The trading session on December 12th concluded on a somber note as the VN-Index experienced the most significant decline in the Asian region. A multitude of sectors were bathed in red, dragging the index downward and causing liquidity to plummet. At the close, the VN-Index dropped by over 52 points, settling at 1,647 points.

The market seemed to lose its direction, with the majority of stocks facing substantial downward pressure, reflecting a pervasive sense of caution and concern among investors.

In stark contrast to the overall trend, shares of Binh Minh Plastic Joint Stock Company (stock code: BMP) continued their upward trajectory. BMP’s stock price momentarily touched the upper limit before closing at 176,000 VND per share, marking a 3.7% increase and setting a new historical high (adjusted for stock splits). The company’s market capitalization surpassed 14.4 trillion VND for the first time.

BMP’s consistent growth on the stock exchange is underpinned by its stable business performance. Additionally, the stock has garnered investor favor due to its regular cash dividend policy and high payout ratio.

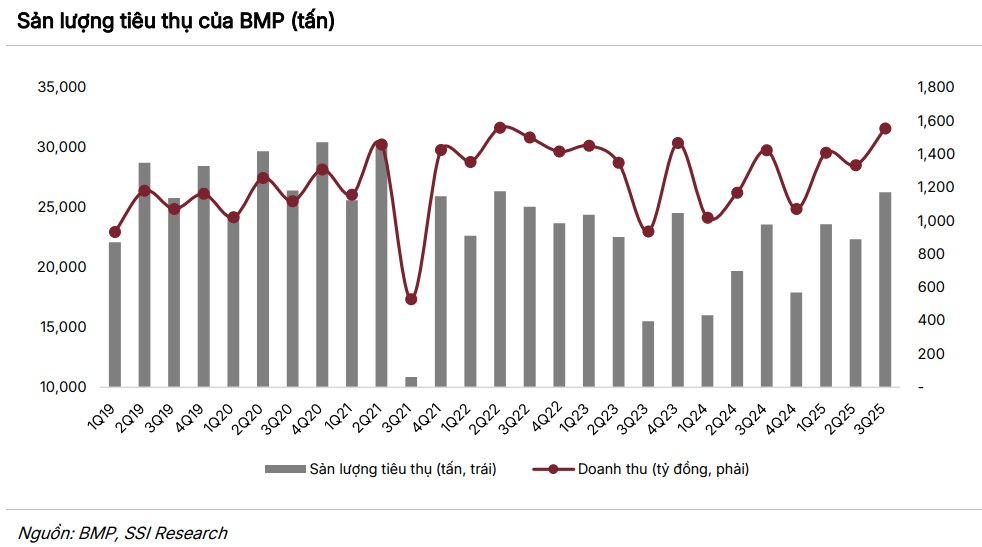

In Q3/2025, Binh Minh Plastic reported net revenue of 1,532 billion VND, a 9% increase compared to Q3/2024. Consequently, its after-tax profit reached nearly 351 billion VND, up 21% year-on-year.

This marks a new quarterly profit record since Binh Minh Plastic became a subsidiary of Nawaplastic Industries, a member of Thailand’s SCG Group, in early 2018. This result surpasses the previous record of 330 billion VND set in the preceding quarter.

For the first nine months of 2025, Binh Minh Plastic’s cumulative net revenue reached 4,224 billion VND, a 19% increase compared to the same period in 2024. After-tax profit stood at 967 billion VND, up 27% year-on-year.

