: Mixed Signals Emerge")

: Short-Term Outlook Continues to Deteriorate")

Numerous stocks have experienced significant declines over the past month, despite the overall index remaining stable. Illustration: L.Vũ |

Misinformation Surrounding Upgrade Voting

Ultimately, the speculative information regarding the “voting” for an upgrade by certain organizations last week turned out to be false, according to the analysis team at Vietcap Securities. FTSE Russell held two formal meetings in September, but the identities of the experts remain confidential.

Following the established procedure, the FTSE Market Classification Advisory Committee formally reviews countries on the Watch List (including Vietnam) for potential upgrades or downgrades. FTSE Russell’s recommendations are submitted to the FTSE Russell Policy Advisory Board. Subsequently, FTSE Russell seeks confirmation from the FTSE Russell Policy Advisory Board for these recommendations, which are then shared with the FTSE Russell Index Governance Committee for final approval. The FTSE Russell Index Governance Committee meeting is scheduled for this week.

Therefore, whether an upgrade will occur remains uncertain, although most commentators express optimism for the October review. Instead, analysts propose two scenarios: one is an upgrade announced on October 8 (local time), and the other is an upgrade in March of the following year.

The market has previously discussed the government’s efforts in establishing rules and meeting conditions for an upgrade. Most criteria have been met, except for two issues related to payment processes.

Specifically, the two barriers mentioned are the “Settlement Cycle” criterion, currently rated as “restricted,” which pertains to the pre-transaction margin requirement for foreign institutional investors. The second barrier is the “Settlement” criterion, related to failed trades. This criterion was upgraded from “unrated” to “restricted” in March 2025. Both criteria need to achieve a “compliant” rating.

The Ministry of Finance issued Circular 68 in November last year, eliminating this requirement and introducing a new No Pre-Funding (NPF) process. Over the past 11 months, FTSE Russell has assessed the effectiveness of the NPF process and gathered feedback from market participants. Vietnam recorded its first and only failed trade in December 2024. This failed trade also served as a test case for FTSE Russell to confirm the practicality of the failed trade handling process. Therefore, according to Vietcap, these two criteria could achieve a “compliant” rating.

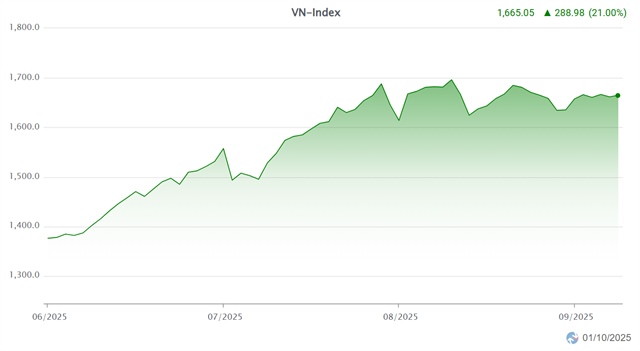

Following a strong rally since early June, the index has been moving sideways and showing increased divergence since mid-August. |

Current concerns among observers are that evaluators may still need time to monitor the market following changes in payment processes. For example, the two payment criteria require 6-9 months of observation, while the KRX system’s settlement cycle (T+1.5) is expected to need 6-9 months of monitoring, according to a report by HSC Securities.

In recent developments, the State Bank of Vietnam issued Circular 03 and Circular 25, aimed at streamlining the account opening process, which has been a significant administrative burden for foreign investors.

During an extraordinary shareholders’ meeting last week, Mr. Nguyễn Duy Hưng, Chairman of the Board of Directors at SSI Securities, expressed confidence with a 90-95% probability, pending investor opinions and voting. However, he also noted that an upgrade is not a “magic solution” for the market.

Market Enters a “Sensitive” Phase

During the waiting period for upgrade news, September saw a decline in Vietnamese securities. “Expectations of an upgrade have heightened anxiety among both institutional and individual investors,” the VietCap analysis team noted.

Last week, the index remained largely unchanged, with a 0.13% weekly increase, equivalent to a gain of over 2 points. Trading liquidity also decreased by 18%, averaging only 25.3 trillion VND, the lowest level in the past two months.

As of October 1, the VN-Index decreased by 0.97% compared to the previous month but still rose by 21% quarterly and over 31% year-to-date. Average monthly liquidity reached 21.317 trillion VND, down 37.5% from the previous month. Meanwhile, foreign investors continued to net sell over 27.257 trillion VND in the past month.

