Just a few years ago, wallets were considered an indispensable item when going shopping, and cash was the king in every transaction due to its convenience and speed. However, today, QR codes have become ubiquitous—from coffee shops and gas stations to street-side tea stalls—and have emerged as the new payment method for users.

In 2024, QR code transactions saw robust growth in both volume and value, while ATM transactions declined by nearly 20% and accounted for a very small proportion of the entire system. This shift not only reflects changing consumer habits but also marks a significant advancement in digital banking in Vietnam.

Ngoc Minh, owner of a small cosmetics store in Ho Chi Minh City, used to queue at the bank every month-end to pay suppliers. Now, with just a few minutes on her phone, she can transfer money, download invoices, and reconcile transactions instantly. Duc Thanh, a 62-year-old retiree in Da Nang, was initially wary of technology due to security concerns. However, after his son helped him download the banking app and activate fingerprint authentication, he completely changed how he managed his finances. Every morning, Mr. Thanh simply opens the app to check his balance, receive savings interest, and pay utility bills for his family.

These changes highlight the significant achievements of the banking sector, as customers increasingly embrace and trust online transactions, driving a stronger push toward digitalization in the future.

Today, most commercial banks in Vietnam have developed digital banking applications (also known as mobile banking or digital banking) to serve their customers. This indicates that Vietnam has moved beyond the initial stages of banking digitalization, with a broad customer base and a technological infrastructure ready for breakthrough developments. This presents an opportunity for businesses to maximize the use of digital banking solutions in financial management and business expansion.

Vietnam is considered one of the fastest-growing digital banking markets in Southeast Asia. What is the most significant highlight of Vietnam’s digital banking sector at present, in your opinion?

Dr. Pham Nguyen Anh Huy – Senior Lecturer in Finance, RMIT University Vietnam: The pandemic accelerated a process that would have otherwise taken five years to shift consumer behavior from cash preference to mobile preference. Today, digital banking is no longer a niche market but a default requirement, especially among younger users.

The most notable highlight of Vietnam’s digital banking sector is the rapid adoption rate and ecosystem integration. We are witnessing swift digitalization within banks, as well as the convergence of banking, fintech, and digital platforms in everyday life, from e-commerce and ride-hailing to investment apps.

What sets Vietnam apart in the Southeast Asian context is that digital banking is not just about digitizing traditional services but also integrating financial services into users’ lifestyles. Banks like Techcombank, VPBank, Cake, and Timo are leveraging APIs and data analytics to deliver seamless, personalized experiences. This ecosystem-based approach is transforming how Vietnamese consumers interact with money and setting a regional benchmark for digital innovation.

