Sir, based on the PRVIATE 100 list – honoring the top private enterprises with the largest budget contributions in Vietnam, recently published by CafeF, the top 100 private enterprises paid 244,400 billion VND in taxes in 2024. From the perspective of Vietnam’s leading tax consulting organization, how do you evaluate the role of private enterprises in contributing to the state budget, and what does this mean for the country’s economic development?

In 2024, the private sector made significant progress, evident from the figure of 244,400 billion VND in tax contributions by the Top 100 Enterprises, equivalent to approximately 12-12.5% of the country’s total state budget revenue for the year. This substantial proportion affirms that, more than ever, the private sector has become a pivotal pillar alongside state-owned enterprises and the FDI sector.

This highlights two important points. Firstly, the financial strength and contributions of private enterprises have transcended the “startup” or “supplementary” phase to become a force on par with state-owned enterprises and FDI in the economic structure. Within the top 200 tax contributors in Vietnam, the private sector accounts for 95 representatives, the highest among the three sectors and approximately three times the number of FDI enterprises. The increasing presence of private enterprises in the state budget also signifies that the Vietnamese economy has entered a more mature stage, where resources are allocated across multiple pillars and in a more balanced manner.

Another crucial aspect is that the taxes paid by private enterprises are not limited to corporate income tax but also extend to various other taxes such as value-added tax (VAT), personal income tax, and land and land rental taxes, demonstrating the far-reaching impact of this sector on the entire economy.

The PRIVATE 100 list reveals a significant gap between the top performers (the Top 10 contributing 61% of the total) and the bottom half (contributing just over 10%), with 48 enterprises paying over 1,000 billion VND, an increase from 30 enterprises the previous year. What are your thoughts on this trend, and does it reflect a polarization within the private sector? Do you have any tax advice for the smaller enterprises on the list to enhance their contributions?

In my opinion, this polarization is a natural occurrence in the economic development process. The leading group, comprising large private conglomerates, accounts for more than 60% of the total tax contributions of PRIVATE 100. Meanwhile, the enterprises in the bottom half contribute just over 10%. However, it’s noteworthy that the number of companies with tax contributions exceeding 1,000 billion VND has increased significantly, from 30 to 48 in just one year. Additionally, among the top 200 tax contributors in Vietnam, approximately 95 are private enterprises, outnumbering the state-owned and FDI enterprises.

This is a very positive sign, as budget revenue will not solely depend on a few leading enterprises but will be shared more broadly. Furthermore, despite the polarization within the private sector, many enterprises in the lower half of the PRIVATE 100 list still outperform prominent members of the other two sectors in the Top 200 contributors.

To enable this group of enterprises to continue their growth and enhance their tax contributions, I believe that tax authorities and government agencies can implement more encouraging policies for private enterprises and facilitate their participation in domestic and global value chains, thereby accelerating their business development and, consequently, their contributions to the state budget.

Tax authorities could also provide incentives for higher compliance from taxpayers. For instance, for enterprises committed to high compliance and adopting standards such as the Tax Governance Framework, the frequency of inspections could be reduced. Additionally, enterprises themselves should focus on “getting it right from the start,” implementing mechanisms to ensure transparent and accurate compliance with tax regulations. An important consideration is to link tax obligations with ESG (environmental, social, and governance) strategies, as this not only reduces legal risks but also enhances their reputation in the capital market and internationally.

Within the PRIVATE 100, there are four conglomerates that contributed over 10,000 billion VND (Vingroup, THACO, TC Group, and Hoa Phat), accounting for nearly 45% of the total contributions. Can you analyze the tax structure that such diversified conglomerates typically face and how they optimize their budget contributions while maintaining business growth?

Diversified conglomerates always have to navigate a complex, multi-layered tax matrix. Corporate income tax (CIT) arises from various industries; value-added tax (VAT) is linked to imports, distribution, and retail; land tax is associated with real estate projects; and personal income tax (PIT) applies to their large workforce. The challenge lies in the asynchrony of these tax cycles: CIT is calculated quarterly and annually, VAT is monthly, PIT is both monthly and annual, and taxes related to land use rights and land rental tend to be lump-sum payments, often due at the beginning of a project. This creates pressure on cash flow and complicates financial management, risk management, and overall corporate governance.

