: The Shockwave Continues")

: A Mixed Bag of Wins and Woes")

I. MARKET DEVELOPMENT OF WARRANTS

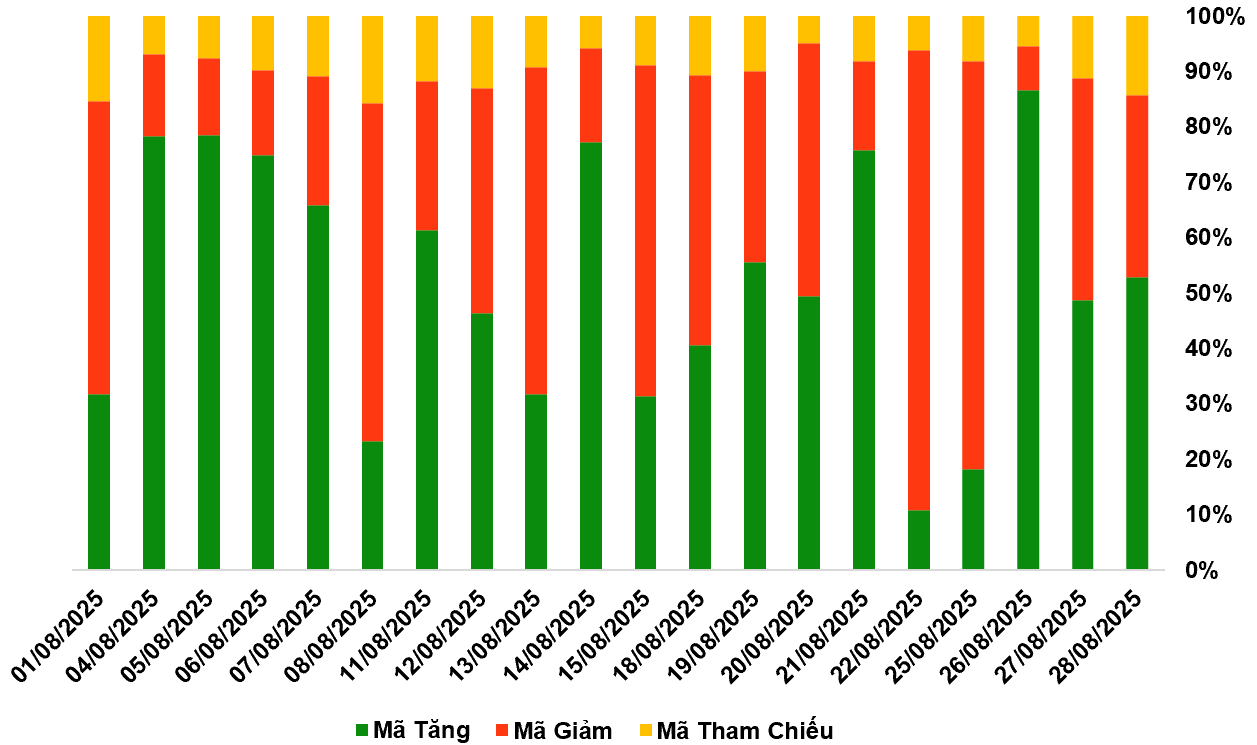

As of the close of the trading session on August 28, 2025, the market witnessed 137 advancing codes, 85 declining codes, and 37 reference codes.