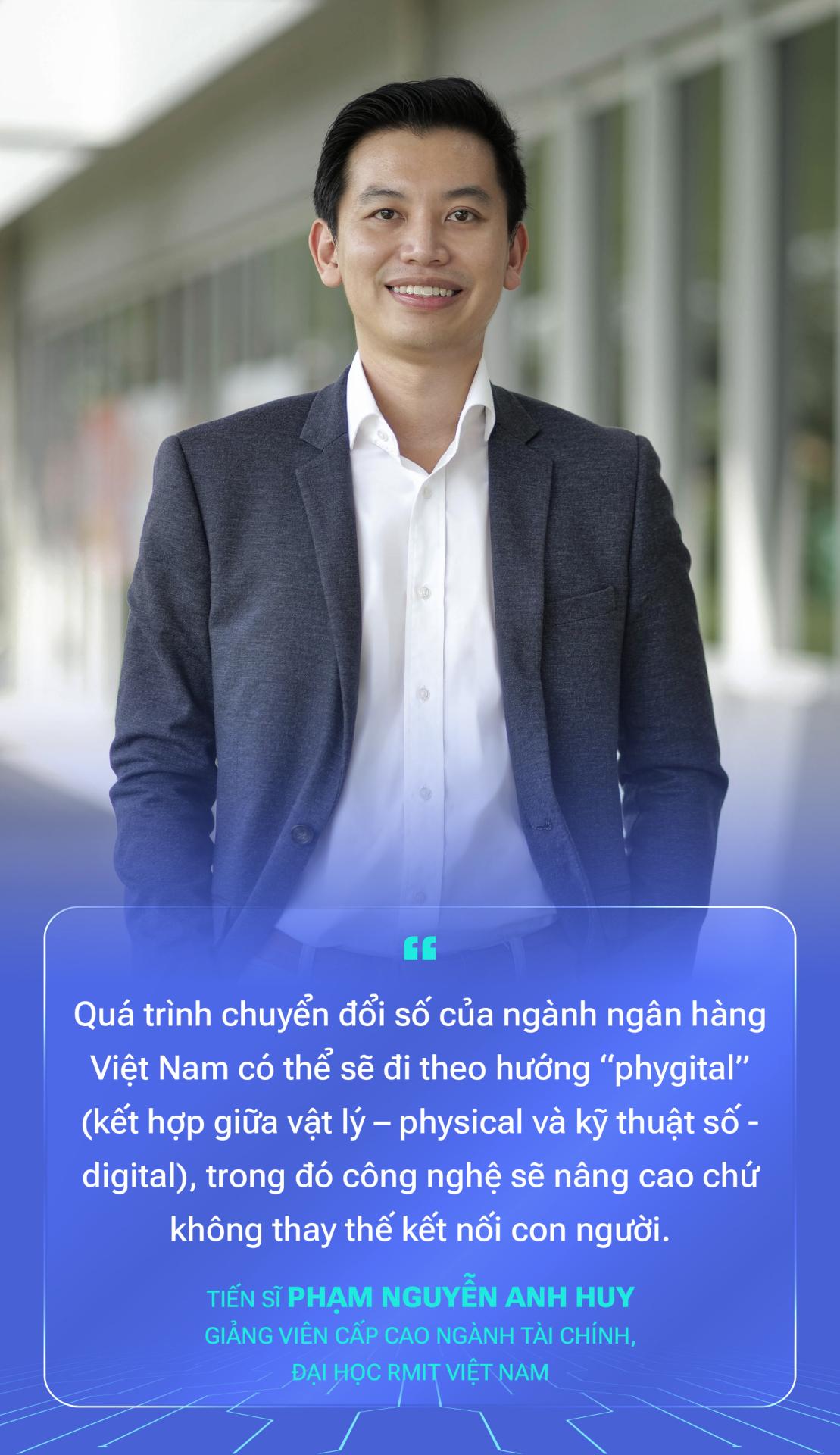

However, the readiness to embrace fully digital banking varies among customer segments. Trust, data privacy, and digital literacy remain significant barriers. Urban, tech-savvy consumers are ready for a 100% online experience, but many rural and older users still prefer a blend of digital and in-person interactions.

This suggests that Vietnam’s digital banking transformation may follow a “phygital” approach (combining physical and digital), where technology enhances rather than replaces human connections.

To what extent can generative AI and automation replace advisory and operational roles? How soon will we see fully automated, staffless banks become a reality?

AI is transforming banking at an astonishing pace, from automating customer support to providing personalized financial advice. However, machines can process information but cannot replicate empathy, trustworthiness, and ethical judgment—core elements of financial decision-making.

In the near future, we won’t see “staffless banks” but rather “human-centric smart banks,” where automation handles routine tasks, allowing employees to focus on strategic advice, relationship management, and solving complex issues. The future of finance is not “AI versus humans” but AI empowering humans to deliver smarter, more personalized, and comprehensive banking experiences.

According to the State Bank of Vietnam, digital banking is entering a phase of robust growth, with 87% of adults owning payment accounts as of early 2025. Digital banking revenue is projected to exceed $1 billion in 2025, driven by smartphone proliferation, high demand for digital experiences, and the rapid growth of e-commerce (forecast at $15.4 billion). This has created a massive opportunity, sparking a race among both large and small banks.