To optimize their tax obligations, conglomerates typically establish a centralized tax management unit to ensure data consistency across the entire system. They also restructure their legal entities to take advantage of incentives in different sectors, stagger land-related tax obligations according to project progress, and integrate tax strategies with ESG (environmental, social, and governance) goals, transforming tax costs into a part of their commitment to sustainable development.

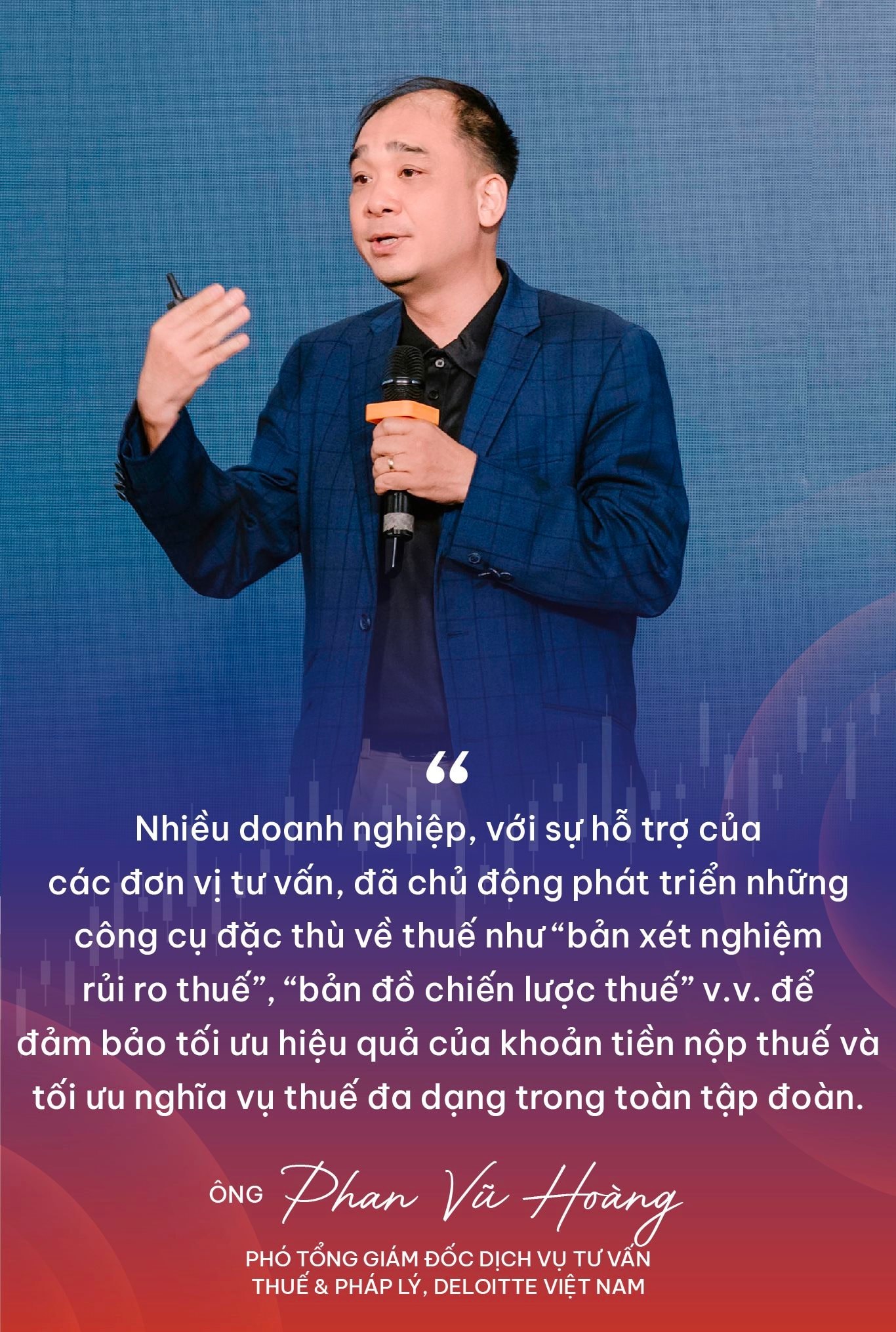

Most importantly, many enterprises, with the support of consulting firms, have proactively developed tax-specific tools such as “tax risk assessment frameworks” and “tax strategy roadmaps” to ensure the optimization of tax payments and tax obligations within the conglomerate, maintaining absolute compliance while maximizing cash flow efficiency.

