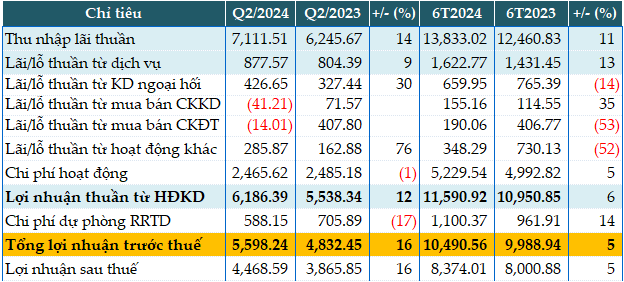

ACB reported a strong second quarter of 2024, with net interest income reaching 7,112 billion VND, a 14% increase year-over-year. The bank saw growth in non-interest income, including a 9% rise in service fees, a 30% jump in foreign exchange trading profits, and a 90% surge in other operating income. However, investment and trading securities reported losses compared to profits in the same period last year.

Additionally, a 17% reduction in credit risk provisions to just over 588 billion VND boosted pre-tax profits to over 5,598 billion VND, marking a 16% increase year-over-year.

For the first half of 2024, ACB achieved 11,590 billion VND in net operating income, a 6% increase year-over-year. The bank increased its risk provisions by 14% to 1,100 billion VND, resulting in a pre-tax profit of nearly 10,491 billion VND, a 5% rise.

With these results, ACB has accomplished 48% of its full-year 2024 target of 22,000 billion VND in pre-tax profits. The ROE ratio remains steady at 23.4%.

|

ACB’s Q2 2024 Financial Results. In VND billion

Source: VietstockFinance

|

As of June 30, 2024, ACB’s total assets grew by 7% since the beginning of the year, reaching 769,678 billion VND. Meanwhile, deposits with the State Bank decreased by 15% to 15,724 billion VND, and deposits and loans with other credit institutions dropped by 8% to 105,419 billion VND.

Notably, customer loans saw a significant increase of 13% since the start of the year, totaling 550,172 billion VND. ACB attributed this growth to its balanced approach, targeting both individual and corporate segments, which grew by over 12% compared to the beginning of the year. Customer deposits also rose by 6% to 511,696 billion VND during the same period, with a CASA ratio of 22%.

|

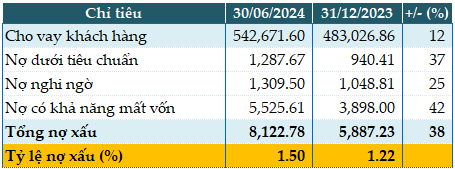

ACB’s Loan Quality as of June 30, 2024. In VND billion

Source: VietstockFinance

|

Excluding the 7,500 billion VND in margin loans from ACBS, ACB’s total non-performing loans as of June 30, 2024, stood at 8,123 billion VND, a 38% increase since the beginning of the year. The NPL ratio slightly increased from 1.22% to 1.5%, influenced by market conditions and the impact of CIC-related loans. The LDR ratio was 82.2%, and the ratio of short-term capital used for medium and long-term loans was 17.6%.

Han Dong

Banking: Huge Profits Yet Worried

Several banks have announced their 2023 financial results, showing outstanding growth. However, they are also facing increased pressure in setting aside provisions for credit risk.

Novaland reports over VND 1,600 billion in profit for Q4/2023, bond debt reduced by VND 6,000 billion in one year.

In 2023, Novaland achieved a profit of over 800 billion VND, in contrast to the first half of the year when the company incurred a loss of over 1,000 billion VND.

{kind=link}