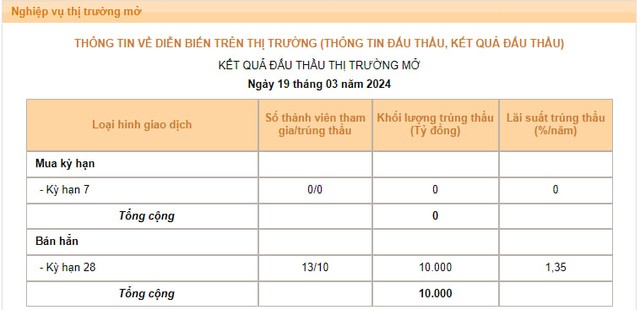

After 6 consecutive sessions maintaining at nearly 15,000 billion dong, the amount of bonds issued by the State Bank in the session on March 19 decreased to 10,000 billion dong, and the winning interest rate also decreased from 1.4% to 1.35%.

The decreasing trend of the winning volume and the winning interest rate shows that the State Bank is no longer too determined in its liquidity withdrawal activities.

Source: SBV

As we reported earlier, the State Bank had resumed the bond sale since the session on March 11 after more than 4 months of suspension. After 7 consecutive bond issuance sessions, the State Bank had withdrawn nearly 100,000 billion dong from the banking system. This is the amount of money that is not circulating in the economy and will be injected back into the system from April 8.

The restart of the bond sale activities shows the orientation of reducing the excess liquidity in the banking system by the Administrator, thus pushing up the VND interest rate in the interbank market, indirectly restraining the momentum of the USD/VND exchange rate – which is currently under pressure and is trading at a record high level.

Meanwhile, the interbank market interest rates have reversed down in the last 2 trading sessions. According to the latest figures released by the State Bank, the average VND interbank overnight interest rate (the main term accounting for about 90% of transaction value) has decreased to 0.79% in the session on March 15, from 1.21% recorded in the session on March 14, and 1.47% in the session on March 13.

Interest rates for other key terms also tend to decrease, such as: 1-week term decreased from 1.68% to 1.1%; 2-week term decreased from 1.81% to 1.43%; 1-month term decreased from 2.01% to 1.6%.

In addition, even though the State Bank had withdrawn a total of 100,000 billion dong, the USD exchange rate at commercial banks still continues to stay at a historic high level, 24,900 – 25,000 dong at the selling side.

The decrease in interbank interest rates, together with the number of bidders for bond auctions still at a relatively high level reflecting that the system liquidity is still quite abundant. This, together with the existing exchange rate pressure, will stimulate the possibility of the State Bank continuing to issue more bonds in the upcoming trading sessions.

Looking back at the most recent bond issuance period, 21/9-8/11/2023, the State Bank had issued bonds in 35 consecutive sessions with a total volume of 360,345 billion dong. In which, the highest net withdrawal (the cumulative volume of issued bonds – the cumulative volume of matured bonds) in this period was 255,600 billion dong.

After the State Bank had withdrawn money, the exchange rate started to decrease and continued to decline until the end of November 2023. The interbank overnight interest rate increased sharply to over 2% in the period from 21/9 – 25/10/2023 – in response to the withdrawal of money. The State Bank stopped issuing bonds from the session on November 9, 2023 when the exchange rate began to cool down and gradually pumped back the withdrawn amount into the system before that.

According to the assessment of SSI Securities Company in the latest currency market report, the purpose of issuing bonds by the State Bank is to absorb excess liquidity in the secondary market to reduce exchange rate speculation pressure in the short term and limit the impact on interest rates in the primary market.

Analysts believe that the bond issuance move by the State Bank can be seen as a way to adjust short-term liquidity in the system and is a common practice for central banks. SSI also affirmed that the above action does not mean that the State Bank has reversed its monetary policy.

However, SSI also warns that with the continued strong pressure on the exchange rate in the international market, the State Bank may have to take stronger measures, including considering increasing the bond term or inspecting currency trading at commercial banks.

With a relatively abundant system liquidity (credit in the first 2 months of the year decreased by 0.72% compared to the end of 2023), SSI predicts that the State Bank can continue to maintain this activity for at least the next 2 weeks.

If maintaining the current bond issuance rate (15,000 billion dong / session), analysts estimate that the total net withdrawal volume in this period is about over 200,000 billion dong, similar to the end of 2023.

In a new analysis report, BSC also stated that the bond net withdrawal is a regulatory tool and does not imply a reversal of policy. The short-term goal when the State Bank issues bonds is to regulate short-term liquidity in the market to impact the exchange rate. In the long term, the issuance of bonds to stabilize the exchange rate, interest rate, liquidity,… serves the long-term objectives of the monetary policy.

Prior to this, during the period from 2018-2023, the State Bank had regularly carried out this operation several times a year. Statistics from BSC show that the State Bank had carried out an average net withdrawal about 9.7 times per year in this period, with the number of days from the beginning of the cycle to the end of the cycle on average/session is about 13.4 days. The average net withdrawal value per cycle is 43,385 billion dong. The largest net withdrawal value per cycle was 191,100 billion dong in 2022.

With the above assessments, BSC estimates that the largest net withdrawal scale (the cumulative volume of issued bonds – the cumulative volume of matured bonds) in this period may be about 150,000 billion dong.

With Reference Price of VND 81.8 Million/Tael")

{kind=link}