Market liquidity increased from the previous trading session, with the VN-Index matching volume reaching over 453 million shares, equivalent to a value of more than VND 10.5 trillion; The HNX-Index reached over 39.5 million shares, equivalent to a value of more than VND 710 billion.

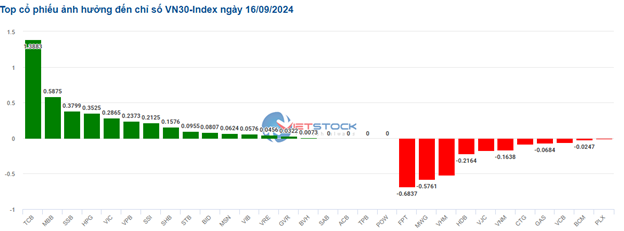

The red color continued to dominate the afternoon session despite the presence of buying power, which was still unable to withstand the strong selling pressure causing the VN-Index to plunge and close with a rather pessimistic investor sentiment. In terms of impact, VCB, VHM, GAS, and VIC were the codes with the most negative impact, taking away more than 4.2 points from the index. On the contrary, NAB, GVR, KDH, and BMP were the codes with the most positive impact, but the impact was insignificant.

| Top 10 stocks with a strong impact on the VN-Index on 09/16/2024 (in points) |

Similarly, the HNX-Index also had an unoptimistic performance, with the index negatively impacted by the KSV (-3.78%), MBS (-2.56%), IDC (-1.03%), and PVS (-0.99%) codes…

|

Source: VietstockFinance

|

The telecommunications sector had the largest decrease in the market at -2.45%, mainly from the VGI (-2.09%), VNZ (-14.99%), CTR (-0.8%), and ELC (-0.83%) codes. This was followed by the real estate and information technology sectors, which decreased by 1.48% and 1.42%, respectively.

In terms of foreign trading, this group returned to net buying of more than VND 140 billion on the HOSE floor, focusing on TCB (VND 69.94 billion), NAB (VND 53.87 billion), FPT (VND 53.23 billion), and VNM (VND 44.08 billion) codes. On the HNX floor, foreigners net bought more than VND 31 billion, focusing on PVS (VND 30.6 billion), TNG (VND 10.29 billion), TIG (VND 2.35 billion), and TVC (VND 1.09 billion) codes.

| Foreign net buying and selling dynamics |

Morning session: Selling pressure increases, VN-Index turns down

The market recorded a positive start to the session with more than 3 points gained. However, selling pressure soon emerged and intensified, causing difficulties for the market. At the end of the morning session, the VN-Index returned to a loss of 4.62 points, temporarily stopping at 1,214.09 points; The HNX-Index lost 0.96 points, falling to 231.46 points.

At the end of the morning session, the market liquidity was rather weak, with the VN-Index matching volume reaching just over 204 million units, equivalent to a value of VND 4.7 trillion. The HNX-Index recorded a meager volume of over 18 million units, with a value of VND 286 billion.

In terms of impact, VHM, CTG, and GAS are putting the most negative pressure on the VN-Index, taking away more than 1.6 points from the index. On the opposite side, a group of bank stocks, including TCB, SSB, and NAB, are the driving force supporting the index, contributing more than 1 point.

The industry groups are witnessing a mixed performance. On the positive side, the materials sector is the brightest spot in the market. Within this group, chemical stocks maintained their gains until the end of the morning session, up 0.21%. Stocks that increased by more than 1% included BMP (+2.59%), APH (+3.69%), DPM (+1.27%), and AAA (+1.13%). However, due to their low capitalization, they were unable to attract widespread buying interest.

In contrast, the telecommunications sector is currently at the bottom of the table with a decrease of 1.25%, mainly pressured by stocks such as VNZ, which fell by more than 7%, STC, which fell by more than 5%, and EBS, which fell by nearly 10%. Stocks like FOX, FOC, and TTN recorded decreases of more than 1%. The majority of the remaining stocks only fluctuated slightly around the reference price.

10:35 a.m.: Leaning towards the upside

Investors’ cautious sentiment still exists, leading to the main indices’ inability to break out and continue to fluctuate with a slight advantage towards the buying side. The VN-Index gained 1.46 points, trading around 1,253 points. The HNX-Index rose 0.2 points, trading around 232 points.

