Today’s price action was interrupted by the patience of waiting liquidity, stifling any potential recovery. It was only when prices dipped significantly that larger waiting orders emerged. Following last weekend’s low-volume session, which could be seen as a positive sign as those most eager to cut their losses had already exited, liquidity remained very low.

The surprisingly positive macroeconomic data released over the weekend sparked some initial enthusiasm, but the flow of funds disagreed. Weak buying pressure quickly dampened the rally, and the market is now in the hands of sellers rather than buyers. Price negotiations will continue to create many sessions of range-bound trading, as seen today, with low volume until those holding funds become more aggressive.

Intraday fluctuations are creating a sense of frustration, as any upward movement is met with selling pressure. Only those holding stocks are feeling discouraged, while those holding funds are in a comfortable position. The market is still in the ‘test margin’ phase and has yet to test investors’ psychology. It will only transition to the bottom-building phase when stockholders lose interest in prices altogether.

Today’s session had two positive aspects. Firstly, liquidity; in a downward trend, slow trading after high-volume distribution and sharp declines is a good sign. It indicates either a reduction in selling pressure or a decrease in loose stocks. Today’s matched trading volume on the two exchanges was 11.5k billion, similar to mid-September levels. Secondly, there were many deep-catch orders placed at the end of today’s session. Whenever prices fell significantly, trading activity increased. Some stocks, particularly securities stocks, witnessed impressive reversals, suggesting a shift in the mindset of fund holders.

Market trading is always a probe into the thinking of each side, and volume, range, and price fluctuations are part of that outcome. Guessing can be right or wrong, but over many sessions, consistent signals increase the likelihood of accuracy. Therefore, market tops and bottoms often involve failed fluctuations and rarely conclude within 1-2 sessions.

Some stocks have corrected to levels where buying is feasible. However, as the market remains unstable, a gradual buying strategy is advisable. Stockholders are at a disadvantage, so patience will pay off. Buying on dips is easy, as it merely involves covering previously sold stocks, ensuring everyone gets a piece of the pie without competition.

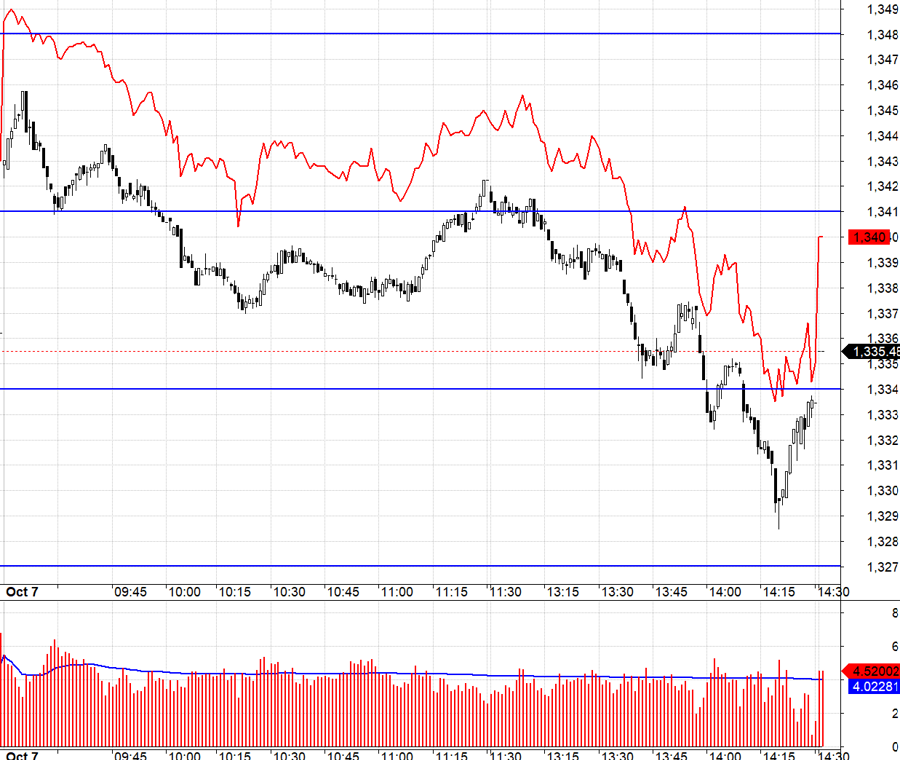

Today’s derivatives market continued to reflect expectations of the underlying market, with the F1 basis remaining positive throughout the day. This situation, coupled with low volume, could easily become a target for short sellers. However, to increase volatility, the index needs to be pushed down. In the morning, the VN30 dip below 1341.xx favored shorts, but it was not very profitable as the index hovered around the same level, and those who didn’t exit quickly even incurred losses. The afternoon session was better; the second dip below 1341.xx saw more aggressive selling, and although the basis didn’t contract, it limited short sellers’ profits. The VN30 index opened up two ranges, from 1341.xx to 1334.xx and then to 1327.xx. However, it is crucial to maintain discipline and close half the position at the 1334.xx threshold to secure profits, with the remaining half aiming for additional gains or breaking even.

Today’s significant drop in volume indicates a decrease in loose stocks. The market is likely to experience a few narrow-range sessions with low volume or sessions with forced openings to test supply. The strategy remains to buy stocks, and long/short derivatives positions should be managed flexibly.

The VN30 closed today at 1335.48. Tomorrow’s resistances are 1341, 1348, 1356, and 1365. Supports are 1333, 1325, 1318, and 1308.

“Blog chứng khoán” reflects the personal views of the author and does not represent the opinions of VnEconomy. The assessments and investment views expressed are solely those of the author, and VnEconomy respects the author’s perspective and writing style. VnEconomy and the author are not responsible for any issues arising from the published assessments and investment views.

{kind=link}