Reports 70% Surge in Q3 Profits, Partners with Energy Giant in Oil & Gas Sector")

With a large number of shares circulating on the stock exchange in the non-financial group (approximately 6.4 billion units) and a high free-float rate, Hoa Phat (HPG) has long been considered a national stock with very vibrant trading activities. However, in the eyes of foreign investors, the leading steel stock doesn’t seem particularly appealing recently.

Foreign investors have just heavily sold HPG on the first trading session of September, thereby extending the net selling streak to 21 consecutive sessions. Since the beginning of August, foreign investors have net sold a total of more than 100 million HPG shares, equivalent to a value of nearly VND 2,500 billion. This is a record number in recent years for Hoa Phat alone. In the past month, no stock on the exchange has been net sold more heavily by foreign investors than HPG.

Earlier, in late June, more than 581 million bonus HPG shares issued by Hoa Phat to shareholders at a ratio of 10% were traded after being listed additionally. With the ownership ratio of foreign investors accounting for about 1/4 of the charter capital, it is estimated that foreign investors received about 130 million HPG shares from this issuance. It is likely that the supply of HPG shares in the past time came from this action.

Pressure from foreign investors pushed the HPG stock back to the lowest price range since the beginning of the year. Compared to the 28-month peak reached in mid-June, the stock has fallen by nearly 15%. The corresponding market capitalization reached VND 161,500 billion (~USD 6.5 billion). This figure caused Hoa Phat to drop out of the top 10 most valuable enterprises on the Vietnamese stock exchange.

