Rate Adjustment is Necessary

In its newly released September strategic report, SSI Securities (SSI Research) anticipates that the market could be supported by expectations of a Fed rate cut on September 17 and the potential for a market upgrade in early October.

However, the main index has seen impressive growth in the last two months, so the pressure could increase significantly. “In a more cautious scenario, a strong adjustment phase could occur during the September – early October period, with a potentially larger amplitude than the adjustment phases since the April low,” SSI Research forecasts.

Looking back, the VN-Index recorded a relatively positive growth rate in September, with 7 increases in the past 10 years. However, the past 4 years have shown a marked change: since the 4-day holiday policy was implemented in September (from 2021), the market has often moved sideways or declined sharply – specifically falling 6% and 11.6% in 2022 and 2023, and rising less than 1% in 2021 and 2024.

Several factors could trigger a market adjustment, including increasing exchange rate pressure (VND depreciated by an average of 3% in the period of September-October from 2022-2024). Additionally, the season for announcing Q3 business results is usually less vibrant, and profit-taking pressure after a strong recovery in August could also lead to an adjustment phase.

“Statistics show that the market often goes through adjustment phases of more than 7% in an uptrend, especially after a rapid increase of more than 20% within 3 months. Currently, the VN-Index has increased by 50% in the past 3 months and has not recorded a decrease of more than 4.5% since the April low,” the SSI report states.

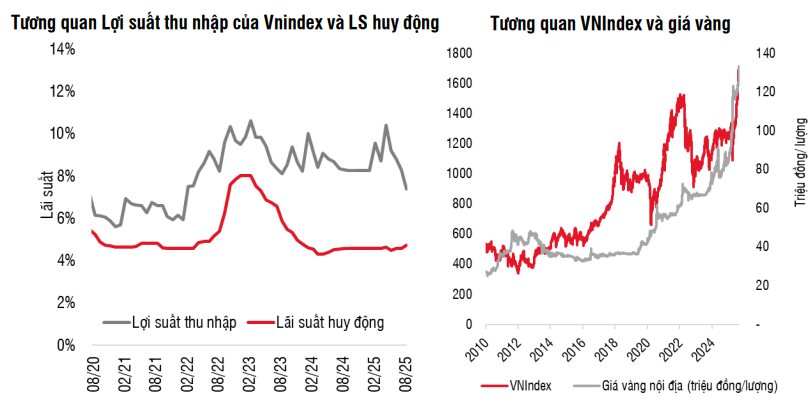

Currently, the Vietnamese stock market is offering an earnings yield of 7.7%, outperforming other major investment channels such as bank deposits (common interest rate of 5-6%), real estate (rental yield of 3-4%), and gold (after recent price increases).

Therefore, a strong adjustment phase in the coming time, if it occurs, could open up opportunities to accumulate stocks for a long-term investment horizon.

This outlook is reinforced by: (1) expectations of double-digit GDP growth in the next 5-10 years, driven by comprehensive institutional reforms and a focus on promoting the development of the private economic sector, (2) prospects for solid profit growth of over 14%/year in the period of 2025 – 2026, (3) market upgrade prospects that will attract more international capital, and (4) supportive monetary policies that maintain a favorable interest rate environment for the stock market.

Foreign Capital will Return Soon

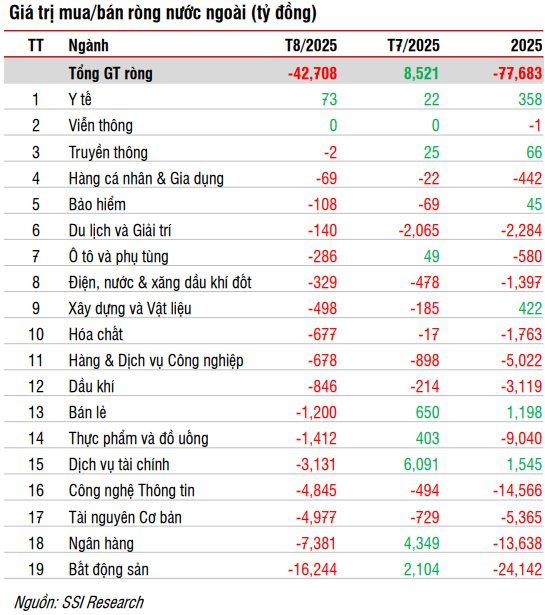

Regarding foreign transactions, foreign investors net sold strongly in August with a value of VND 42.7 trillion, contrary to the net buy value of VND 8.5 trillion in July, bringing the net sell value since the beginning of the year to VND 77.7 trillion.

In the context of global capital flowing back to the US and Chinese markets, along with the strong increase of VN-Index by +32.7% in the first 8 months of the year, foreign investors’ profit-taking is understandable. However, SSI assesses the mid to long-term outlook to remain positive.

In addition, the launch of new indices by HOSE, such as VN50 Growth, VNMITECH, and the renaming of Xtrackers FTSE Vietnam Swap UCITS ETF to Xtrackers Vietnam Swap UCITS ETF, along with a change in the base index from FTSE Vietnam to STOXX Vietnam Total Market Liquid, will also create certain short-term momentum. The analysis team expects the Vietnamese market to soon welcome the return of foreign capital in the coming period.

September Market: Where Should Investors Focus Their Attention?

The VN-Index is predicted to sustain its upward trajectory, aiming for the 1700 – 1800 point range, presenting an attractive investment prospect for September. With a focus on securities, port, and steel sectors, this presents a fresh opportunity for investors to capitalize on.

SSI Research: A Major Correction May Unfold by Late September

The latest insights from SSI suggest that a significant market correction in the near term could present a strategic opportunity for long-term investors to accumulate stocks at attractive valuations.

What Stock Code Was at the Center of Securities Companies’ Proprietary Trading “Sell-Off” on the Last Trading Day of the Week?

“Local brokerage firms turned net sellers on the Ho Chi Minh Stock Exchange (HoSE), offloading a total of VND224 billion ($9.5 million) worth of shares.”

The Stock Market’s Volatile Week: What’s Next?

Today (September 12th) marks the fourth consecutive session of stock market gains, propelled by Vingroup stocks, real estate, and steel sectors. While the market extended its positive momentum, trading liquidity weakened as foreign investors continued to offload holdings. Amid this upbeat performance, the market also received a boost from positive news on potential upgrades.

“Foreign Sell-Off Surges: A 3,000 Billion Dong Shockwave – Which Stock is the Main Target?”

“The HoSE witnessed a significant foreign sell-off, with net selling peaking at a whopping VND 2,937 billion.”

{kind=link}