|

Dollar-Dong Exchange Rate Soars: Regulator Steps In. Image: TL

|

The heat on exchange rates continues

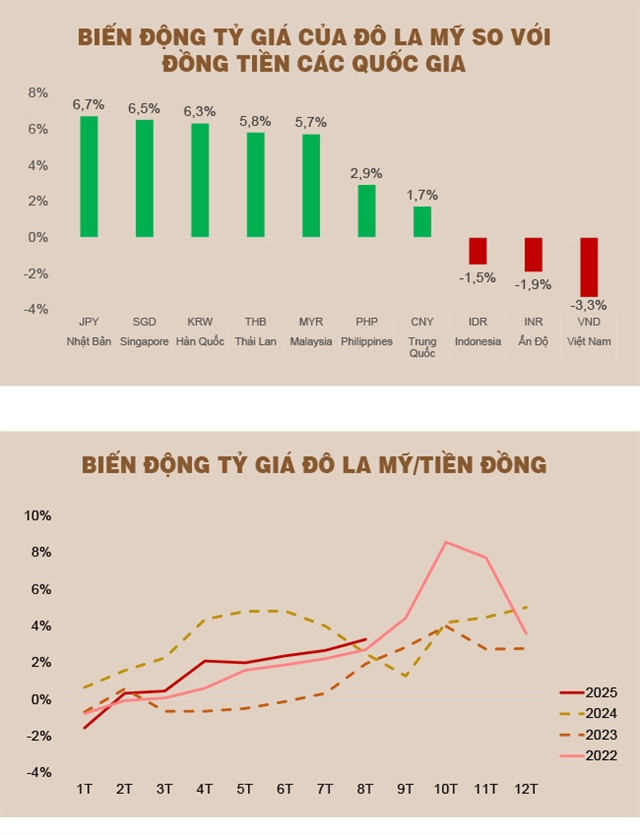

As of August 22, 2025, the US dollar-to-VND exchange rate in the interbank market had reached 26,350 VND per dollar, a roughly 3.3% increase compared to the beginning of 2025. Notably, the Vietnamese dong’s depreciation occurred amid a nearly 10% decline in the international US dollar index, and the dong also weakened against many regional currencies. This indicates that exchange rate pressures stem not only from external factors but also reflect the economy’s internal weaknesses.

According to analysts, the current exchange rate tension results from both objective and subjective causes, influenced by domestic and international factors. Externally, the two most significant impacts stem from the US’s new tariff policy and the Federal Reserve’s monetary policy shift. The US’s tariff changes have slowed down foreign direct investment (FDI) disbursements in Vietnam, while the trade surplus tends to narrow, reducing foreign reserve supplementation. Simultaneously, the Fed’s high-interest rates on the US dollar make it more attractive than the dong.

|

Domestically, keeping interest rates low and expanding credit to support economic growth have diminished the dong’s appeal. Vietnam’s foreign reserves currently stand at around $80 billion, lower than in previous periods, while supplementary foreign currency sources from trade and investment are slower. This limitation makes exchange rates more volatile, especially during periods of high foreign currency demand for commercial activities.

Commitments from the regulator

Facing escalating exchange rate pressure, the State Bank of Vietnam (SBV) has announced direct intervention by selling 180-day foreign currency with cancellation rights on August 25 and 26, 2025, to credit institutions with a negative foreign currency status. The selling rate was set at 26,550 VND per dollar, close to the ceiling (+5%) compared to the central exchange rate of 25,298 VND per dollar on August 23, 2025.