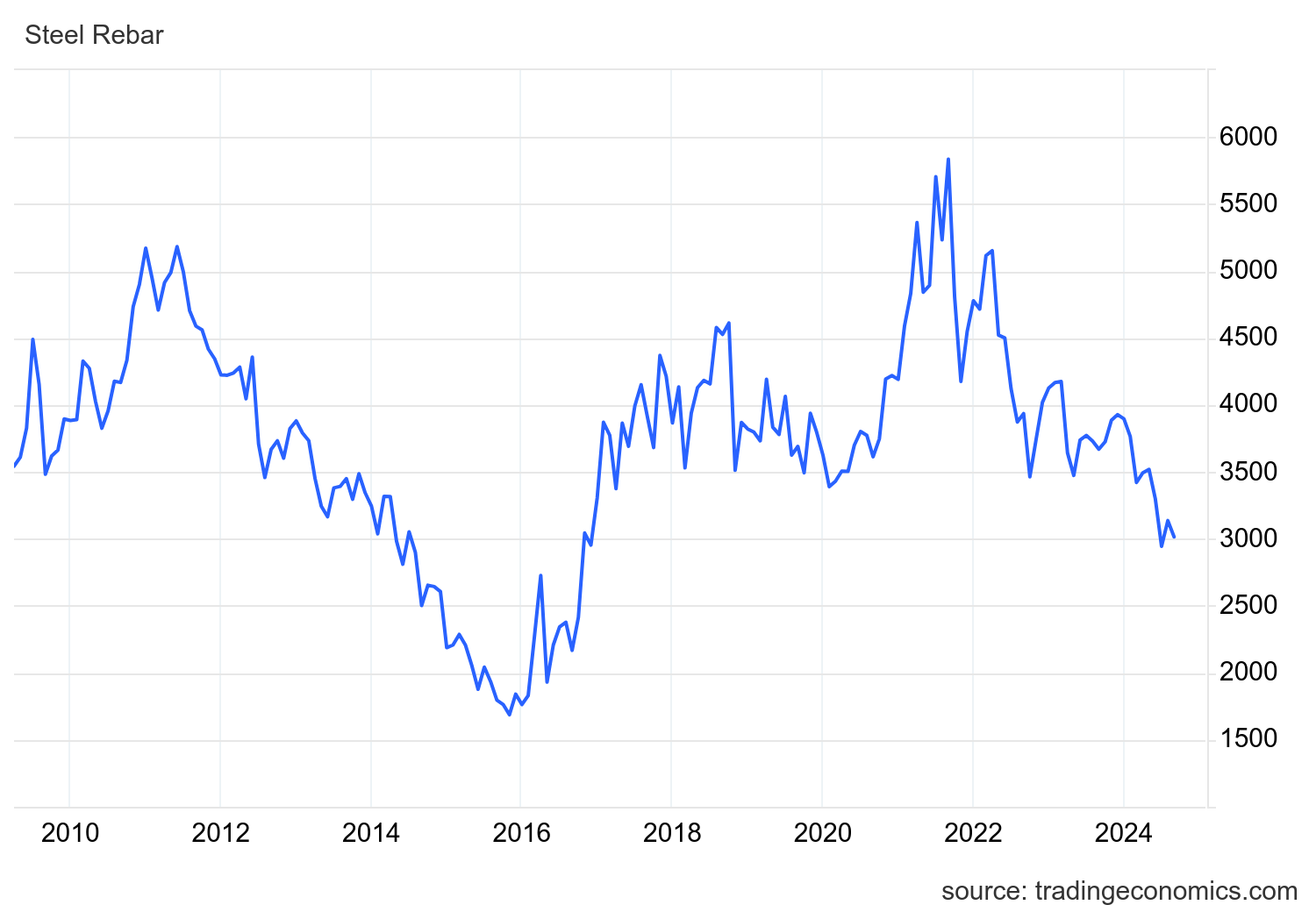

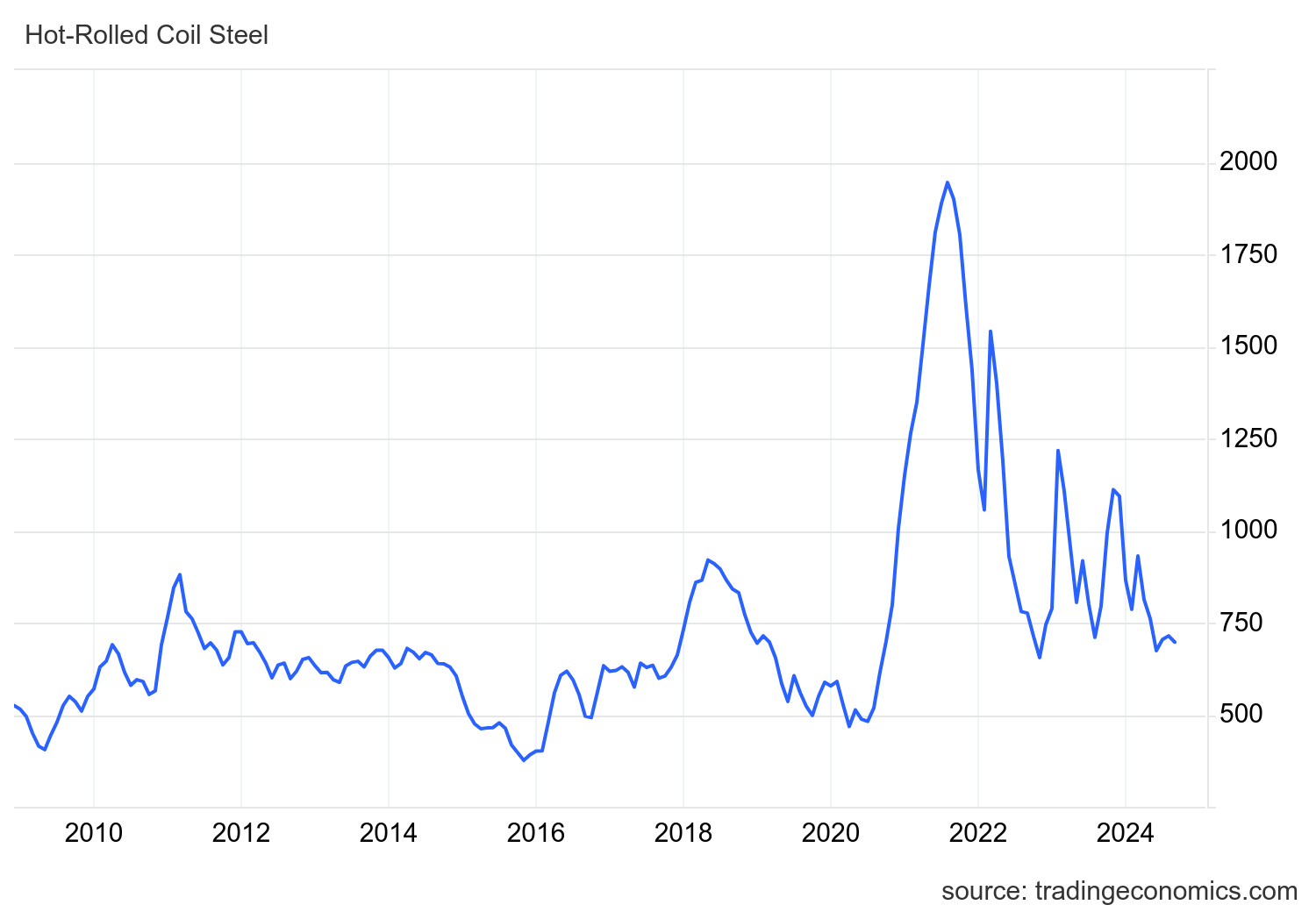

Foreign investors are putting pressure on HPG stock while the global steel industry is going through a “harsh winter” and Hoa Phat, along with domestic steel producers, cannot avoid being affected. Rebar steel futures prices have fallen to around CNY 3,000 per ton, the lowest level in eight years since 2016. Similarly, HRC prices have also fallen to a four-year low of less than $700 per ton.

Steel prices worldwide ended their rapid rebound and continued to fall sharply after China’s official manufacturing PMI unexpectedly fell to 49.1 in August, recording the sharpest decline since the beginning of the year. In addition, the construction PMI of the National Bureau of Statistics of China (NBS) also fell to 50.6, recording the weakest activity growth since data collection began in 2020.

The indexes indicate a decline in the outlook for steel demand in China. This is in line with the housing over-supply crisis in China as the country wants to reduce its dependence on metal-intensive industries. Chinese mills have turned to overseas customers to make up for weak domestic demand. This has added further downward pressure on prices.

In this context, domestic steel companies like Hoa Phat are awaiting a decision from the Ministry of Industry and Trade regarding anti-dumping (AD) investigations to hopefully ease some of the pressure on the domestic market. The focus of the investigations is on imported HRC from China and India and galvanized steel from China and the Republic of Korea.

However, during the waiting period, the Vietnamese steel industry has repeatedly received bad news as the European Commission (EC) and the Directorate General of Trade Remedies of India (DGTR) have successively announced the initiation of anti-dumping investigations on certain hot-rolled steel products originating from or exported from Vietnam.

