Projects 2026 Profit Decline, Marking a 5-Year Low")

")

: Mixed Signals Emerge")

: Short-Term Outlook Continues to Deteriorate")

In a recent report, KBSV Securities highly rates Saigon Cargo Service Corporation (SCS) for its potential involvement in the Long Thanh Cargo Terminal Project.

According to the company, throughout the planning, design, and operational strategy development for the Long Thanh Cargo Terminal, Airports Corporation of Vietnam (ACV) has exclusively collaborated with SCS. Analysts commend SCS’s strong position to participate in the project, citing its extensive experience in cargo terminal operations with a 48% market share at Tan Son Nhat International Airport, robust financial health, ample cash reserves, and ACV’s significant stake in SCS.

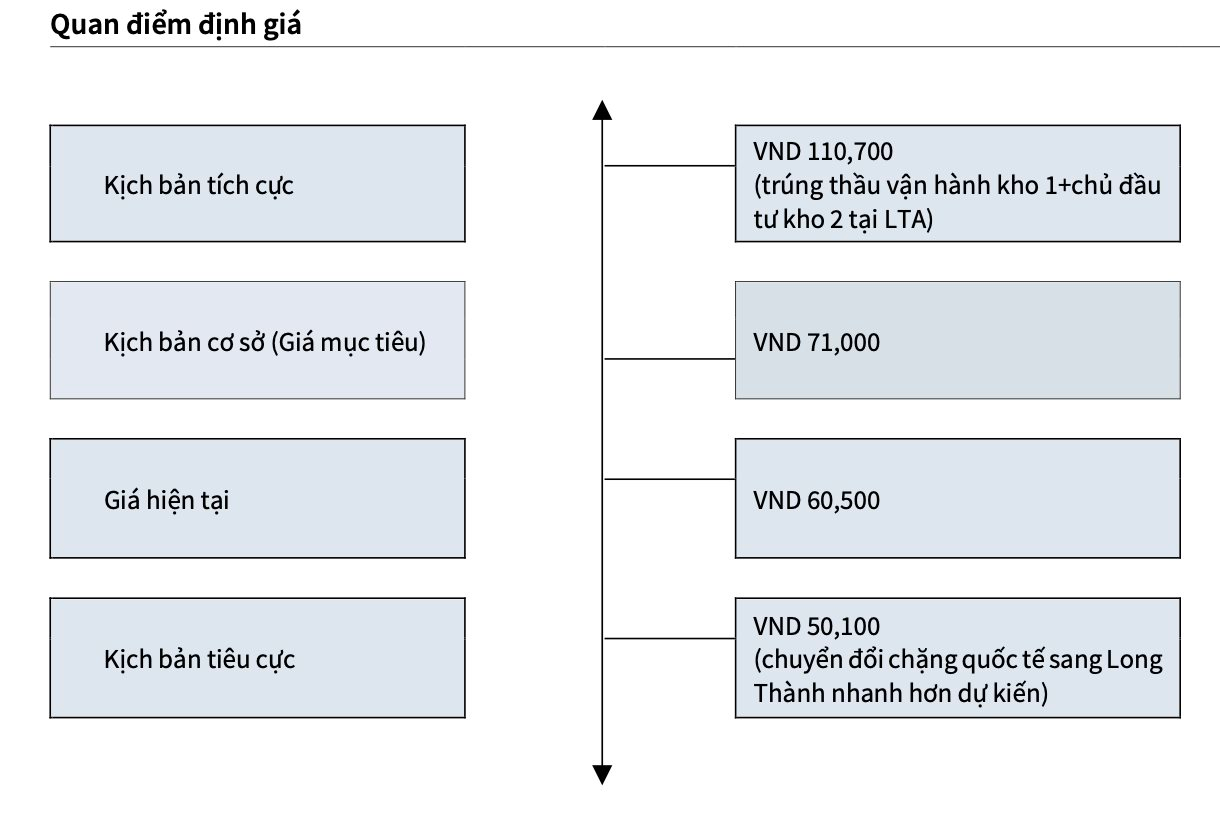

As there is no official announcement yet regarding the project investor or operator (expected by year-end), KBSV has not factored SCS’s potential Long Thanh contract into its base valuation. However, securing this project would bolster SCS’s long-term growth prospects and justify a higher market revaluation.

Previously, SCS identified preparing for the Long Thanh International Airport cargo terminal operations as a 2025 strategic priority. The company is actively strengthening its financial and human resources to partner with ACV.

This initiative is pivotal for SCS’s future. Once Long Thanh Airport becomes operational, most international cargo will shift there to alleviate pressure on Tan Son Nhat, directly impacting SCS’s current business.

At the 2025 Annual General Meeting, Mr. Nguyen Quoc Khanh, SCS CEO, revealed Phase 1 includes three warehouses: one fast-development warehouse (100,000 tons) and two general cargo warehouses (550,000 tons each). While ACV leads Component 3’s Warehouse 1, the operator remains undecided.