In this digital race, do larger or smaller, more agile banks have the advantage, in your opinion?

Dr. Fiza Qureshi – Senior Lecturer in Finance, RMIT University Vietnam: In Vietnam, large banks continue to hold advantages in infrastructure, customer trust, management experience, and access to capital. Banks like Vietcombank and VietinBank can leverage vast customer data to train generative AI models and possess robust risk management systems and financial capabilities for digital transformation.

However, smaller banks also have unique advantages. They operate with lower overhead costs, can quickly pilot new products, and often target specific customer segments.

Digital banks like Tnex, Cake, and Liobank have quickly attracted users by offering simple, app-focused services tailored to young, mobile-first customers, without the burden of maintaining physical branch networks. Overall, large banks excel in scale and stability, while smaller digital banks stand out for their speed, simplicity, and agility.

In the AI era, users are increasingly concerned about security risks and online fraud. Is digital banking leaving the elderly or low-income groups behind?

Trust is the foundation of digital finance—and once lost, it’s hard to rebuild. In the AI era, banks must shift from passive to predictive trust-building. This means using AI not just for automation but also for real-time risk detection, fraud prevention, and transparent customer communication. Beyond warnings and guidelines, banks should provide comprehensive support for victims of AI-related fraud, including helping customers recover losses after verifying they’ve been scammed.

Inclusivity must be at the core of this transformation. Older and low-income users should not be left behind. Banks can introduce simplified interfaces, use plain language, and offer micro-savings tools to bridge the gap. We must remember: the true success of digital banking is not measured by growth speed but by the number of people included in the journey.

Vietnam’s banking innovation culture remains cautious. How can banks overcome the “fear of risk” when experimenting with new technologies?

Vietnamese banks are often cautious about adopting new technologies due to concerns about financial risks, reputational impact, and regulatory requirements. However, avoiding innovation and experimentation can slow digitalization and limit the adoption of novel solutions.

Establishment of Free Trade Zones in Ho Chi Minh City, Da Nang, and Hai Phong by 2026

The Prime Minister has called for the development of exceptional, competitive policies to pilot a number of free trade zones.

CIO Techcombank in the Hot Seat: Leveraging AI to Solve Real-World Challenges

“AI Battle” – the first-ever artificial intelligence competition on national television and the country’s flagship AI program, is nearing the end of its semi-final rounds. In the latest episode, teams tackle the theme “Building a Bank’s Financial Report,” with guest judge Mr. Nguyen Anh Tuan, Director of Technology Division at Techcombank, joining the panel.

Anticipated Catalysts for MCH Stock Post HOSE Listing

Hailed as the “missing piece” of Vietnam’s stock market, MCH shares are taking center stage ahead of their upcoming transfer to the HOSE. With the advantages of the transfer, coupled with a favorable macroeconomic backdrop and strong corporate fundamentals, analysts are confident in Masan Consumer’s explosive growth in 2026 and beyond.

BIM Energy and Evolution Data Centres Sign MoU to Deliver Renewable Energy for Data Centers in Ho Chi Minh City

BIM Energy, a leading renewable energy developer and member of the BIM Group in Vietnam, has joined forces with Evolution Data Centres (EDC), Southeast Asia’s sustainable data center platform. Together, they have signed a Memorandum of Understanding (MoU) to collaborate on supplying renewable electricity through a Direct Power Purchase Agreement (DPPA). This partnership marks a significant step towards a greener future, combining BIM Energy’s expertise in renewable energy with EDC’s commitment to sustainable data center operations.

FTSE Director: Vietnam Upgraded, On Track for 1-Year Transition to Emerging Market Status

In a recent episode of Phở Side Chat, Wanming Du, Director of Index Policy for Asia Pacific at FTSE Russell, delved into the details surrounding Vietnam’s market upgrade. Du confirmed that Vietnam has officially met the technical criteria to qualify as a Secondary Emerging Market.

{kind=link}