Real estate and construction is the sector with the largest contribution, amounting to approximately 65,000 billion VND. From Deloitte’s tax consulting experience, what tax challenges do private real estate enterprises typically face, especially regarding land-related taxes and corporate income tax, and how can they enhance their contribution efficiency?

The real estate industry is among the sectors bearing the heaviest tax burden. Taxes related to land, land use rights, and land rentals often account for more than half of their financial obligations, and they are typically lump-sum payments, creating challenges for cash flow management. Regarding corporate income tax, revenue is usually recognized once upon project completion, while expenses are incurred over several years. This can lead to discrepancies and differing interpretations when determining taxable income. Additionally, VAT is another hotspot, as the refund procedures are complex, and the risk of additional tax assessments is high.

To enhance efficiency, enterprises need to proactively plan their tax obligations related to real estate according to the project’s progress, standardize their documentation, especially expense-related documents, and adopt technology for tax management. These solutions not only optimize tax costs but also minimize legal risks in an industry that is under constant scrutiny.

The private banking group has 16 representatives on the list, with a total contribution of nearly 46,300 billion VND, led by Techcombank and HDBank. What does their significant growth in budget contributions (e.g., HDBank’s 101% increase) signify? Does it reflect improved financial health?

The substantial increase in tax contributions by private banks indicates enhanced operational efficiency and financial health within the system, despite the numerous adverse factors in 2024. The surge in corporate income tax reflects actual profits and better cost control measures. Simultaneously, revenues from personal income tax and value-added tax have also increased, reflecting the expanding scale of personnel and digital services.

More importantly, this breakthrough confirms that private banks have become a pivotal pillar alongside the state-owned banking system. This contributes to the diversity and resilience of the nation’s financial sector.

However, it’s worth noting that as the scale of assets and product complexity grow, so do tax risks, especially regarding reasonable expenses (particularly those specific to the financial-banking industry), related-party transactions, provision for losses, and financial derivatives. Therefore, establishing a robust governance framework, including tax governance, aligned with international standards, is imperative.

Compared to other countries in the Southeast Asian region, how do you assess the Vietnamese tax system in terms of its effectiveness in encouraging investment and growth?

If we look at the basic parameters, Vietnam has made significant strides in developing its tax system in line with international best practices. The standard corporate income tax rate of 20% and the preferential rate of 15-17% for small and medium-sized enterprises are reasonable compared to the region. The value-added tax rate of 10% (which can be reduced to 8%) is appropriate for the country’s current development stage, while the sector-specific and location-based incentives have successfully attracted both domestic and foreign investments.

However, there are areas where the Vietnamese tax system can be further refined. Compliance costs for enterprises are relatively high, especially in VAT refund procedures and land-related tax obligations. Some regulations lack clarity, leading to inconsistencies and differing interpretations between taxpayers and tax authorities, such as the 0% VAT rate for services provided to export processing enterprises. The regulations are issued relatively quickly, but more time is needed to assess their practicality and alignment with business realities.

Additionally, the budget remains heavily dependent on VAT and taxes and fees related to the oil and gas and real estate sectors, which are susceptible to fluctuations in external markets and consumer demand, both of which are constantly evolving.