Market breadth over the last 20 sessions. Unit: Percentage

Source: VietstockFinance

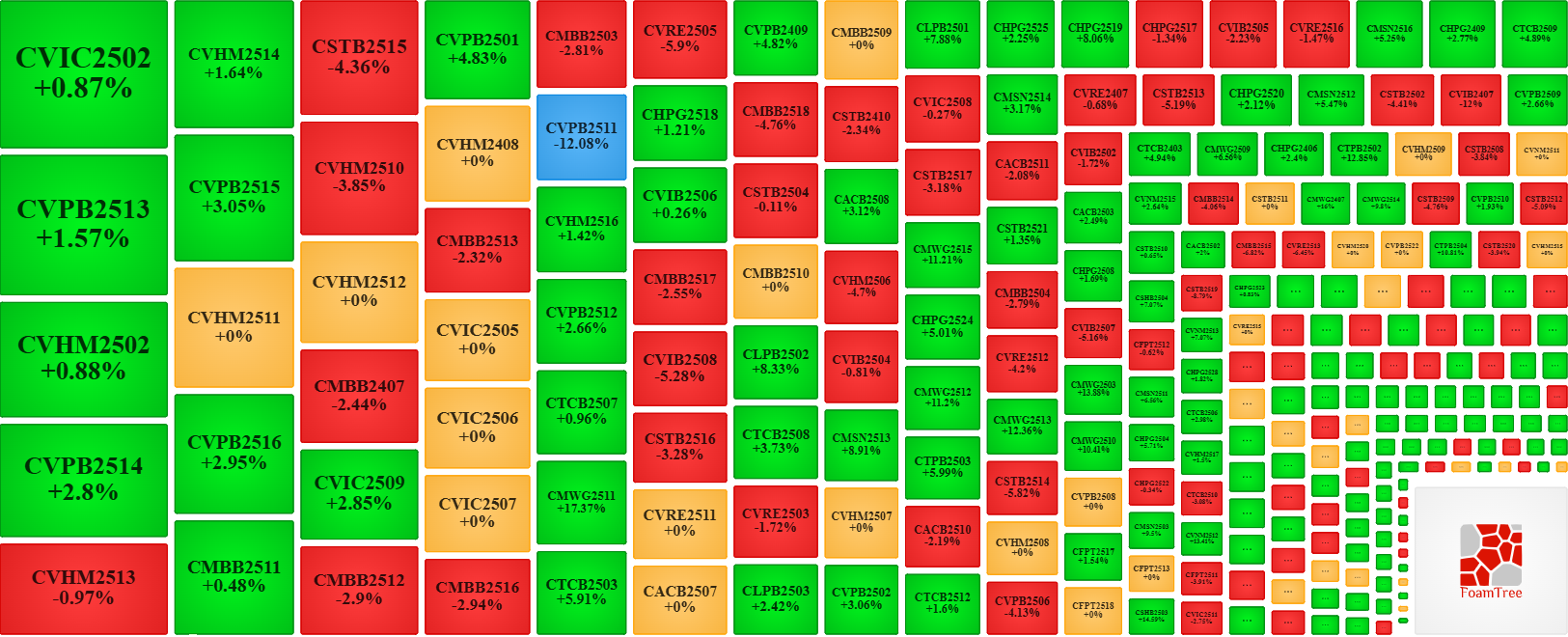

During the trading session on August 28, 2025, buyers continued to lead the market, causing most of the warrant codes to increase in price. Specifically, the large codes in the increasing group were CVPB2513, CVHM2502, CMBB2511, and CVIC2502.

