.")

Issue – CEO FiinRatings’ Assessments: “Dealing with bond repayment cash flow is still a major challenge for investors” Đinh Thơm (Perform) • 01/03/2024 06:36

“Addressing the current issues of real estate credit or real estate bonds will largely depend on the legal clearance of specific projects that have been implemented according to existing regulations. or old policies for projects to access credit capital, implementation and sales,” said Mr. Nguyen Quang Thuan, CEO of FiinRatings, expressing his point of view.

Mr. Nguyen Quang Thuan, CEO of FiinRatings

Risks or impacts on investors still exist

Reporter: “Sir, statistics show that 2024 will be the peak year for bond maturities. How do you assess the pressure of bond maturities this year?”

Mr. Nguyen Quang Thuan: As of February 29, 2024, the total value of individual bonds of non-banking issuers maturing in the remaining months of 2024 is VND 240.9 trillion. This figure includes both the principal and the expected interest, after implementation of rescheduling or restructuring, including under Decree 08.

Although the absolute number has decreased significantly compared to the peak period and before restructuring, the risks still persist for investors who currently own those bond lots.

We would like to note the maturity value for all 3 real estate industry groups, construction, tourism and entertainment currently at VND 186.6 trillion to mature in the remaining months of 2024 (including real estate VND 131.9 trillion, construction and materials VND 26.8 trillion; tourism and entertainment VND 23.1 trillion, as of 28/2/2024).

These are the industries that we still see facing many difficulties, and more importantly, the quality of the issuing organizations that mobilized in previous years, which reached its peak in 2021 at a low level and there are many projects with thin or just entering into operation financial strength.

Therefore, risks or impacts on investors, including individual investors, still exist. We foresee that although Decree 08 has expired, the restructuring of bond debts will still take place according to the negotiation mechanism between the issuer and the investor.

Regarding bond buyers who are commercial banks, the risk of bad debt may increase as the majority of issuers also have credit balances with banks alongside the bonds.

Reporter: “In fact, many enterprises with large bond values this year are real estate non-listed businesses and have little information on the market, and the published business results are not very optimistic. So in your opinion, how is the likelihood of payment of these businesses?”

Mr. Nguyen Quang Thuan: Recently, the quality of information disclosure or disclosure has improved significantly according to the new regulations of Decree 65 and the requirement to concentrate transactions on HNX from July 2023 for individual bonds. However, to assess and update the clear bond repayment capacity is a very big challenge, especially for individual investors.

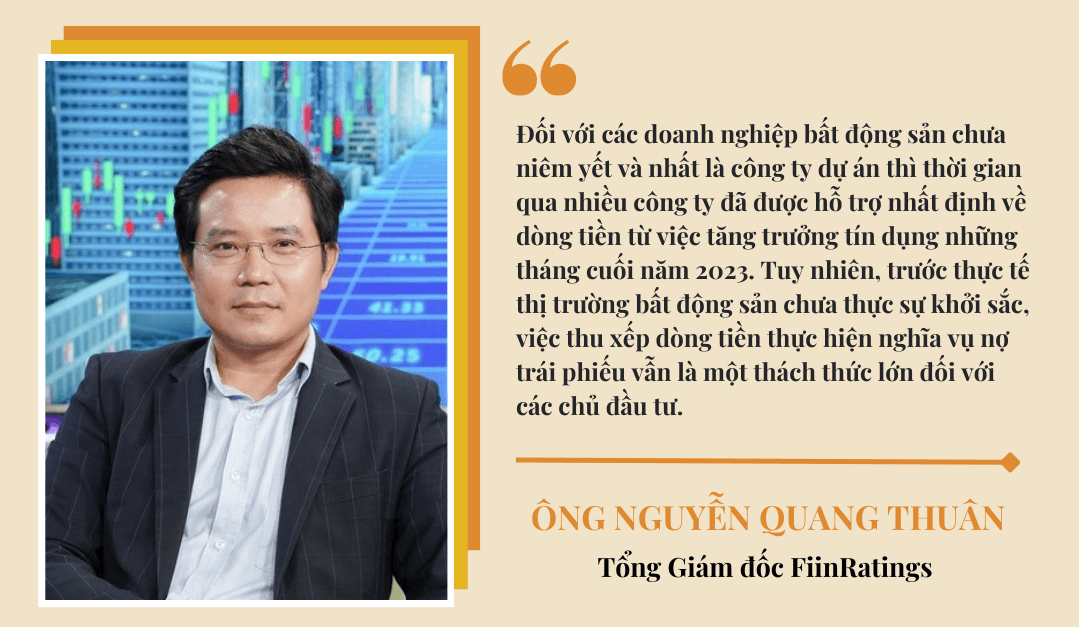

For real estate companies that are not listed and especially project companies, many companies have been supported by cash flow from credit growth in the last months of 2023. However, given the current state of the real estate market and the need for cash flow to fulfill bond obligations remains a major challenge for investors.