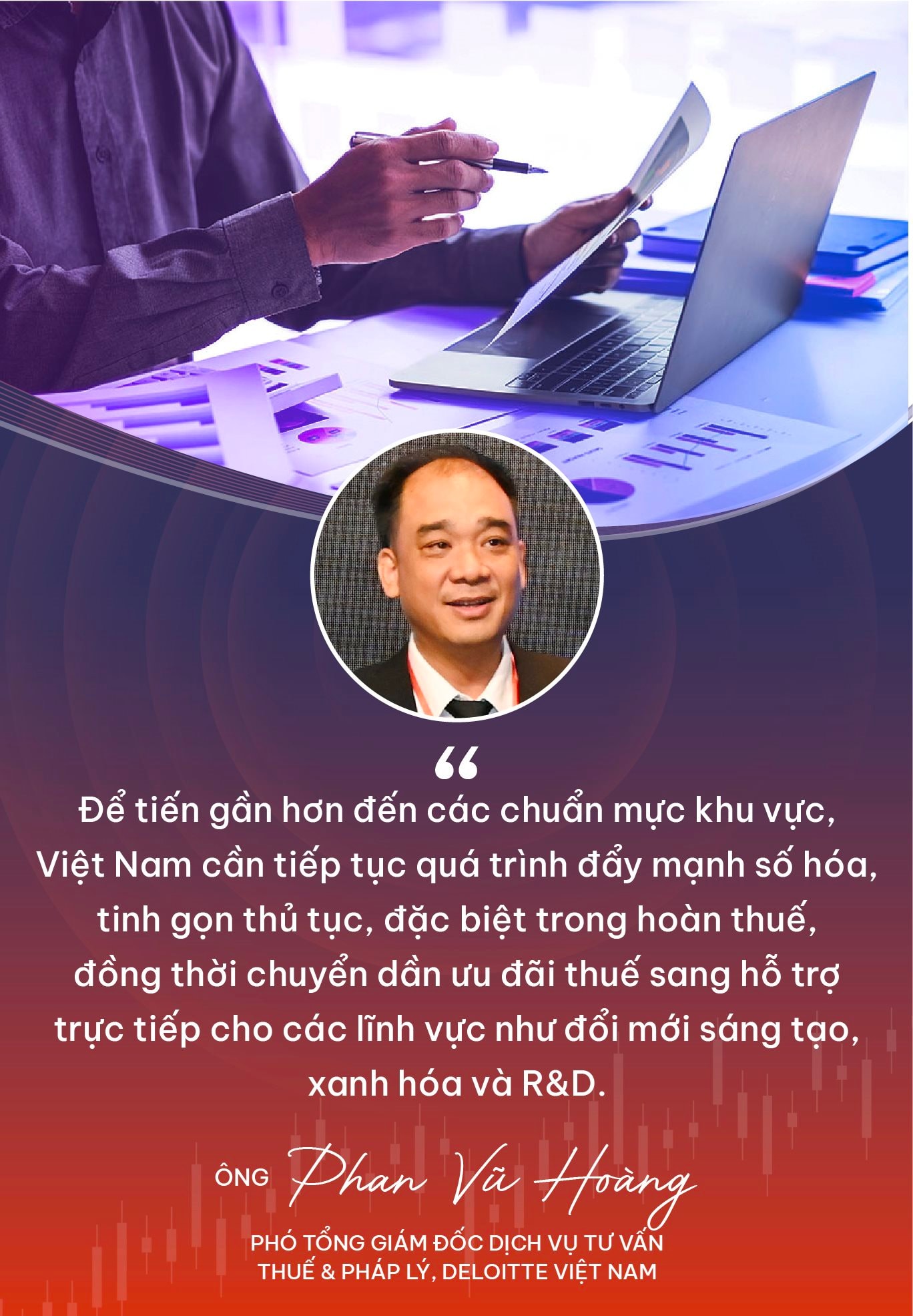

To align more closely with regional standards, Vietnam should continue to digitize and streamline procedures, especially for VAT refunds, and gradually shift from tax incentives to direct support for sectors such as innovation, greening, and R&D. What are your thoughts on the significant tax changes impacting the private enterprise sector?

2025 marks a pivotal year, with several new tax policies coming into effect and directly affecting enterprises across all three sectors.

In indirect taxes, the VAT Law extends the reduced VAT rate of 8% until the end of the year to support consumption. However, the new VAT Law (No. 48/2024) also tightens conditions for deductions and requires the digitalization of invoices, forcing enterprises to modify their tax management processes, if not their entire framework. Corporate income tax has also tightened regulations on deductible expenses (e.g., reducing the threshold for non-cash payments from 20 million VND to 5 million VND) and tax incentives, such as requiring industrial parks to be located in challenging areas to qualify for incentives.