Most of the stocks in the VN30 basket turned positive. Notably, TCB, MBB, SSB, and HPG contributed 1.39 points, 0.59 points, 0.38 points, and 0.35 points to the VN30 index, respectively. On the other hand, FPT, MWG, VHM, and HDB were the stocks that continued to face selling pressure, taking away nearly 2 points from the index.

Source: VietstockFinance

|

The materials sector showed positive momentum from the start of the session. Within this group, fertilizer stocks stood out with DPM up 2.25%, DCM up 1.18%, and BFC up 2.11%… In addition, there were also representatives from the chemical group, such as DGC, which rose by 0.7%, and the steel group, with HPG up 0.4% and NKG up 0.48%.

From a technical perspective, DPM continues to trade sideways in the long term, and during the morning session of September 16, 2024, this stock witnessed a strong upward momentum, forming a Rising Window candlestick pattern with an increase in volume, indicating a rather optimistic investor sentiment.

In addition, DPM‘s price is testing the neckline of the Inverse Head and Shoulders pattern. If the recovery scenario is maintained in the future, the price target will be in the range of 41,500-42,500. Furthermore, the MACD indicator has given a buy signal after the Signal line cut up the MAD line, reflecting the positive outlook.

Source: https://stockchart.vietstock.vn/

|

Following this, the financial sector also contributed to the market’s upward momentum, although the performance was still mixed. Specifically, on the recovery side, SSI rose by 0.62%, TCB by 1.35%, MBB by 0.84%, and NAB by 3.94%… Meanwhile, SHB, TPB, VPB, and VND remained unchanged, while some stocks continued to face selling pressure, such as HDB, which fell by 0.57%, MSB by 0.44%, and CTG by 0.29%…

On the other hand, the telecommunications sector is experiencing contrasting performances, with selling pressure mainly focused on VGI, which fell by 0.64%, VNZ by 7.16%, LBE by 9.09%, and FOX by 0.89%…

Compared to the beginning of the session, the buying side still has a slight advantage. There were 359 stocks that increased and 212 stocks that decreased.

Opening: Indecisive sentiment remains

At the beginning of the September 16 session, as of 9:30 a.m., the VN-Index fluctuated around the reference level, reaching 1,250 points, with 10 stocks touching the ceiling price, 225 stocks increasing, 1,219 stocks standing at the reference price, 145 stocks decreasing, and 7 stocks touching the floor price.

At the Government Standing Committee meeting on September 15, Minister of Planning and Investment Nguyen Chi Dung stated that Storm No. 3 (Yagi) and its aftermath affected 26 northern provinces and Thanh Hoa province. These localities account for more than 41% of GDP and 40% of the country’s population.

In addition to human losses, according to the Ministry, Storm Yagi caused property damage of about VND 40,000 billion to people and the State. According to a report by the Ministry of Planning and Investment, about 257,000 houses, 1,300 schools, and many infrastructure works were collapsed or damaged, and 305 dyke incidents occurred, mainly on major dykes.

As of 9:30 a.m., the materials sector led the market with a positive performance from the start of the session. Typically, stocks such as DPM increased by 1.55%, DCM by 1.18%, HPG by 1%, NKG by 0.95%, HSG by 0.75%, CSV by 0.13%,…

Next was the industrial group, with most stocks in this group recording positive performances. Specifically, PC1 rose by 0.87%, VCG by 1.1%, BCG by 0.94%, DGT by 3.03%, NHH by 1.41%,…

The Year-End Wave: Riding the Stock Market Surge

The domestic stock market lull presents an opportunity to accumulate stocks.

The Stock Market ‘Anticipates’ Next Week’s Key Event

The market experienced a rather dull trading week, with the last two sessions seeing the lowest liquidity since April 2023. Investor sentiment seems to be heavily impacted by the aftermath of the third storm, which disrupted the business operations of a significant number of enterprises. The market is also awaiting the response of the State Bank of Vietnam following the interest rate cut by the Federal Reserve.

{kind=link}