From a market risk perspective, this is still a factor that many bond investors are facing with the delay in payment will continue to occur and negotiations for these bond lots must be carried out.

Reporter: “Statistics show that the ratio of delayed payment of interest or principal on bonds in the real estate enterprise group is many times higher than other industry groups. Will this figure continue to increase in 2024, sir?

Mr. Nguyen Quang Thuan: The ratio of delayed payment of real estate bonds is about 23.5% of the circulating value at the end of 2023. This figure is calculated based on both the bonds that have been restructured.

From the perspective of systemic safety risks, we assess that the risks are not large because the scale of circulating real estate bonds (VND 403.5 trillion, of which 96% equivalent to VND 387.4 trillion is individual bond) is still not too large in proportion to total system credit outstanding (accounting for about 2.9% of total system credit) and the fundamental transmission effects, in our opinion, have been controlled.

New issuances in 2023 in the real estate industry with a total value of VND 87 trillion, mostly associated with large enterprises or projects with lower legal risks than previous periods. In addition, most of those bonds are purchased and owned by commercial banks, so we expect careful assessment and appraisal by the banks in their financing decisions.

Reporter: “According to you, how will the new amended laws on Real Estate Business (amended), Housing (amended), and Land (amended) affect the real estate market in general? Will the expectation of market recovery help real estate bonds overcome the most difficult phase?”

Mr. Nguyen Quang Thuan: The new or amended regulations of these laws will have positive impacts on the capital market in general because these new regulations provide more specific guidelines, especially regarding the legal transparency of projects or real estate products, which is a major risk factor in the current phase.

After the recent violations, it is very difficult for banks to be able to lend or businesses to raise corporate bonds for a project that is not legally clear. Therefore, the latest regulations, such as the Land Law amendments, for example, provisions that provide better protection of the legitimate rights and interests of land users or narrow down cases that require permission when changing land use purposes, will contribute to creating favorable conditions for capital mobilization, including the channel of corporate bonds, in the coming years.

However, the application of new policies will take time and after the law takes effect along with the documents under the law are promulgated. Therefore, the impact will provide a foundation for the recovery of the real estate market rather than supporting the resolution of current issues in real estate bonds.

Addressing the current issues of real estate credit or real estate bonds will largely depend on the legal clearance of specific projects that have been implemented according to existing regulations or old policies for projects to access credit capital, implementation and sales.

The corporate bond market should have the participation of institutional investors

Reporter: “Recently, regulators have made efforts to provide solutions to help the bond market recover and develop more healthily. In your opinion, have these solutions been strong enough?”

Mr. Nguyen Quang Thuan: Clearly, the new regulations of Decree 65 have contributed to tightening and making issuance conditions more specific and transparent, as well as enhancing the responsibilities of parties involved in a bond transaction, including the risk acceptance commitment of individual investors.

In addition, Decree 08 of the Government has supported a lot for the “soft landing” of the bond market or the regulations of the State Bank in relaxing the conditions for allowing banks to repurchase corporate bonds (Circular 16 and then Circular 03). The smoothness in implementing the rescheduling of repayment terms and maintaining debt groups (Circular 02) from the State Bank has also helped reduce the pressure on customers in difficulty, including real estate businesses.

The registration of concentrated trading for individual bonds on HNX is also an important solution to create liquidity for this market and contribute to improving information transparency, especially about bond prices and bond yields associated with credit quality or credit ratings. We are gradually creating a soft foundation for the market towards sustainable development.

However, we still believe that the corporate bond market according to international and regional practices should be a market with the participation of institutional investors. The new provisions that enhance the standards for professional investors participating in individual bond investments are a good policy to implement this orientation.

In parallel with the above measure, there should be solutions to improve the participation of institutional investors other than commercial banks outside of a wide public bond offering channel, targeting any party interested in the fixed-income product channel, such as corporate bonds.

Reporter: “We can see that the bond market has shown more positive changes in the last months of 2023, so why did it slow down at the beginning of 2024? With the developments of the bond market in early 2024, do you have any predictions for the whole year?”

Mr. Nguyen Quang Thuan: The improvement in the second half of 2023 was thanks to the main factors including: implementing the new regulations of Decree 65, solutions to remove legal barriers in real estate and taking advantage of the low-interest rate environment as well as exploiting the credit relief of the banking system in the last months. of the year.

In the first two months of 2024, although the domestic interest rate environment is still low, as mentioned above, the focus of basic investors on commercial banks while other institutional investors have not prospered has reduced new issuance activities or not vibrant again, along with low or negative credit growth in many banks.

Therefore, for the market to grow steadily, sustainably, and contribute to mobilizing domestic resources for long-term economic development, the key is still to develop or open up the basis of institutional investors for individual bonds, along with more effective solutions for strengthening wide public offering channels and targeting any entity interested in the fixed-income product channel such as corporate bonds.

Reporter: Thank you, sir!