Vietnamese Stock Market Surges Past Predictions

Vietnam’s stock market on August 28 once again proved that its movements are often unpredictable. Contrary to the expectations of many experts of a downward correction after a hot streak, the VN-Index remained in the green and closed at 1,680 points, an increase of 8 points from the previous session.

The VN30 performed even better, surpassing the 1,860-point mark, while the HNX-Index also edged up to 276 points. Liquidity cooled down compared to the previous explosive sessions, but the HOSE floor still recorded a trading value of more than VND 34,400 billion.

Notably, foreign investors continued their net selling streak, offloading more than VND 6,500 billion in just two days. However, despite this pressure, the market rose for the third consecutive session, pushing the VN-Index back to its historical peak.

This situation has left many individual investors in a dilemma. Tuan Minh, an investor in Ho Chi Minh City, shared that he sold all his bank and securities stocks last weekend because he believed the market was about to correct downward by 10-15% as predicted. However, just a few days later, bank stocks such as SHB, HDB, VPB, MBB, and LPB rebounded to their peaks, leaving early profit-takers with regrets.

The stock market has been vibrant in recent sessions

Which Sectors to Invest in for the Year-End?

According to Truong Hien Phuong, Senior Director of KIS Vietnam Securities Company, the stock market often presents surprises. Since April, the VN-Index has surged by nearly 400 points. A corrective phase is inevitable to balance prices, but it seems that the recent correction has quickly come to an end. Mr. Phuong believes that the market is on the cusp of a new growth cycle, presenting opportunities for both existing investors and those holding cash.

So, which sectors should investors focus on during this period? Mr. Phuong identified four main pillars: securities, banking, residential real estate, and public investment. Among these, the banking sector is highly regarded due to the recent relaxed policies from the State Bank of Vietnam.

The reduction in the compulsory reserve ratio not only reduces capital costs and boosts credit flow but also opens up more significant profit opportunities for banks. Notably, banks that take over weak institutions can directly benefit by utilizing tens of thousands of billion VND from the reserve source for lending, optimizing their business efficiency.

