prevailing wait-and-see attitude. The buying side recorded 17 ceiling-hitting codes, 228 increasing codes. On the opposite side, there were 335 decreasing codes and 6 floor-hitting codes, reflecting the existing selling pressure.

Source: VietstockFinance

|

Opening: Caution prevailed from the beginning of the session

The opening trading session this morning presented a rather positive picture of the market, with most of the main indices recording gains. Although the VN-Index only increased slightly, the indices on the HNX and UPCoM exchanges witnessed remarkable breakthroughs, reflecting the spread of cash flow to mid-cap and small-cap stocks. The VN-Index opened up 0.03% to 1,314.89 points, indicating a cautious start for the overall market. Meanwhile, the HNX-Index performed strongly with a gain of 0.31% to 216.99 points.

The VN30 basket started with a dominant red backdrop. The market breadth showed 18 decreasing stocks, outperforming 11 increasing stocks and 1 stock keeping the reference price. On the supportive side of the index, HDB contributed the most positive impact with 0.50 points, followed by VNM with 0.37 points, SHB with 0.22 points, and VPB with 0.13 points. Conversely, the main pressure came from large-cap stocks. HPG was the most negative influence, reducing 1.01 points, followed by VIC with 0.81 points, MWG with 0.64 points, and STB with 0.58 points. This dynamic reflected the prevailing caution from the beginning of the session.

Overall, the stock market recorded an increase of 0.21% across all 1,613 trading codes. Industries with large contributions to market capitalization, such as credit institutions (accounting for 29.84% of market capitalization), maintained a slight increase of 0.10%, indicating the stability of this pillar group. Conversely, the real estate industry, with 15.82% of market capitalization, recorded a decrease of 0.12% in the industry index. However, many large-cap and liquid real estate stocks rose, including VHM up 1.02%, VIC up 1.08%, TCH up 1.33%, NVL up 0.40

What’s Capturing the Attention of Stock Investors?

The VN-Index is inching closer to its 2025 peak after three consecutive weeks of gains. The looming profit-taking pressure could trigger short-term market volatility. Next week, investors’ eyes will be glued to news of potential tariff negotiation support between Vietnam and the US, which could provide a fresh impetus for the market.

The Expert’s Take: A Tactical Pause is a Prelude to the Next Wave

Short-term investors need to exercise caution and adopt a prudent stance. It is wise to maintain a sensible equity allocation and refrain from chasing stocks that have already surged.

Market Pulse for May 26: A Tale of Two Markets as Real Estate Sector Steals the Show

The market remained volatile and highly divided during the morning session. By the midday break, the VN-Index had shed 3.54 points, settling at 1,310.92. Conversely, the HNX-Index rebounded into positive territory, edging up 0.11% to 216.55. The market breadth was relatively balanced, with 314 decliners outweighing 300 advancers.

“Market Trends Analysis for May 26: Uncertainty Prevails”

The VN-Index and HNX-Index experienced a tug-of-war session in the morning trade, with a significant spike in liquidity, indicating investors’ cautious sentiment.

Market Beat: The Tug-of-War Begins as Sellers Step In.

The market steadies and shifts to a tug-of-war around the reference point after a sudden surge of selling pressure. VN-Index’s 0.65% dip indicates an impending adjustment, reflecting investor caution amidst unpredictable dynamics.

{kind=link}