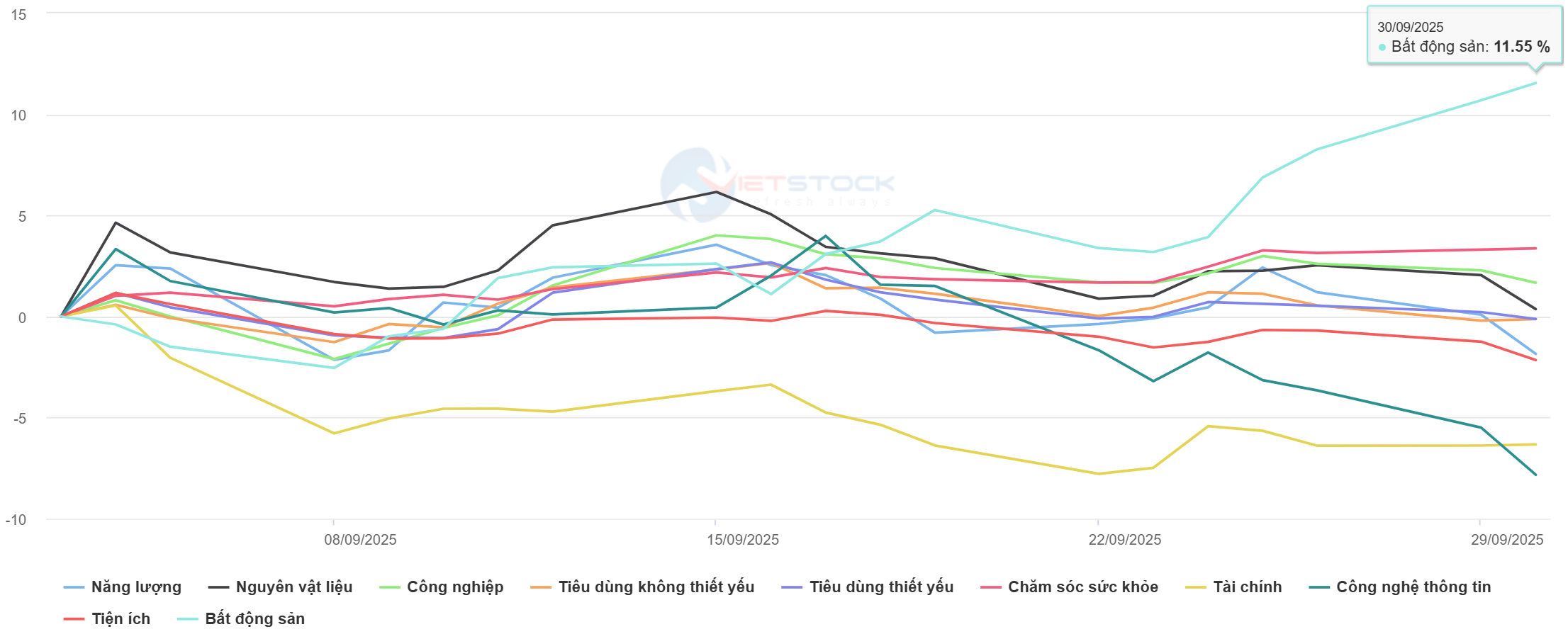

Over the past month, only the real estate sector showed positive performance, while most other sectors declined, with the financial sector experiencing the deepest drop. Source: Vietstock.

|

However, many investors believe the market is entering a “sensitive” phase due to other significant news, including business performance reports gradually “leaking” under the guise of “rumors.”

Most notably is the securities sector, expected to benefit significantly from this upgrade and anticipated positive business news as liquidity recorded new highs in the recent quarter.

According to the analysis team at MBS Securities, high-growth sectors include securities (73%), residential real estate (70%), and banking, forecast to grow by 21.5%, more optimistic than the first half of the year.

However, some sectors are estimated to have lower profit growth compared to the market, such as industrial real estate and telecommunications technology. The overall market forecast for the third quarter shows a 25% year-on-year profit growth.

Alongside upgrade prospects and business performance, upcoming third-quarter macroeconomic data will be crucial in determining year-end market trends.

In related news, S&P Global recently announced that Vietnam’s manufacturing PMI remained above the 50-point mark for the third consecutive month, unchanged from the previous month.

According to the analysis team at Maybank Securities, this figure is considered positive, with export activities also showing stabilization, expected to drive growth. However, inflation trends require close monitoring in the coming month. “The rate of increase in input costs and selling prices has continued to strengthen. If this trend persists, price pressures could negatively impact consumer demand,” the team noted.

According to MBS, to achieve GDP growth of 8% or higher, third-quarter growth must reach at least 8.4%. In a positive scenario (where growth and upgrade news align with expectations), the market could break out of its one-month accumulation phase. Conversely, domestic speculative capital could push the VN-Index below the 1,600-point mark.

Dũng Nguyễn

– 19:00 01/10/2025

Leading Brokerage Firm Goes Big: Offers Luxury Car Giveaway to Clients

The stock market’s year-end frenzy just got more thrilling with MBS’s launch of the “Breakthrough Trading – Win VF3” campaign, boasting an unprecedented prize structure. Investors need only trade from 10 million VND to stand a chance at winning the electric VF3 car, iPhone 17 Pro, and other high-value tech and fashion rewards.

Vietnam’s Stock Market: Scaling New Heights in a Historic Ascent

According to HSC Securities experts, while short-term weakening signals or the possibility of breaching the 1,600-point support level exist, they do not alter the positive long-term outlook for Vietnam’s stock market.

Vietnam Stock Market Upgrade Decision Meeting Scheduled for This Week

Vietcap Securities remains confident in its outlook, anticipating a positive announcement from FTSE Russell regarding Vietnam’s market classification next Wednesday.

Unlock Your Investment Journey with Dragon Capital’s “Metro Thịnh Vượng”

Unlock exclusive benefits when you open a new online investment account with Rong Viet: enjoy commission-free trading, a competitive margin rate of 6.88% per annum, access to our comprehensive ecosystem, and a chance to win VND 10 million in RVPIF fund certificates through our exciting lucky draw.

Foreign Investors Continue Selling Spree, Offloading Nearly VND 400 Billion in Real Estate Stocks on September 30th

In the afternoon session, CII and SHB emerged as the top net buyers in the market, with impressive purchase values of 90 billion VND and 82 billion VND, respectively.

{kind=link}