Source: VietstockFinance

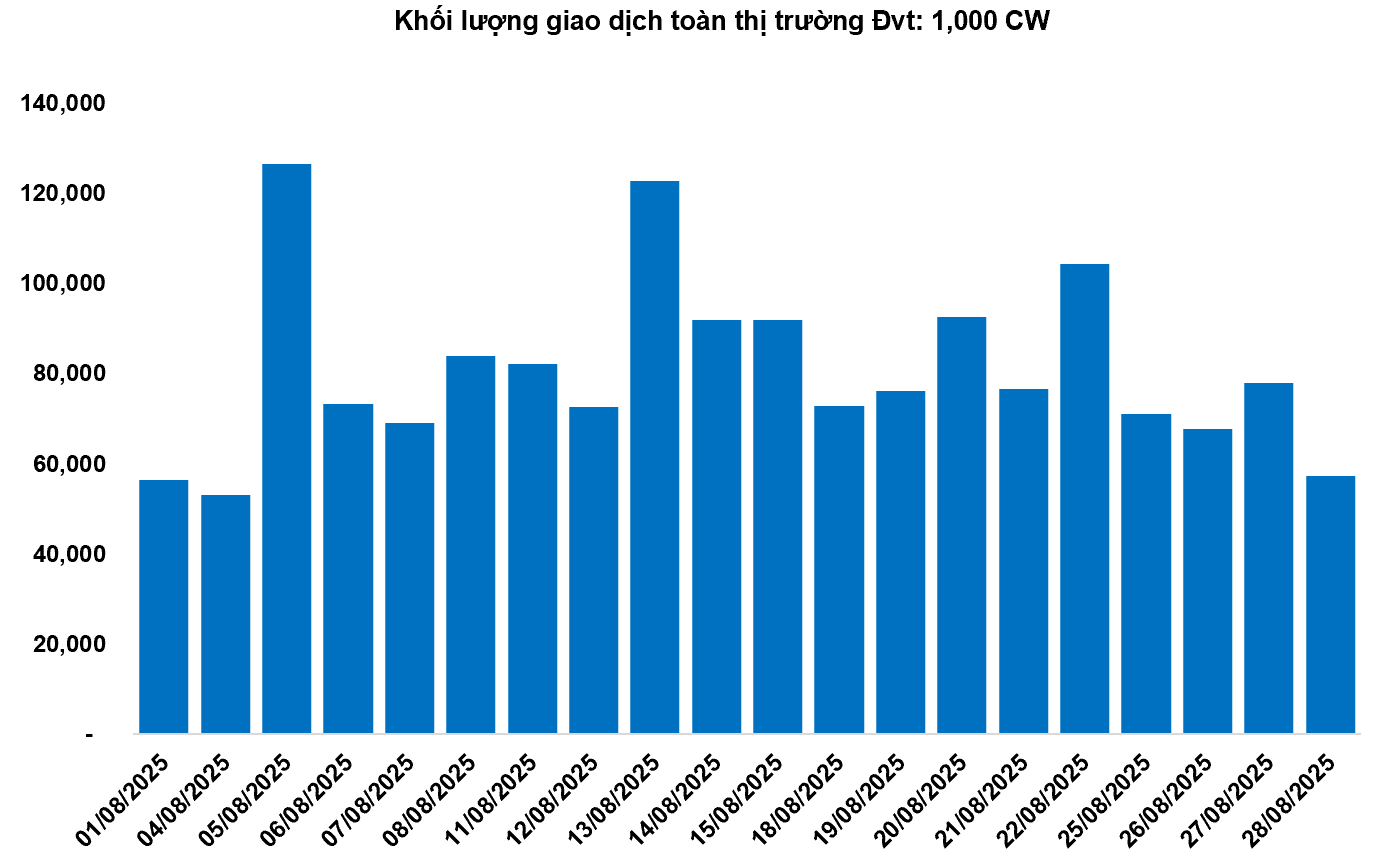

The total market trading volume in the August 28 session reached 57.31 million CWs, down 26.34%; the trading value reached VND 140.07 billion, down 27.22% compared to the previous session. Of which, CHPG2406 was the code leading the market in volume with 2.31 million CWs; CTPB2503 led in trading value with VND 7.09 billion.