Profits may grow strongly

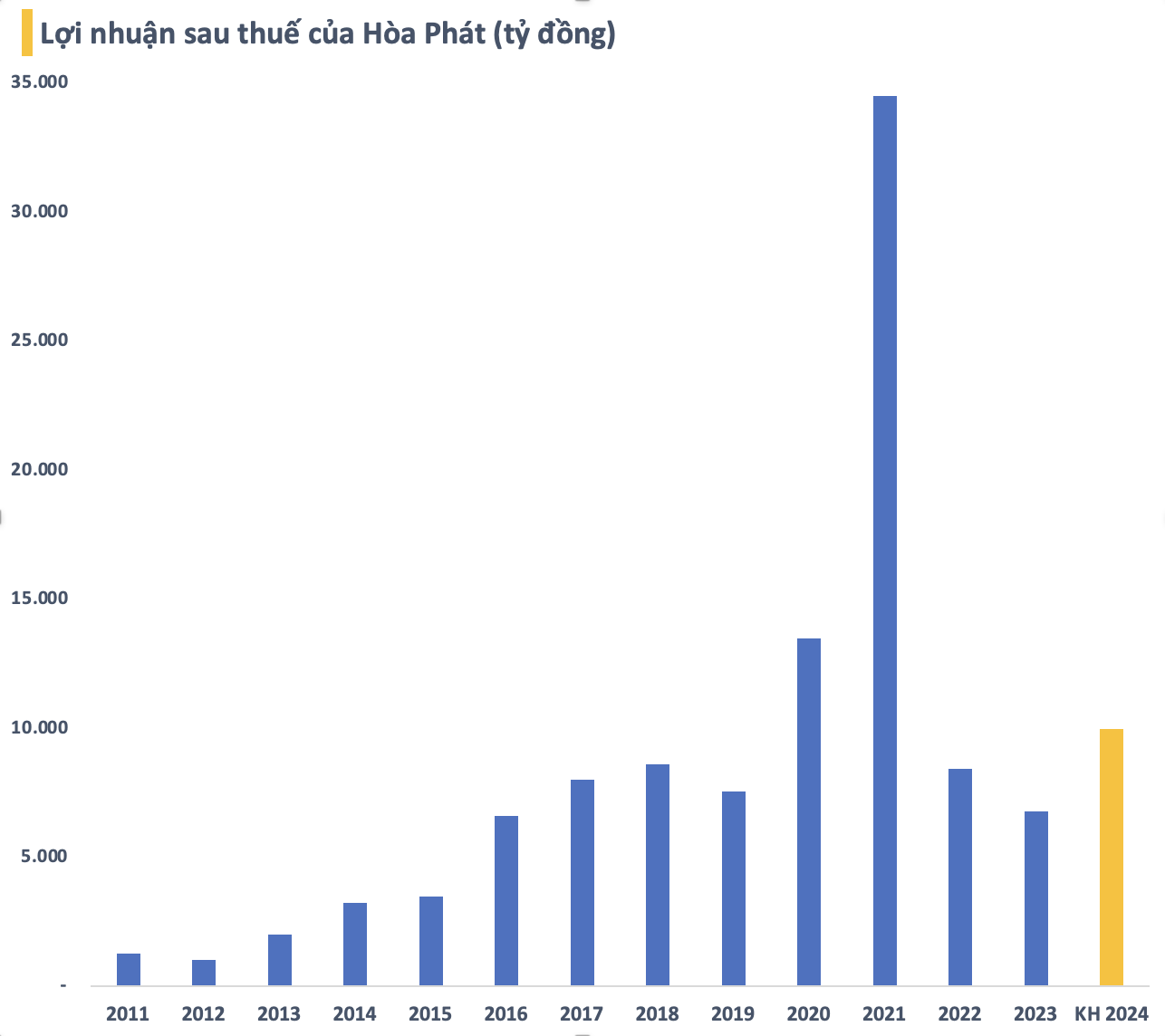

Although the trend of world steel prices is unfavorable, Hoa Phat’s profits are still expected to grow strongly in 2024 on a low comparative basis last year. In a recent report, VDSC projected Hoa Phat’s net profit to reach VND 12,000 billion, up 77% over the same period last year.

VDSC expects the domestic steel market to continue to maintain its recovery momentum and support the company’s sales volume in the second half of 2024. Especially when construction activities are promoted, the real estate market recovers more strongly, along with the peak construction season in Q4. In addition, the company will proactively switch HRC orders to serve the needs of domestic galvanized companies when Europe conducts anti-dumping investigations.

Previously, SSI Research’s report in early August also projected Hoa Phat’s net profit in 2024 to reach VND 12,800 billion, up 87% over the same period in 2023. The analysis department forecasts Hoa Phat’s construction steel and HRC output to reach 4.5 million tons and 3.05 million tons, respectively, up 17.6% and 10% over the same period last year. If the projections are accurate, Hoa Phat will exceed its 2024 profit plan (VND 10,000 billion).

Regarding the progress of the Hoa Phat Dung Quat 2 integrated steel production complex project, Mr. Mai Van Ha, Director of Hoa Phat Dung Quat Steel, said that the project has currently completed 80% of the progress of phase 1 and 50% of phase 2. It is expected that phase 1 will complete the installation of equipment for the hot-rolled steel production line in mid-September 2024, and then the company will proceed with cold testing and equipment calibration. According to the current progress, phase 1 is expected to have the first hot test product at the end of 2024.

VDSC assesses that the project’s construction progress is in line with expectations and Dung Quat 2 may start to generate commercial products to recognize revenue in Q1/2025. The plant is expected to operate at a relatively high efficiency in 2025 (80% for phase 1, equivalent to 2.2 million tons), corresponding to HPG’s HRC output in 2025 which can reach 5 million tons, up 67% over the same period and meet about 40% of Vietnam’s HRC demand.

“Positive Growth, Wood Industry Seizes Opportunity to Conquer $15.2 Billion Target”

The road to achieving the timber and forest product export target of $15.2 billion by 2024 will be challenging, according to experts. They believe that the industry will face numerous obstacles and require a concerted effort from businesses within the sector to overcome these hurdles.

{kind=link}