Sustaining Double-Digit Growth

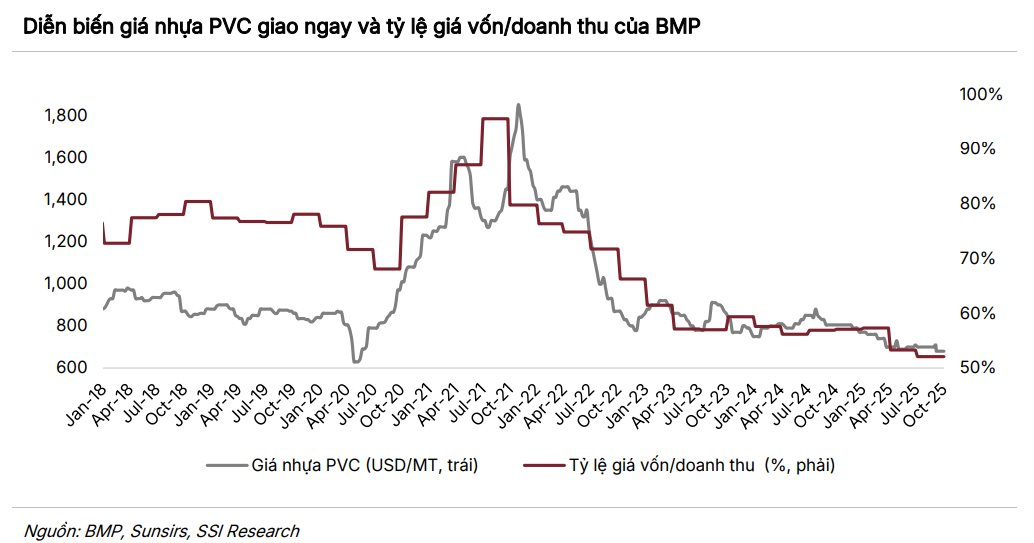

According to an update from SSI Securities (SSI Research), BMP’s competitive edge stems from its superior product quality compared to competitors. The “Product-Market Fit” approach and stringent supplier standards ensure that BMP’s products meet certification requirements for the Australian market and adhere to specific quality standards.

BMP’s operational capabilities and quality advantages are further strengthened by: (i) increasing automation through collaboration between NPI Thailand, BMP, and AI Tech; (ii) improved operational efficiency, including the restructuring of the Long An factory and warehouse expansion (from 7,000 to 12,000 tons by 2026); (iii) diversified supply sources, with 80% from domestic suppliers—a strategic advantage amid rising exchange rates; and (iv) optimized production processes.

Furthermore, Vietnam’s plastic industry is projected to grow at a CAGR of 8.44–10% from 2026 to 2030. BMP aims to capitalize on this trend by expanding its regional market presence, enhancing product value through innovation, and maintaining cost competitiveness through operational efficiency. The company’s management has set a minimum annual growth target of 10% for both volume and revenue, though profit growth remains contingent on PVC input cost dynamics.

Meanwhile, SSI anticipates that PVC prices will remain low in Q4/2025 and extend into the first half of 2026, barring any unexpected strong recovery in China’s industrial sector. Lower oil prices (down approximately 19% year-to-date), weakened downstream demand in China, and increased PVC production capacity continue to exert downward pressure on plastic resin prices.

“BMP remains unconcerned about supply disruptions, even if domestic producers shift to exports, thanks to its diversified supplier model. This provides the company with a significant advantage, particularly in a volatile market environment,” the report highlights.

Based on these analyses, SSI Research forecasts that in Q4/2025, BMP’s revenue will reach 1,253 billion VND, with net profit exceeding 285 billion VND, representing year-on-year increases of 17% and 24%, respectively. For the full year 2025, BMP’s net revenue is projected at 5,480 billion VND, with net profit reaching 1,270 billion VND, reflecting growth rates of 19% and 28%, respectively, compared to 2024.

In addition to SSI, several other research firms have provided outlooks for 2025. Specifically, BSC Securities and ACBS estimate that BMP’s 2025 net revenue could range from 5,515 billion to 5,654 billion VND, representing growth of 19.5% to 23% compared to the previous year.

This growth is expected to be driven by a recovery in consumer demand and existing sales strategies. After-tax profit forecasts for 2025 range from 1,316 billion to 1,347 billion VND, reflecting growth of 33% to 36% compared to 2024.

12/12 Session: Foreign Investors Continue Net Selling Over 500 Billion VND – Which Stocks Were Hit Hardest?

In contrast, HPG topped the net buying list with a value of approximately VND 88 billion.

Billionaire Stocks Hit as Foreign Investors Net Sell Over $170 Million in Week of December 8-12

Foreign investors, who were net buyers in the previous week, reversed their position and became net sellers throughout the past week.

“After a 50-Point Drop in 3 Volatile Sessions, How Much Further Could the VN-Index Retreat?”

At present, the expert observes that the market is exhibiting several more positive signals.

Stock Market Plunges Sharply

The weekend trading session concluded on a negative note, with the VN-Index plunging over 50 points. This sharp decline erased all gains from the consecutive winning streak earlier in December.

How Does Becamex IDC Secure Funding Without Selling Shares?

Becamex IDC sought to publicly offer 150 million BCM shares, but the proposal failed to gain shareholder approval. The company has consistently turned to bond issuance as a means to secure capital.

{kind=link}