This familiar measure was previously employed by the SBV in 2022 when foreign capital outflows net withdrew 22.7 billion USD. The 180-day sale mechanism allows the regulator to send a strong signal that exchange rates will be controlled within a certain range without immediately tapping into foreign reserves. This approach curbs speculative sentiment and is seen as a “buying time” solution, awaiting more favorable conditions in the future.

|

This foreign currency sale decision follows a series of interest rate regulatory moves in the interbank market, where interest rates are maintained at around 4% despite ample liquidity. The aim is to narrow the interest rate gap between the dong and the US dollar to discourage capital shifts towards holding US dollars. Combining interest rate management with foreign currency sales indicates that the regulator is employing multiple tools simultaneously to curb exchange rate hikes. |

Essentially, the SBV aims to affirm its determination to keep the US dollar-to-dong exchange rate fluctuations within a 4% target for 2025. By implementing this solution, banks with a negative foreign currency status can purchase from the SBV to balance their needs and benefit if the exchange rate rises beyond the SBV’s selling rate (26,550 VND per dollar). Conversely, they also have the right to cancel if market conditions change, causing the exchange rate to drop significantly (with the right to cancel 2-3 times depending on the purchase value of over or under $10 million). This flexibility significantly reduces dollar speculation, thereby easing pressure on the exchange rate. However, if foreign currency demand in the coming period surpasses the current scale (based on the negative foreign currency status of credit institutions), dollar-buying demand may increase, prompting the SBV to open new sale rounds or even intervene directly, as occurred in 2022.

This foreign currency sale decision also follows interest rate regulatory moves in the interbank market, with rates maintained at around 4% despite ample liquidity. The goal is to narrow the interest rate gap between the dong and the US dollar to curb capital shifts towards holding US dollars. The combination of interest rate management and foreign currency sales indicates a comprehensive approach to curbing exchange rate hikes.

Expectations for improved external conditions

Exchange rate developments in the coming months will heavily depend on expectations of the Fed’s monetary policy easing. The market currently leans towards the possibility of a Fed interest rate cut in September 2025 and another in December 2025. Should this scenario unfold, the interest rate gap between the dong and the US dollar would narrow somewhat, thereby reducing pressure on the exchange rate. However, the impact’s extent depends on the cut’s magnitude; a mere 0.25 percentage point reduction may not be enough to alter the situation, and pressure on the dong could persist if the trade balance and investment flows remain unfavorable.

In reality, with exchange rates facing dual pressure from domestic and international factors, a slight Fed interest rate reduction is unlikely to reverse the trend. For the dong to stabilize, more favorable conditions are needed, including improvements in the trade surplus, enhanced foreign investment attraction (direct and indirect), and reasonable domestic interest rate policies to encourage capital inflows while deterring outflows.

Given the current assumptions, the most plausible scenario is for the exchange rate to remain high in the final months of the year but within the regulated range of approximately 4%, fluctuating with the Fed’s interest rate reduction trajectory and the balance of foreign currency flows from trade and investment activities. Should the Fed delay interest rate cuts or unexpected shocks cause sharp foreign currency outflows, the SBV would likely intervene directly by selling foreign currency, absorbing money through bills, or even considering raising interest rates or accepting further dong depreciation.

Trịnh Duy Viết

– 07:00 30/08/2025

“The Vietnamese Dong Strengthens: State Bank’s USD Sale Intervention Sees Rates Drop Below 26,500”

The central bank has intervened in the forex market by offering USD sales with a maturity period of 180 days at a rate of VND 26,550 per USD. This move is part of a broader strategy to stabilize the foreign exchange market and ensure liquidity.

The Central Bank’s U-turn: A Modest Net Inflow in the Open Market

The State Bank of Vietnam (SBV) shifted its focus to a mild net withdrawal from the open market during the week of August 11-18, marking a change in direction after a month of consecutive net injections.

“Viet Nam Dong Surges: Bank Rates Surge Past 26,500, Freefalling USD Hits New Lows”

This morning, the US dollar rate surged past 26,500 VND at several banks. Meanwhile, the dollar rate in the free market hit a record high of 26,600 VND on the selling side.

The Price of Gold Drops: A Missed Opportunity for Many

The gold trading price this morning of August 12th took an unexpected turn as the 99.99 gold ring witnessed a sharper decline compared to the SJC gold bar, following the downward trend of global gold prices.

The Overnight Interbank Interest Rate Surges Past 6%, The State Bank Continues to Inject Liquidity

The sharp rise in interbank VND interest rates narrowed the gap with USD interest rates, easing pressure on exchange rates. However, this also resulted in increased capital costs for banks.

{kind=link}