|

Source: VietstockFinance

|

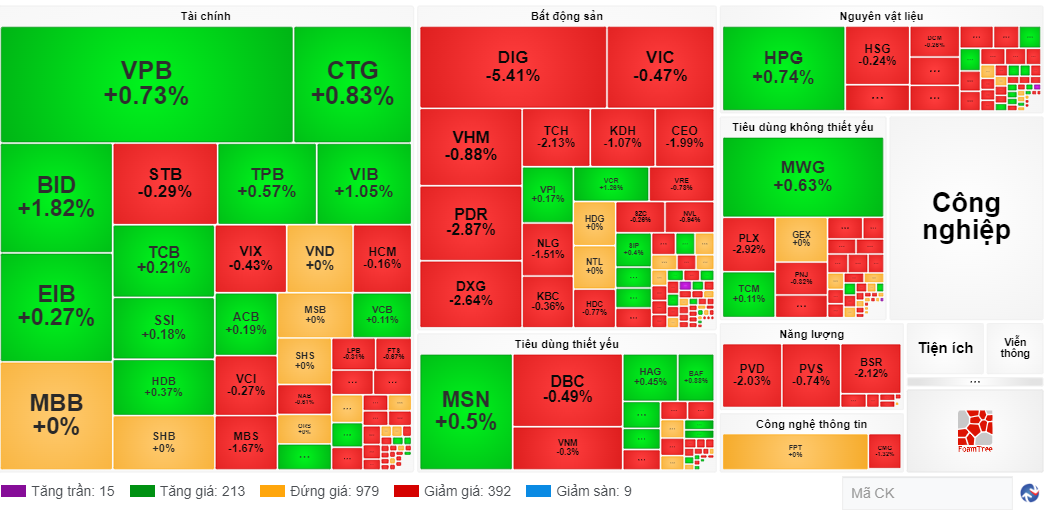

Bears dominated today’s session, with over 500 tickers closing lower compared to nearly 240 gainers. Most sectors ended in negative territory, except for consumer services, hardware, and banking, which managed to stay afloat.

BID, CTG, VPB, HDB, VIB, MSB, and OCB managed to stay in the green, providing some support to the banking sector. However, TCB, MBB, ACB, LPB, and STB faced selling pressure, weighing on the industry.

On the downside, telecom and energy stocks witnessed steep declines, with BSR leading the energy sector lower. Oil and gas-related names such as PVS, PVD, and PVC also fell, shedding over 2% each.

In the telecom space, VGI, FOX, and CTR all traded lower, with VGI plunging more than 4%.

Today’s trading value exceeded 18.5 trillion VND. Buying interest picked up on the HNX and UPCoM exchanges, while turnover on the HOSE remained on par with the previous session.

AM Session: Sellers Take Control, Banks Provide Support

Market sentiment remained hesitant around the 1,300 level. The VN-Index lacked a clear direction and dipped into negative territory in the final minutes of the morning session on October 15. At the midday break, the VN-Index edged down 0.01 points to 1,286.33, while the HNX-Index lost over 1 point to close at 229.69.

Banking stocks continued to serve as the primary pillar of support for the market. BID, CTG, VPB, VIB, VCB, and OCB contributed a combined 2.3 points to the VN-Index‘s performance. However, financial stocks exhibited signs of divergence, with many names closing lower or flat.

Source: VietstockFinance

|

By the end of the morning session, decliners outnumbered advancers by a significant margin, with over 400 tickers in the red compared to nearly 220 gainers. Selling pressure was concentrated in the real estate, energy, and materials sectors.

On a positive note, market liquidity picked up, with trading value surpassing 9 trillion VND across the three listed exchanges.

10:40 AM: Banks Hold the Fort

Buying and selling forces were more evenly matched in the market, and by 10:30 AM, the number of gainers and losers was relatively balanced, with 278 tickers in the green and 279 in the red.

The VN-Index maintained its upward trajectory, rising nearly 4 points, thanks to the resilience of the financial and banking sectors. CTG, BID, EIB, TPB, and VIB posted solid gains. Notably, BID contributed 1.7 points to the index’s advance, accompanied by CTG, VCB, VIB, ACB, and TCB. The banking sector played a pivotal role in propelling the VN-Index higher during the morning session.

Real estate stocks reversed course and slipped into negative territory, with DIG plunging over 5%. Several other names in the sector, including PDR, DXG, and KDH, also faced selling pressure. However, the situation wasn’t entirely bleak, as VPI, HDG, SZC, SIP, and VPH managed to eke out modest gains.

The energy and telecom sectors were the worst performers, with the former declining nearly 2% and the latter falling over 1%.

Healthcare stocks took the lead, driven by AMV, which hit the upper circuit breaker, and BBT, which climbed more than 13%.

HPG, a steelmaker, inched up nearly 1%. During the third quarter of 2024, the Hoa Phat Group (HOSE: HPG) reported a 51% year-over-year increase in after-tax profit, reaching 3,022 billion VND.

Market Open: Buyers Take the Upper Hand

Vietnam’s stock market kicked off the session on October 15 with a mild positive bias. By 9:20 AM, the VN-Index had climbed nearly 3 points. The initial trading hours followed a familiar pattern, with sellers slightly ahead.

Essential consumer goods stocks set a positive tone early on, with companies in the livestock industry, such as DBC (+1.3%) and BAF (+2.2%), leading the way. Several other names in the sector, including VNM, MSN, CTP, and KDC, also edged higher.

Financial and real estate stocks moved higher in unison, although the magnitude of their gains was not entirely convincing.

In the real estate sector, VHM slipped 0.3%, exerting some pressure on the market. Conversely, several real estate tickers, including VPH, CIG, and OGC, soared to their daily limit-up levels.

On the flip side, energy and information technology stocks tilted lower. BSR and PVC in the energy sector, along with FPT in the IT space, retreated marginally.

{kind=link}