Moreover, tax authorities are enhancing their data analysis capabilities and risk detection systems, making it easier to identify even minor tax errors.

In this context, tax risks for private enterprises and other sectors are increasing in both magnitude and complexity. Business operators will need to devote more attention and consideration to tax matters than before.

For private enterprises, it’s crucial to take a proactive approach to assessing tax risks (e.g., using a heatmap to evaluate the impact and likelihood of tax risks) and implementing a robust tax governance framework to manage risks, maintain transparency, and build trust with partners, investors, and regulatory bodies.

In conclusion, the PRIVATE 100 list for 2024 underscores the growing significance of private enterprises in Vietnam’s economy. With contributions exceeding 244,000 billion VND, accounting for approximately 12% of the country’s total state budget revenue, they are not just important economic players but also pivotal contributors to the state budget.

However, alongside this role come increasingly complex tax challenges. To maintain their position and promote sustainable development, enterprises need to transcend the “minimal compliance” mindset and embrace “proactive tax governance.” By utilizing appropriate tools, such as the Tax Governance Framework, which has proven successful in international practice, enterprises can ensure compliance while linking tax obligations to their sustainable development strategies.

In the next decade, with the current growth trajectory and supportive policies, if private enterprises in Vietnam seize the opportunities, they will not only top the tax contribution lists but also become the key driver of the country’s sustainable economic development. I look forward to witnessing this transformation! Thank you for your insights!

CafeF Lists 2025 marks the return of two prestigious honor rolls:

PRIVATE 100 – Top private enterprises with budget contributions of 100 billion VND or more

VNTAX 200 – Top enterprises with budget contributions of 200 billion VND or more in the fiscal year

These lists are compiled by CafeF based on publicly available data or verifiable figures, reflecting the actual budget contributions of enterprises, including taxes, fees, and other mandatory payments. The transparent and accurate aggregation of publicly available data not only acknowledges the financial contributions of these enterprises but also fosters a sense of social responsibility and affirms their standing in the economy.

Notable enterprises in the 2025 list, reflecting their contributions in the 2024 fiscal year, include Agribank, ACB, AIA, BIM Group, Coteccons, HDBank, LPBank, LOF, Masan Group, MoMo, OCB, PNJ, SHB, Tasco, DOJI Group, PC1 Corporation, Nam Long Group, Hoa Sen Group, TCBS, Techcombank, TPBank, Vingroup, VPBank, Vinamilk, VNG Group, VPS, and VIMID.

“The Benefits of Registering for a 17% Tax Rate: Why It’s a Smart Move for Your Business”

The Ministry of Finance has recently submitted to the Ministry of Justice a dossier for appraisal of the Personal Income Tax Law (amended). This latest draft features several significant changes, most notably the introduction of a mechanism to calculate taxes on income and apply a 17% tax rate for households and individuals with business revenues exceeding the prescribed threshold.

“NCB Visa Cards Shine Bright Across Hanoi for National Day Celebrations”

Introducing the NCB Visa card, a symbol of pride and patriotism, released just in time for the 80th anniversary of our nation’s independence. With its vibrant red and yellow colors, this special “Pride” edition card is a perfect tribute to our beloved country. Just like the vibrant hues of our national flag flying high across the streets, this card adds a special touch to your celebrations.

A Rewarding Announcement for Over a Million Educators Nationwide

“This information has been provided by the Minister of Education and Training, Nguyen Kim Son.”

Don’t Be Mechanical: Applying International Standards to Vietnam’s Green Finance

“Over the years, Nam A Bank has been a strong advocate for green finance, and Mr. Vo Hoang Hai, the bank’s Deputy General Director, shared three key lessons learned during this journey at the International Conference on September 5th, with the theme ‘Unlocking the International Green Capital Market’.”

“Vietnam Emerges as a Rising Economic Powerhouse”

“In recent years, Vietnam has been emerging as a new economic powerhouse, according to Ramla Khalidi, the United Nations Development Programme (UNDP) Resident Representative in the country.

{kind=link}