Marking the Fed’s Policy Reversal

In September, a positive macroeconomic context and progress towards meeting FTSE Russell’s upgrade criteria could serve as catalysts to maintain the recovery momentum and resume the upward trend in the Vietnamese stock market.

The focus of global investors will be on the FOMC meeting taking place from September 17-18, as the Fed is likely to end its monetary tightening period with a decision to cut interest rates for the first time in four years.

A 25-basis point cut is the base-case scenario, but the probability of a 50-basis point cut has increased significantly after some less-than-optimistic economic data, according to the CME FedWatch. Additionally, the BOJ’s interest rate decision meeting on September 20 also warrants attention.

A rate hike decision or a hawkish message about the potential for rate increases in the remainder of the year could further weaken the US dollar. A weak US dollar trend would create a favorable environment for policymakers to implement supportive policies to maintain low-interest rates, stimulate investment and consumption, and contribute to high economic growth (6-7%) in the context of significant fiscal and monetary room for the rest of the year.

According to estimates, disbursed investment capital reached 31.6% of the yearly plan, with an additional VND 530 trillion disbursed. Meanwhile, credit in the first eight months of 2024 increased by 6.25% since the beginning of the year, and an additional VND 1,000 trillion could be injected into the economy to achieve the 15% target.

Vietnam remains on the watchlist for a potential upgrade to secondary emerging market status by FTSE Russell in its annual September review. Compared to the closest evaluation, relevant authorities have made practical efforts to remove obstacles and promote the development of the stock market with the goal of upgrading, typically the State Securities Commission (SSC)’s publication of the Draft Circular amending and supplementing solutions to allow foreign institutional investors to buy securities without the need for 100% pre-funding and to provide foreign investors with equal access to information, thereby meeting the remaining two criteria for the upgrade as assessed by FTSE.

However, these solutions have not yet officially taken effect. Therefore, VDSC expects that FTSE Russell will likely make positive comments regarding the efforts of the management agencies in this review and that the chances of being approved for an upgrade in 2025 will be more feasible when the above-mentioned Circular is officially issued and foreign institutional investors have positive feedback during the use of the pre-funding solutions.

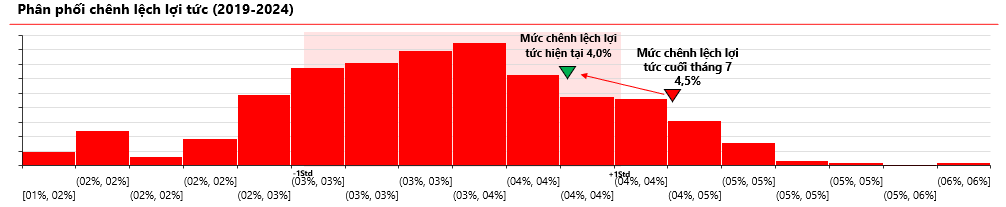

In terms of index levels, VDSC expects the VN-Index to trade within the range of 1,250 – 1,325 in September, bringing the yield gap between the stock market and the 10-year government bond to near the 5-year average of 3.6%, corresponding to a P/E of 15.2x. This is the level that the market has touched several times since the beginning of the year when the overall sentiment has maintained positive momentum.

Source: VDSC September 2024 Strategic Report

|

Macro Environment Suits Accumulation Investment

At the end of August, the State Bank of Vietnam (SBV) announced that it would adjust the credit growth limit for banks that have completed 80% of their 2024 credit growth target. This second adjustment of the credit growth limit by the SBV indicates a shift in monetary policy, and the cooling off of the DXY index has bolstered the SBV’s confidence in maintaining a supportive monetary policy environment.

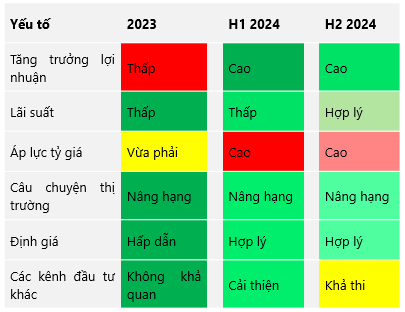

With the positive macroeconomic outlook, VDSC believes that the sideways-up trend of the VN-Index remains intact, and the range of 1,237 – 1,325 is considered a reasonable valuation for the index after reflecting the business results of the first half of 2024. This implies that investors can increase their stock allocation if the index falls below the lower bound and realize profits when the index rises to the upper bound.

With individual investors consistently net buying for nearly two years, the return of foreign investors will be the catalyst for the VN-Index to be re-rated.

VDSC maintains a positive view on stocks in the banking, industrial zone, food and beverage, consumer goods, industrial goods and services sectors.

Residential real estate, financial services, information technology, retail, utilities and energy, construction and building materials are also sectors that can be considered when the market price is reasonably discounted.

Source: VDSC September 2024 Strategic Report

|

The Foreign Sell-Off Continues: Over 300 Billion Dong Dumped on Two Blue-Chip Stocks in the Latest Trading Session

The foreign investors continued to net sell with a value of about VND 66 billion on the entire market.

The Unexpected Movement of the Stock Exchange’s ‘Most Expensive’ Shares

The VN-Index rebounded into the green today (September 12th), with the recovery’s momentum hinging on a select few stocks. Notably, VNG’s shares soared to the ceiling price after the company clarified Le Hong Minh’s current role within the organization.

{kind=link}