: Mixed Signals Emerge")

: Short-Term Outlook Continues to Deteriorate")

“**USD/VND Exchange Rate: Analyzing the Dynamics and Impact**

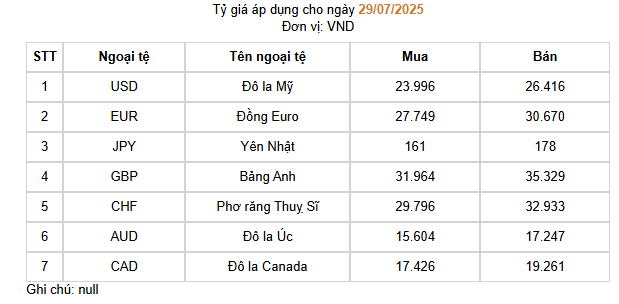

On July 29, 2025, the State Bank of Vietnam (SBV) set the daily reference exchange rate at 25,206 VND per USD, a 24-dong increase from the previous session. The selling price of USD by SBV was also raised to 26,416 VND per USD.

Commercial banks followed suit, with Vietcombank offering rates from 26,010 to 26,400 VND per USD, while VietinBank traded at 26,039 to 26,399 VND per USD for buying and selling, respectively.

Source: SBV

|

Mr. Nguyen Quang Huy, CEO of the Faculty of Finance and Banking at Nguyen Trai University, commented on the continuous surge in the USD/VND exchange rate, with the buying price surpassing the 26,000 VND per USD mark and the reference rate consistently hitting new highs. He attributed this development to a combination of external and internal factors, amidst a volatile global economic landscape and mounting macroeconomic management pressures.

On the international front, the US dollar maintained its upward trajectory due to the US Federal Reserve’s cautious monetary policy, prolonged high-interest rates, and international capital flows gravitating towards safe-haven assets. This dynamic exerted pressure on regional currencies, including the VND. Additionally, the ongoing shifts in global supply chains and trade presented new challenges for exchange rate management in developing economies.

Domestically, there was an increase in foreign currency demand following the import payment cycle, foreign debt payments, and periodic profit remittances by certain economic sectors. Conversely, foreign currency supply tended to slow down in the short term due to export market fluctuations and a growing tendency to hold foreign currencies. Such phenomena are not uncommon during policy transition periods and necessitate close monitoring and agile responses from the regulatory authorities.

The adjustment in the reference exchange rate was viewed as a proactive, technically driven move that aligned with market realities. It also contributed to stabilizing market sentiment and ensuring resources for exports amidst intensifying global competition.

The sharp rise in exchange rates signaled a new phase in the market, where the balance between macroeconomic stability and adaptability to external factors became pivotal. This juncture also called for enhanced information sharing and coordinated actions among businesses, credit institutions, and regulatory bodies to safeguard stability and sustainable growth in the medium to long term.

Meanwhile, PGS.TS. Nguyen Huu Huan, a senior lecturer at the University of Economics in Ho Chi Minh City, attributed the hot spell in exchange rates to three primary factors.

Firstly, the trade balance shifted from a surplus to a deficit. For two consecutive months (June and July), Vietnam experienced a shift from a trade surplus to a deficit. Specifically, export turnover showed signs of decline, while import demand remained high. This situation could be partly attributed to seasonal factors, as large orders were front-loaded in the first half to take advantage of US trade policies. The trade deficit increased the demand for foreign currency to make payments, directly putting pressure on the exchange rate.

Secondly, key industrial production indices weakened. Important indicators such as the Purchasing Managers’ Index (PMI) and indices in the manufacturing and business sectors showed declines, reflecting a downturn in the health of the manufacturing and export sectors, which, in turn, reduced the foreign currency supply to the economy.

Thirdly, the SBV had been injecting substantial Vietnamese dong liquidity into the market through the open market operation (OMO) channel to support commercial banks. The underlying reason was the strong flow of money into investment channels such as securities and real estate, which were in the recovery phase, causing temporary liquidity shortages in some banks. Injecting large amounts of VND into the market while maintaining high-interest rates indirectly led to the depreciation of the domestic currency against the USD.

Amid the rising exchange rates, the question arises as to what measures the SBV will take to stabilize the market. Halting liquidity injections could ease pressure on exchange rates but would immediately impact the banking system’s liquidity negatively, pushing interest rates higher and affecting macroeconomic stability.

At the same time, the option of using foreign exchange reserves for intervention is not considered optimal at this point. Vietnam’s foreign exchange reserves are estimated to have decreased to a relatively low level, hovering around 80-90 billion USD.

Expectations for easing exchange rate pressure towards the year’s end

Looking ahead to the latter part of the year, Mr. Huan anticipated that exchange rate pressure would persist. Typically, the market faces three peak periods of foreign currency demand: the back-to-school season (August-September), the Christmas and New Year holiday season (November-December), and the pre-Lunar New Year shopping and foreign debt payment season (January).

However, the difference this year is that the pressure on exchange rates has persisted throughout the year. The core reason remains the interest rate differential, with the US Federal Reserve not showing any signs of lowering interest rates, while Vietnam maintains a relatively low-interest rate environment to support economic growth.

According to Mr. Huan, the expectation for easing pressure in the coming months lies in the recovery of industrial production indices and the usual increase in remittances during the year-end holiday season.

Cát Lam

– 15:54 29/07/2025

“

The Greenback Slides: A Sudden Shift in Fortune

“The U.S. dollar took a turn last week, experiencing a decline in the international market as the deadline for higher tariffs loomed. As the week of July 21-25, 2025, unfolded, the implications of President Donald Trump’s trade policies became increasingly apparent, with the dollar’s performance reflecting the market’s anticipation of these changes.”

Tightening Financial Discipline: Ensuring a Secure Banking System

As of this year, banking sector inspections have resulted in the punishment of 277 organizations and individuals, with 73 administrative fines totaling over VND 10.4 billion.

Japan Concerned as Yen Falls to Four-Month Low

The Japanese yen continued its downward trajectory against the US dollar on August 1st, with the exchange rate reaching a staggering 150.9 yen to one USD at certain points during the trading day.

Stabilizing Businesses for the Lunar New Year Holiday with Special Loan Interest Rates

Meeting capital needs and providing banking services, especially maintaining lending rates lower than the common rate and the same term lending rates of credit institutions, have significantly contributed to the market stabilization program, especially during the Lunar New Year period.

The Greenback and the Yuan: A Tale of Contrasting Fortunes

The State Bank of Vietnam’s central exchange rate today stands at 24,333 VND, a decrease of 5 VND compared to the morning of January 15th. Meanwhile, the Chinese yuan remained stable at commercial banks, showing no signs of fluctuation.

{kind=link}