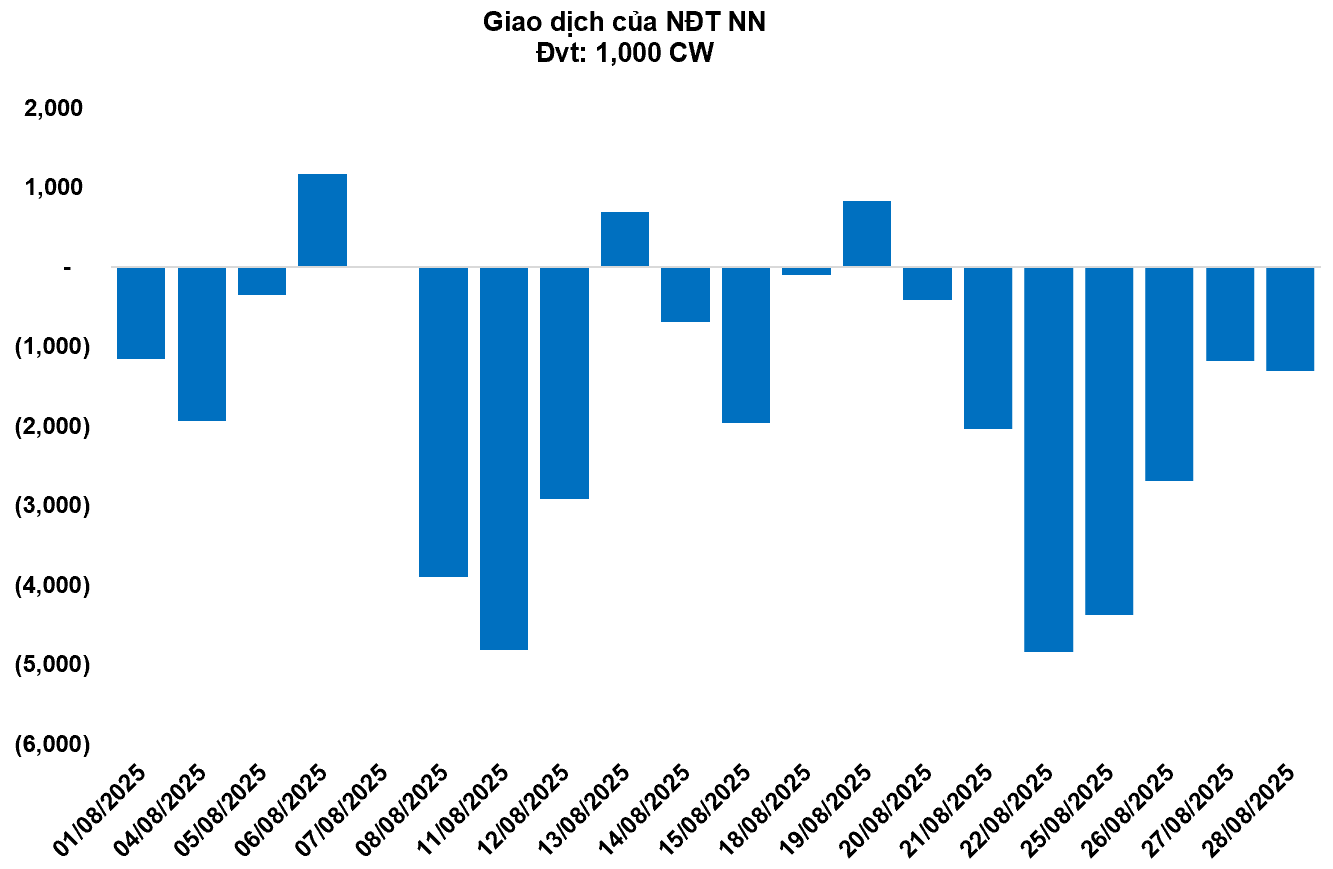

Foreign investors continued to net sell in the August 28 session with a total net selling volume of 1.32 million CWs. In particular, CHPG2513 and CHPG2515 were the two codes that were net sold the most.

