Market liquidity increased compared to the previous trading session, with the VN-Index matching volume reaching over 505 million shares, equivalent to a value of more than 11.9 trillion dong; HNX-Index reached over 48.1 million shares, equivalent to a value of more than 865 billion dong.

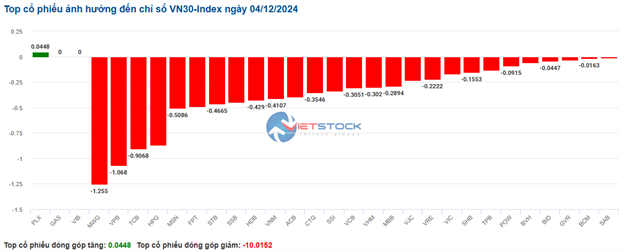

VN-Index opened the afternoon session with a continued lackluster performance as selling pressure increased, causing the index to plunge and close in the red. In terms of impact, BID, VHM, CTG, and MWG were the most negative stocks, taking away more than 3.3 points from the index. On the other hand, VCB, SAB, VTP, and PLX were the most positive stocks, contributing more than 1.4 points to the overall index.

| Top 10 stocks impacting the VN-Index on 04/12/2024 (in points) |

Similarly, the HNX-Index also witnessed a lackluster performance, with negative impacts from stocks such as IDC (-1.82%), DHT (-3.23%), MBS (-1.79%), and SHS (-1.53%)…

|

Source: VietstockFinance

|

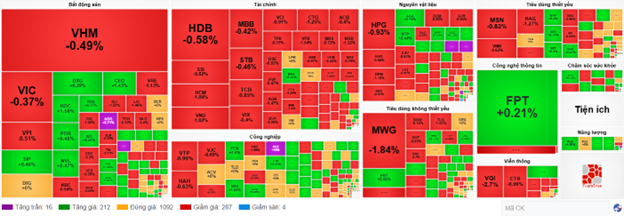

The information technology sector witnessed a sharp decline of 1.13%, mainly due to losses in FPT (-1.03%), CMG (-3.09%), ITD (-1.53%), and CMT (-0.72%). This was followed by the real estate and telecommunications sectors, which decreased by 1% and 0.93%, respectively. On the other hand, the energy sector witnessed the strongest recovery in the market, gaining 0.46% with green signals from BSR (+1.04%), PSB (+1.85%), HLC (+1.67%), THT (+0.81%), and MGC (+3.64%). The utilities sector also witnessed a recovery, increasing by 0.17%.

In terms of foreign trading, foreign investors continued to net sell over 682 billion dong on the HOSE exchange, focusing on stocks such as MWG (250.38 billion), FPT (134.51 billion), VRE (82.24 billion), and VNM (71.14 billion). On the HNX exchange, foreign investors net sold more than 27 billion dong, focusing on IDC (26.12 billion), SHS (5.78 billion), PSW (1.69 billion), and NTP (1.2 billion).

| Foreign Trading Buy-Sell Dynamics |

Morning Session: Large-cap stocks and foreign trading continue to weigh on the market

The pressure from large-cap stocks and foreign trading caused the VN-Index to remain in negative territory throughout the morning session, despite a significant recovery effort after adjusting near the 1,240-point level. At the midday break, the VN-Index lost 2.3 points, settling at 1,247.53 points. Meanwhile, the HNX-Index fluctuated slightly above the reference level, reaching 225.57 points, up 0.12%. The market breadth remained tilted towards decliners, with 320 decreasing stocks and 245 advancing stocks.

CTG, BID, HPG, MWG, and VPB were the leading stocks with a similar impact on the index, collectively causing the VN-Index to drop by approximately 2 points. Conversely, VCB, SAB, and GAS contributed the most in narrowing the decline towards the end of the morning session, recovering nearly 1.5 points for the VN-Index.

No sector stood out during the morning session, as most sectors exhibited mixed performances with narrow ranges. The telecommunications group witnessed the sharpest decline, pressured by stocks such as VGI (-0.76%), FOX (-2.03%), CTR (-0.64%), and SGT (-0.67%). However, VNZ (+1.91%) and YEG (+4.18%) managed to buck the trend and record impressive gains.