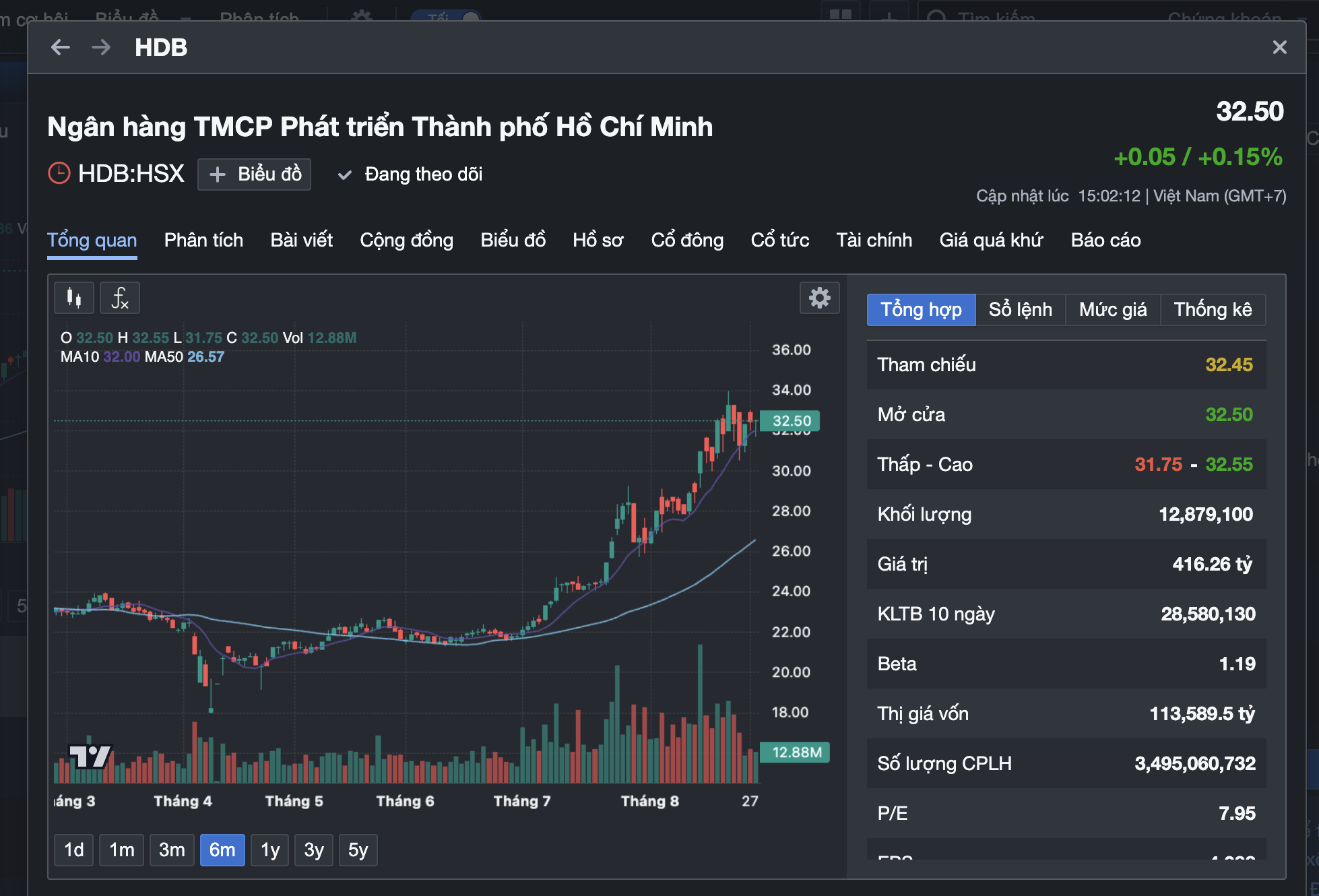

It is evident that bank stocks are currently in the spotlight. For instance, HDBank (HDB) has surged by nearly 50% in just under two months. This performance reflects not only robust demand but also the industry’s solid fundamentals, with banking profits witnessing impressive growth.

Since the end of last year, the State Bank of Vietnam has completed the transfer of four weak banks to large institutions such as Vietcombank, MB, HDBank, and VPBank. This move strengthens the system and provides additional development space for the acquiring banks.

Many bank stocks, such as HDB of HDBank, have surged in the past period

Recent reports also reinforce this positive outlook. According to Maybank Securities, the listed banks’ profit in Q2/2025 exceeded expectations, rising 16% year-on-year, bringing the six-month growth to 13%. For the full year 2025, the banking sector is expected to achieve a profit growth rate of about 15%, with Q3 projected to be the strongest quarter.

Many securities companies still believe that bank stocks have significant upside potential, especially with credit growth expected to reach 16% for the year, and profits for many banks surpassing 20%.

The question arises as to whether this upward trend can be sustained, especially with foreign investors maintaining their net selling position. Can the banking sector continue to lead the market, or will capital gradually shift to other areas such as residential real estate or public investment? And, more importantly, if this indeed marks the beginning of a new growth cycle, what is the optimal timing for investment?

Stock Market Update for Week of August 25-29, 2025: Foreign Investors Apply Pressure at Peak Levels

The VN-Index concluded its fourth consecutive week of gains despite facing substantial pressure at the peak. However, the recent strong selling trend among foreign investors is a notable concern. August 2025 witnessed the largest foreign net-selling since the beginning of the year, which could hinder the market’s upward trajectory in the short term if the situation doesn’t improve promptly.

“Technical Analysis for the Session Ahead: On the Cusp of History”

The VN-Index has been on a remarkable growth trajectory, inching closer to its historical peak. With a high probability of breaching the old peak zone of 1,680-1,693 points, the index is poised for a potential breakthrough. Meanwhile, the HNX-Index has also been on an upward trend, forming a Big White Candle pattern, indicating strong buying pressure and potential for further gains.

Market Beat: Lackluster Liquidity Ahead of Holidays, VN-Index Stuck in a Tug-of-War

The trading session concluded with a modest gain in the VN-Index, which rose by 1.35 points (+0.08%), closing at 1,682.21. The HNX-Index also witnessed a positive movement, climbing 3.35 points (+1.21%) to finish at 279.98. The market breadth tilted towards the bulls, as evidenced by 436 advancing stocks against 315 declining ones. However, the large-cap sector told a different story, with the VN30 basket showing a slight dominance of red, as 15 stocks fell, 13 advanced, and 2 remained unchanged.

Technical Analysis for August 28: Shaking Up the Old Highs

The VN-Index experienced significant volatility as it retested the old peak zone of 1,680-1,693 points, while the HNX-Index oscillated around the reference level. Both indices witnessed relatively low trading volumes, indicating a cautious market sentiment.

“Foreign Investors Sell Nearly VND 2.7 Trillion as VN-Index Surges Past 1,680 Points: Which Stocks Were in the Firing Line?”

“Foreign investors showed strong buying interest in GMD stock during the afternoon trading session, making it the most actively bought stock across the market. The net buying value stood at an impressive 135 billion VND.”

{kind=link}