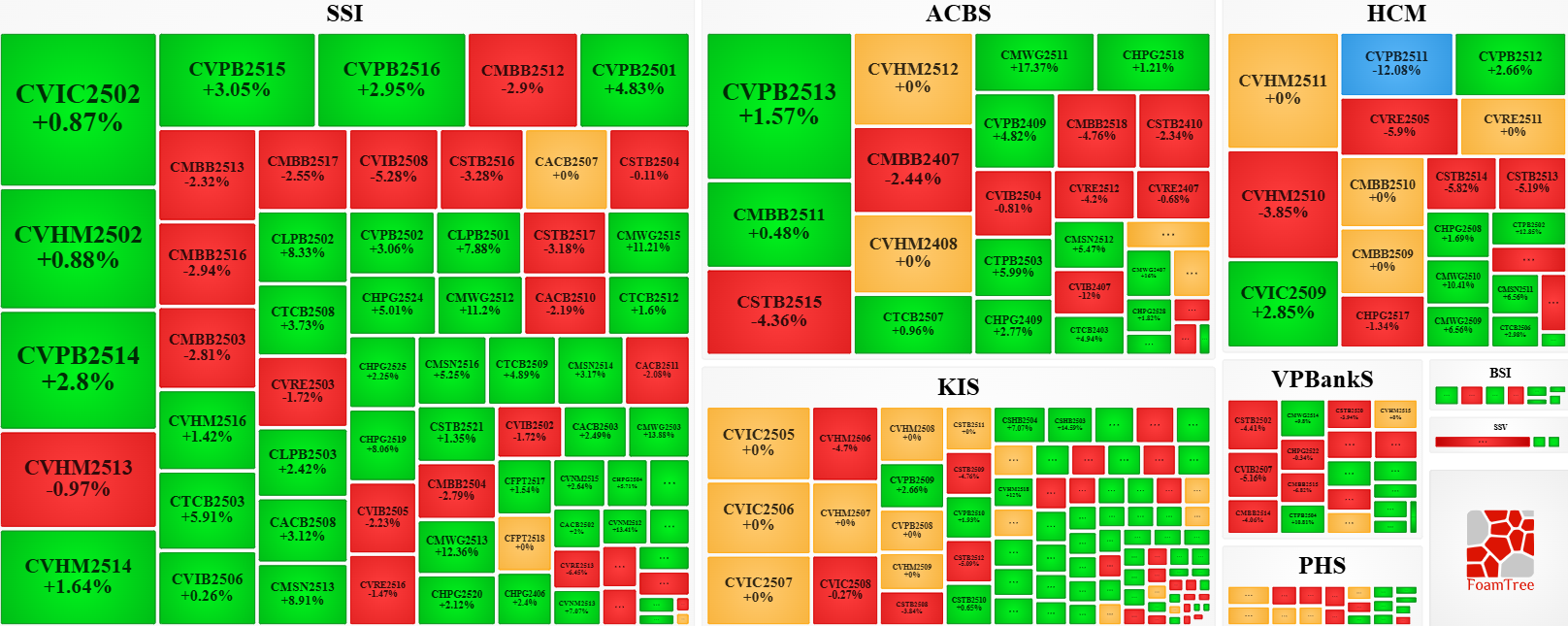

Securities companies SSI, ACBS, HCM, KIS, and VPBankS are currently the organizations with the most issued warrant codes in the market.

Source: VietstockFinance

II. MARKET STATISTICS

Source: VietstockFinance

III. WARRANT VALUATION

Based on the valuation method suitable for the starting point of August 29, 2025, the reasonable prices of the warrants currently traded in the market are as follows:

Source: VietstockFinance

Note: The opportunity cost in the valuation model is adjusted to suit the Vietnamese market. Specifically, the risk-free bill interest rate (government bills) will be replaced by the average deposit interest rate of large banks with term adjustments suitable for each type of warrant.

According to the above valuation, CVHM2515 and CVHM2508 are currently the two warrant codes with the most attractive valuations.

The higher the effective gearing ratio of a warrant code, the greater its increase/decrease relative to the underlying stock. Currently, CHPG2512 and CVNM2512 are the two warrant codes with the highest effective gearing ratios in the market.

Economics & Market Strategy Analysis Department, Vietstock Consulting Department

– 18:58 28/08/2025

The Warrant Market on August 28, 2025: A Mosaic of Green and Red

The trading session on August 27, 2025, concluded with a mixed performance across the market. Out of all the stocks traded, there were 126 gainers, 104 losers, and 29 stocks that remained unchanged. Foreign investors continued their net-selling trend, offloading a total of 1.18 million covered warrants.

The Ultimate Guide to Reaching New Heights: Vietstock Daily 27/08/2025

The VN-Index demonstrated resilience by maintaining its position above the middle of the Bollinger Bands, and its impressive recovery was highlighted by a surge of nearly 54 points. To ensure a more sustainable upward trajectory, an improvement in trading volume is necessary. If the index surpasses the previous peak of 1,680-1,693 points in upcoming sessions, it will pave the way for reaching new heights.

The Warrant Market on August 27, 2025: Is the Outlook Less Grim?

The trading session on August 26, 2025, concluded with a positive note for the market, witnessing 224 advancing stocks, 21 declining stocks, and 14 stocks remaining unchanged. Foreign investors continued their net-selling trend, offloading a total of 2.69 million covered warrants.

“Warrants Market Update for August 26, 2025: Foreign Investors Continue Selling Streak”

The market closed on August 25, 2025, with a mixed performance. Out of all the stocks traded, 47 advanced, 191 declined, and 21 remained unchanged. Foreign investors continued to offload their positions, resulting in a net sell-off of 4.38 million covered warrants.

The Warrant Market Week of August 25-29, 2025: Ablaze with the Underlying Market

The trading session on August 22, 2025, concluded with a mixed performance across the market. Amidst a sea of 243 stocks, 28 emerged victorious with upward trends, while 215 succumbed to downward pressures. The remaining 16 stocks remained unchanged, serving as a stalwart anchor in this tempestuous market climate. Foreign investors maintained their cautious stance, offloading a net sell-off of 4.84 million covered warrants.

{kind=link}