Similarly, the real estate sector also witnessed several bright spots, with AGG and L14 reaching the ceiling price, while NTC (+3.23%), HDC (+2.57%), HDG (+1.75%), CEO (+1.43%), and SIP (+1.43%) also posted notable gains. However, the adjustment pressure from large-cap stocks such as VHM, VRE, VIC, BCM, IDC, KDH, and NLG prevented the sector index from turning positive. The financial sector also exerted considerable pressure on the VN-Index, as red signals were observed across banking, securities, and insurance stocks, although the declines were not significant for most stocks. A few notable exceptions included BVH, VPB, VBB, VND, and VCI, which fell by over 1%.

The energy, utilities, and information technology sectors managed to stay in positive territory at the end of the morning session. However, the notable gains were primarily driven by small-cap stocks such as APP (+4.65%), AAH (+2.86%), PSB (+1.85%), MGC (+1.82%); TTA (+3.21%), KHP (+2.71%), and TDM (+1%). The remaining stocks exhibited only minor fluctuations below 1%.

Foreign investors continued to net sell nearly 422 billion dong on the HOSE exchange, focusing their selling pressure on MWG (111.93 billion), VRE (59.59 billion), and FPT (52.70 billion). On the HNX exchange, foreign investors also net sold nearly 29 billion dong, mainly offloading IDC (17.9 billion).

10:30 am: Selling pressure intensifies in the financial sector, pushing the VN-Index towards the 1,240-point level

The main indices exhibited mixed performances and fluctuated around the reference levels, reflecting investors’ cautious sentiment. As of 10:30 am, the VN-Index decreased by 7.12 points, hovering around 1,242 points. Meanwhile, the HNX-Index gained 0.25 points, trading around 225 points.

The breadth among the VN30 basket remained tilted towards decliners, with 25 decreasing stocks and only 5 advancing stocks. Notably, MWG, VPB, TCB, and HPG negatively impacted the VN30-Index, deducting 1.25 points, 1.06 points, 0.9 points, and 0.86 points from the index, respectively. Conversely, PLX was the sole stock contributing positively to the index, although its impact was not significant.

Source: VietstockFinance

|

Selling pressure persisted in the telecommunications sector during the morning session, causing it to record the sharpest decline of 1.8% among all sectors. Large-cap stocks such as CTR (-0.48%), VGI (-2.27%), TTN (-2.16%), and ELC (-0.75%) led the decline.

Additionally, the financial sector faced significant headwinds, with most stocks trading in negative territory. Specifically, HDB decreased by 0.58%, SSI fell by 0.62%, VND lost 1.82%, and HCM declined by 0.73%… Conversely, a few stocks managed to recover slightly, including LPB (+0.15%), FTS (+0.12%), and NAB (+0.31%).

The real estate sector exhibited mixed performances, with selling pressure slightly outweighing buying interest. Specifically, stocks such as VRE (-0.28%), KBC (-0.36%), VIC (-0.35%), and VHM (-0.24%) faced selling pressure. On the other hand, buying interest remained robust in certain stocks, including SIP (+0.6%), DIG (+0.49%), DXG (+0.29%), and CEO (+2.14%)…

Compared to the opening, the number of declining stocks increased, with 287 stocks trading lower and 212 stocks trading higher.

Source: VietstockFinance

|

Market Open: Cautious Sentiment at the Start of the Session

At the opening of the trading session on December 4, as of 9:30 am, the VN-Index slightly decreased and fluctuated around the reference level, hovering near the 1,247-point mark. Meanwhile, the HNX-Index recorded a slight increase, maintaining the 225.6-point level.

The S&P 500 index edged slightly higher on Tuesday (December 3), setting a new record. Specifically, the S&P 500 index gained 0.05% to close at 6,049.88 points. The Nasdaq Composite Index rose 0.40% to 19,480.91 points, reaching a new intra-day record high as Apple shares surged to a new 52-week high. Both the S&P 500 and Nasdaq Composite indices achieved new record closing highs. In contrast, the Dow Jones index lost 76.47 points (equivalent to 0.17%) to settle at 44,705.53 points.

The VN30 basket witnessed a slightly negative performance, with 22 decreasing stocks, 5 increasing stocks, and 3 stocks trading flat. Notably, SSB, MWG, and CTG were the top losers, while GVR, PLX, and GAS were the top gainers.

As of 9:30 am, the telecommunications services sector was the group with the most negative impact on the market. Specifically, stocks such as VGI (-2.27%), CTR (-0.8%), FOX (-0.2%), and ELC (-1.12%) declined.

: Binance and OKX Issue Urgent Alerts")

{kind=link}