“In my view, SCS will likely operate Terminal 1, as training aviation logistics personnel is complex,” Mr. Khanh stated. He highlighted SCS’s integral role since the design phase, with ACV even modifying designs per SCS’s input.

Established in 2008, SCS is Vietnam’s second-largest air cargo terminal operator at Tan Son Nhat (48% market share). Key shareholders include Gemadept (33.4%) and ACV (13.6%). SCS is upgrading equipment to handle 350,000 tons/year.

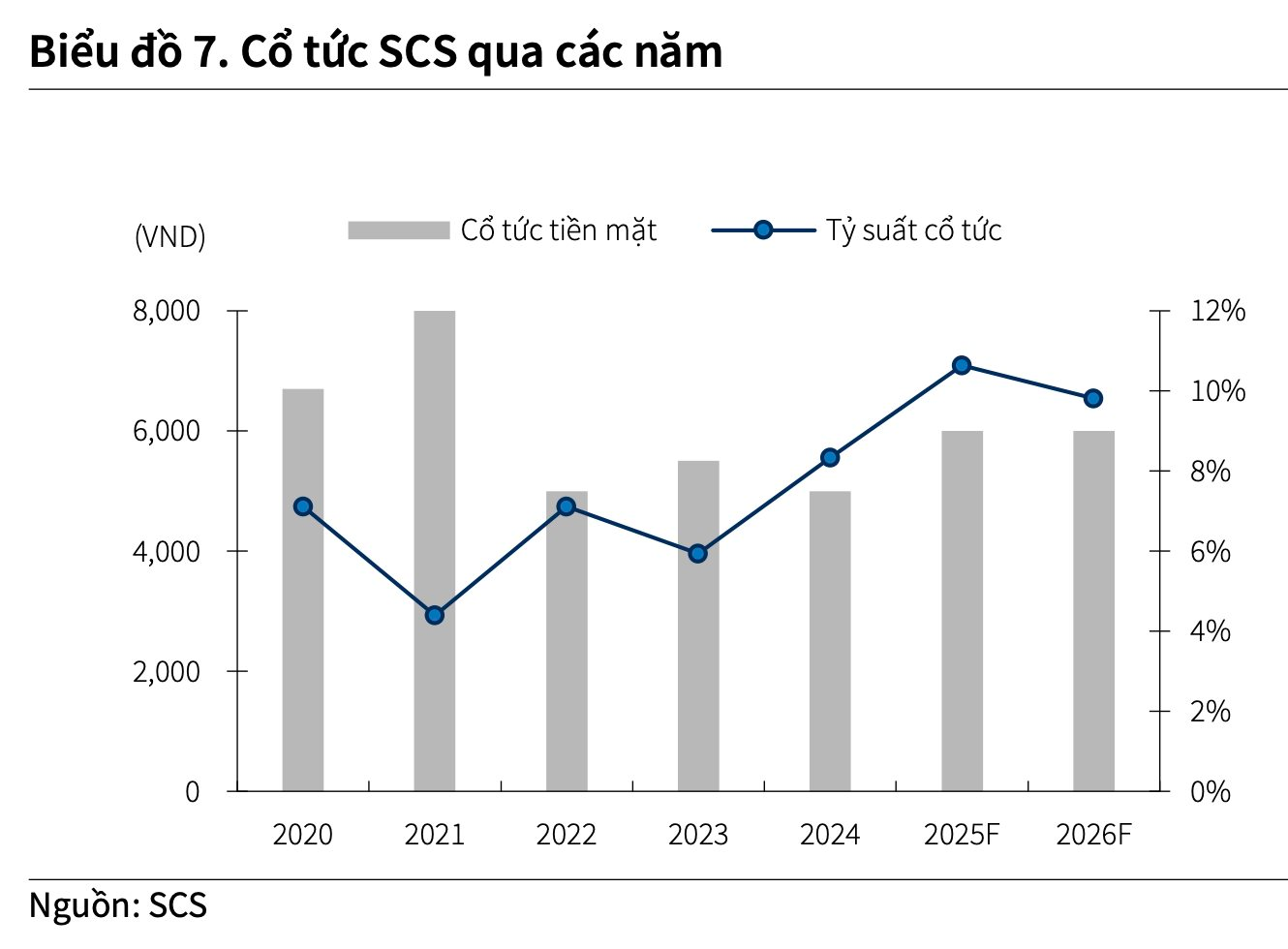

SCS maintains high cash dividends. The June AGM approved a 3,000 VND/share dividend for 2025.

With strong finances, zero debt, and conservative dividend guidance, KBSV expects SCS to sustain 6,000 VND/share dividends in 2025-2026.

Q2/2025 revenue rose 10% YoY to 292 billion VND, with matching gross profit growth. H1/2025 revenue hit 558 billion VND (+17%), net profit 359 billion VND (+7% YoY).

KBSV projects a 2% annual cargo volume decline to 2030 (optimistic scenario) with 5% service price increases, versus a 12% volume drop and 6% price erosion (pessimistic scenario), impacting margins.

{kind=link}